| ||

| 2nd July 2026 | view in browser | ||

| Dollar firms ahead of critical US jobs report | ||

| Markets head into Thursday with investors focused squarely on the U.S. jobs report as resilient global central bank hawkishness, a firmer dollar, rising Treasury yields and softer oil prices continue to drive cross-asset price action. | ||

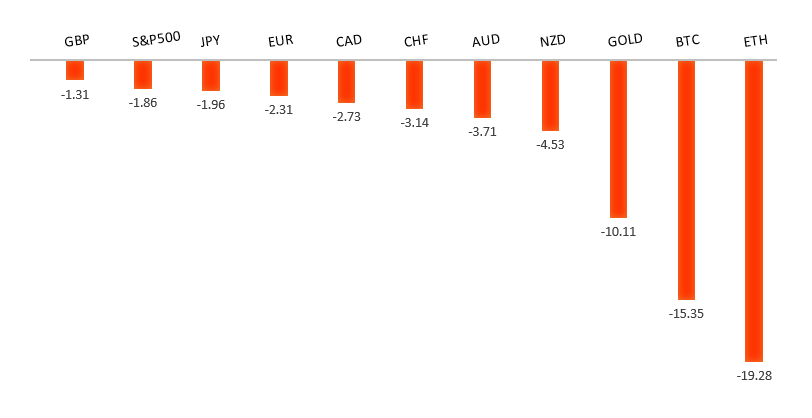

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1529 - 18 June high - Medium R1 1.1440 - 23 June high - Medium S1 1.1325 - 24 June/2026 low - Medium S2 1.1300 - Figure - Medium | ||

| EURUSD: fundamental overview | ||

| The euro remains under modest pressure as markets continue to favor the US Dollar on the back of a widening policy divergence between the Federal Reserve and the European Central Bank. Softer-than-expected Eurozone inflation data this week has reinforced expectations that the ECB is nearing the end of its tightening cycle, reducing the likelihood of another rate hike this year despite President Christine Lagarde reiterating at the ECB Forum in Sintra that the Governing Council stands ready to take whatever steps are necessary to keep inflation under control and stressing that the region is not in stagflation. By contrast, Fed Chair Kevin Warsh maintained a cautious, inflation-focused stance, refusing to provide forward guidance while reaffirming the Fed’s commitment to restoring price stability, helping keep expectations alive for additional US tightening even after softer US ADP employment and ISM manufacturing data. At the same time, lingering geopolitical tensions in the Middle East continue to underpin safe-haven demand for the Dollar, leaving EURUSD vulnerable ahead of Thursday’s closely watched US nonfarm payrolls report, which is expected to play a key role in shaping the next leg of Fed rate expectations and, in turn, the direction of the single currency. | ||

| GBPUSD: technical overview | ||

| The Pound remains exceptionally well supported on dips into the 1.3000 area, with the price largely consolidating above the psychological barrier and previous resistance turned support in the form of the 2023 high. Look for the market to continue be well supported on dips ahead of the next major upside extension through the yearly high at 1.3870 and towards a retest of the 2018 high at 1.4377 further up. Only a monthly close below 1.3000 negates. | ||

| ||

| R2 1.3325 - 18 June high - Medium R1 1.3293 - 1 July high - Medium S1 1.3140 - 24 June/2026 low - Medium S2 1.3100 - Figure - Medium | ||

| GBPUSD: fundamental overview | ||

| The British Pound remains relatively well supported as investors balance a still-resilient UK inflation outlook against a more cautious global backdrop. Sterling found support after softer-than-expected US labor market data weighed on the US Dollar, while Federal Reserve Chair Kevin Warsh maintained a hawkish tone by reiterating the Fed’s commitment to restoring price stability without offering forward guidance. Domestically, political concerns have eased after Andy Burnham reaffirmed his commitment to Chancellor Rachel Reeves’ fiscal rules following Keir Starmer’s resignation, helping reassure investors that fiscal discipline will remain intact. At the same time, Bank of England Governor Andrew Bailey has continued to strike a patient tone, arguing that tighter financial conditions give policymakers time to assess whether higher energy prices feed into broader inflation, even as he acknowledged inflation could rise toward 3.2% later this year. Markets continue to price in at least one BoE rate hike in 2026, reflecting persistent inflation concerns despite the recent decline in oil prices following easing tensions in the Middle East. Sterling has also benefited on the crosses, with EURGBP falling to its lowest level in roughly a year after softer Eurozone inflation reinforced expectations that the ECB may be closer to the end of its tightening cycle than the BoE. | ||

