| ||

| 29th June 2026 | view in browser | ||

| Geopolitical risk fades, but still not far enough | ||

| Markets enter the new week with investors balancing a hawkish Fed, key US jobs data and central bank guidance against renewed Middle East tensions, as the US Dollar remains firm, equities consolidate after recent weakness and oil geopolitical risks return to the forefront. | ||

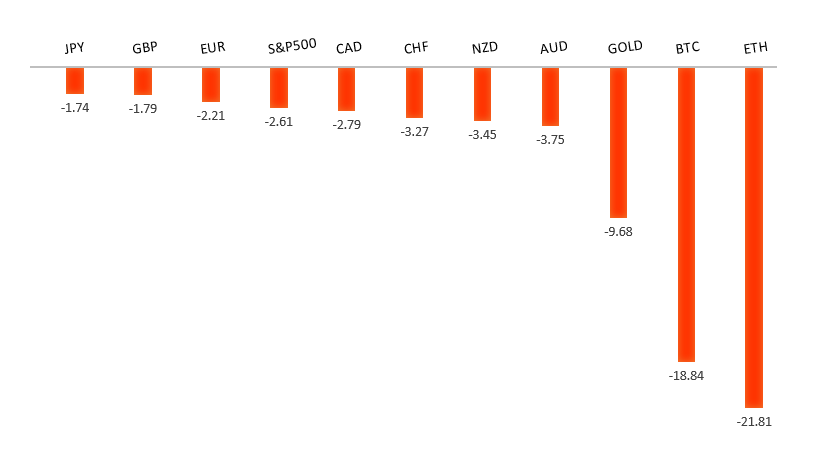

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1529 - 18 June high - Medium R1 1.1440 - 23 June high - Medium S1 1.1325 - 24 June/2026 low - Medium S2 1.1300 - Figure - Medium | ||

| EURUSD: fundamental overview | ||

| The euro remains under pressure against the US Dollar as markets continue to favor the Greenback amid a combination of geopolitical uncertainty and a more hawkish Federal Reserve outlook. Although softer-than-expected US PCE inflation data eased immediate expectations for another near-term Fed rate hike and triggered a modest pullback in the Dollar, Fed officials continue to signal that policy is likely to remain restrictive, keeping US yields elevated and limiting EURUSD upside. At the same time, lingering tensions in the Middle East, including uncertainty surrounding shipping through the Strait of Hormuz, continue to support safe-haven demand for the Dollar. On the Eurozone side, expectations for further ECB tightening have become more mixed as lower energy prices ease inflation pressures, although some policymakers and private-sector economists still see inflation remaining sticky enough to justify another rate increase later this year. As a result, the euro is finding some support from lingering ECB tightening expectations, but the broader backdrop continues to be dominated by Dollar strength driven by Fed policy divergence and geopolitical risks. | ||

| GBPUSD: technical overview | ||

| The Pound remains exceptionally well supported on dips into the 1.3000 area, with the price largely consolidating above the psychological barrier and previous resistance turned support in the form of the 2023 high. Look for the market to continue be well supported on dips ahead of the next major upside extension through the yearly high at 1.3870 and towards a retest of the 2018 high at 1.4377 further up. Only a monthly close below 1.3000 negates. | ||

| ||

| R2 1.3325 - 18 June high - Medium R1 1.3274 - 22 June high - Medium S1 1.3140 - 24 June/2026 low - Medium S2 1.3100 - Figure - Medium | ||

| GBPUSD: fundamental overview | ||

| The pound has found some support after the recent US Dollar rally lost momentum, although it still ended the previous week under modest pressure as markets continue to balance a resilient US economy and hawkish Federal Reserve against domestic UK developments. Political uncertainty has eased following Keir Starmer’s resignation, with investors taking comfort from frontrunner Andy Burnham’s commitment to maintain Chancellor Rachel Reeves’ fiscal rules, helping calm concerns over a looser fiscal stance that had previously weighed on sterling and pushed Gilt yields higher. At the same time, expectations for additional Bank of England tightening have been scaled back, with markets now pricing only limited further rate hikes this year, reflecting confidence that UK inflation will continue to moderate. Looking ahead, focus shifts to next week’s UK GDP data alongside US nonfarm payrolls and Fed Chair Kevin Warsh’s congressional testimony, all of which could prove pivotal in shaping relative monetary policy expectations and the near-term direction for GBPUSD. | ||

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped below 162.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 162.00 negates. | ||

| ||

| R2 163.00 - Figure - Medium R1 161.96 - Multi-Year high/2024 - Very Strong S1 160.41 - 18 June low - Medium S2 159.54 - 11 June low - Strong | ||

| USDJPY: fundamental overview | ||

| The Yen remains under pressure as the Bank of Japan’s long-awaited 25bp rate hike to 1.00% has done little to offset the still-wide interest rate differential with the United States, especially after the Federal Reserve maintained a hawkish stance and signaled rates are likely to remain elevated for longer. That continues to encourage carry trades and keeps USDJPY trading near multi-decade highs despite growing speculation that Japanese authorities could intervene again to support the currency. The prospect of further BoJ tightening later this year, together with periodic intervention fears, has helped limit the pace of Yen losses rather than reverse the trend, while bouts of geopolitical uncertainty in the Middle East have only provided modest safe-haven support as investors continue to favor the higher-yielding US Dollar. Looking ahead, markets are focused on Japan’s Tankan business survey for clues on the domestic economy and the BoJ’s policy path, while US labor market data and Federal Reserve communication remain the key drivers of rate expectations, with strong US data likely to reinforce Dollar strength and keep pressure on the Yen. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7089 - 15 June high - Strong R1 0.6979 - 11 June low - Medium S1 0.6875 - 26 June low - Medium S2 0.6833 - 30 March low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian Dollar remains under pressure as resilient US economic data, elevated geopolitical tensions in the Middle East and expectations that the Federal Reserve could still tighten policy again this year continue to underpin the US Dollar. While stronger-than-expected Australian employment data, with a solid rebound in job creation and unemployment edging back to 4.4%, has helped reinforce the view that the Reserve Bank of Australia can remain patient rather than rush into easing, the underlying details were softer, with weaker hours worked, rising underemployment and job gains concentrated in part-time positions pointing to a gradual cooling in labor market conditions. The Aussie has also found only limited support from month-end US Dollar profit-taking, with investors remaining cautious as China’s uneven economic recovery continues to cloud the outlook for Australian exports despite ongoing hopes for additional Chinese policy stimulus. Markets are now looking ahead to key US data and evolving Fed expectations, while developments in China and broader global risk sentiment remain important drivers for the Australian Dollar. | ||

| Suggested reading | ||

| Ten years after Brexit, L. Fisher, Financial Times (June 26, 2026) Tethered To The Tail Of a Drunken Dragon, P. Harlalka, Bond Vigilantes (June 25, 2026) | ||