| USDJPY: technical overview | ||

| The major pair has extended its run to fresh multi-decade highs, with the latest push through 160.00 opening the door for further upside towards 165.00-170.00. At the same time, daily studies are looking quite stretched, suggesting we could see a healthy correction on the horizon. A break back below 161.51 would be required to take the immediate pressure off the topside and strengthen the case for a larger pullback. Until then, the market will continue to be focused on additional gains. | ||

| ||

| R2 163.00 - Figure - Medium R1 162.84 - Multi-Year high/1 July 2026 - Strong S1 161.51 - 29 June low - Strong S2 160.99 - 19 June low - Medium | ||

| USDJPY: fundamental overview | ||

| The Yen remains under pressure near four-decade lows as the wide interest rate differential between Japan and the United States continues to fuel carry trades, with markets still pricing a high probability of at least one additional Federal Reserve rate hike this year. While softer-than-expected US ADP employment data briefly weighed on the US Dollar, resilient US economic activity and expectations that Thursday’s Nonfarm Payrolls report could reinforce the Fed’s inflation-fighting stance have limited any sustained relief for the Yen. On the domestic side, Japan’s latest Tankan survey surprised to the upside, with business sentiment reaching its strongest level in eight years and inflation expectations remaining above the Bank of Japan’s 2% target, reinforcing expectations that the BoJ will continue gradually normalizing policy. However, investors remain unconvinced that the pace of BoJ tightening will be sufficient to materially narrow the US-Japan yield gap, leaving the Yen vulnerable. At the same time, speculation over possible intervention by Japan’s Ministry of Finance continues to intensify as USDJPY approaches the 163.00 area, although authorities have so far limited themselves to relatively measured warnings, encouraging traders to continue testing the market’s tolerance for further Yen weakness while remaining cautious of the risk of a sudden intervention-driven reversal, particularly during the thinner liquidity conditions around the US holiday. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7089 - 15 June high - Strong R1 0.6979 - 11 June low - Medium S1 0.6865 - 30 June low - Medium S2 0.6833 - 30 March low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian Dollar remains caught between a broadly resilient domestic backdrop and external headwinds that continue to favor the US Dollar. While the Reserve Bank of Australia maintains that policy needs to stay restrictive until inflation is firmly on track to return to target, markets have continued to scale back expectations for additional rate hikes this year as policymakers signal patience and a willingness to let existing policy work through the economy. Australia’s economic fundamentals remain relatively solid, with a healthy labor market, resilient domestic demand and a return to trade surpluses supported by resource exports, although growth has moderated and inflation is only easing gradually. At the same time, China—the Australian economy’s largest trading partner—is providing stability rather than a fresh growth impulse, with manufacturing activity holding up but domestic demand remaining subdued, limiting support for the Aussie. More recently, the currency has come under renewed pressure from a firmer US Dollar, resilient US economic data, elevated Treasury yields and a cautious risk backdrop amid lingering Middle East tensions, although softer US ADP employment data has tempered some of the Dollar’s strength ahead of Thursday’s closely watched US nonfarm payrolls report. Attention now turns to Australia’s latest trade balance figures, where another solid surplus driven by iron ore and coal exports could provide near-term support, but broader direction is still likely to hinge on US rate expectations, global risk sentiment and incoming Chinese data. | ||

| Suggested reading | ||

| Investors Are Still Fighting Last War On Inflation, Fisher Investments (June 30, 2026) The Big Problem As Warsh Tries To Revive Greenspan Fed, R. Forsyth, Barron’s (June 26, 2026) | ||