| ||

| 5th November 2025 | view in browser | ||

| Dollar rally could be nearing its end | ||

| Global markets are tilting toward risk aversion amid growing AI bubble fears, fueled by Michael Burry’s $1B+ put options on Nvidia and Palantir, plus bubble warnings from Morgan Stanley and Goldman Sachs CEOs, alongside a U.S. government shutdown now exceeding a month. | ||

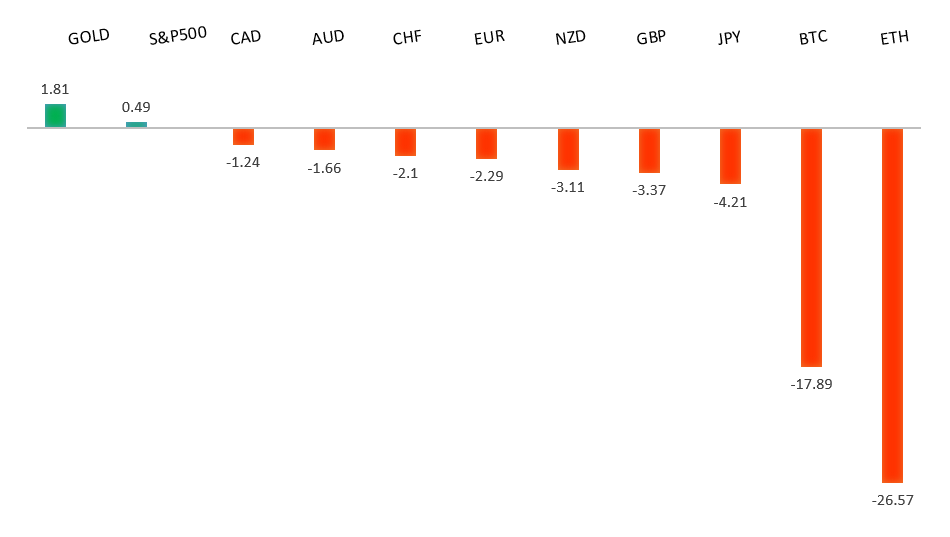

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1729 - 17 October high -Strong R1 1.1669 - 28 October high - Medium S1 1.1446 - 19 June low - Medium S2 1.1392 - 1 August low - Strong | ||

| EURUSD: fundamental overview | ||

| ECB Governing Council member Joachim Nagel reports that Eurozone data align with the ECB’s projections, supporting unchanged interest rates until the December review amid uncertainties. Markets have narrowed expectations for ECB-Fed policy divergence after Fed Chair Powell tempered December cut hopes, pressuring EURUSD lower, though the 1.1392 support level should hold without new catalysts. Analysts at some major banks view the euro as undervalued by about 1%, with neutral positioning poised for rallies on weak U.S. jobs data; they forecast ECB rates steady until mid-2026 while the Fed eases, driving EURUSD to $1.18–$1.20 by year-end and up to $1.26 by Q3 2026, aided by improved European growth outlooks and reduced global risks. Upcoming data include September PPI (forecast flat MoM at 0.0%, YoY -0.2%, signaling easing deflation), finalized October HCOB Services/Composite PMIs, and German factory orders (MoM +0.9%, YoY -4.1%). | ||

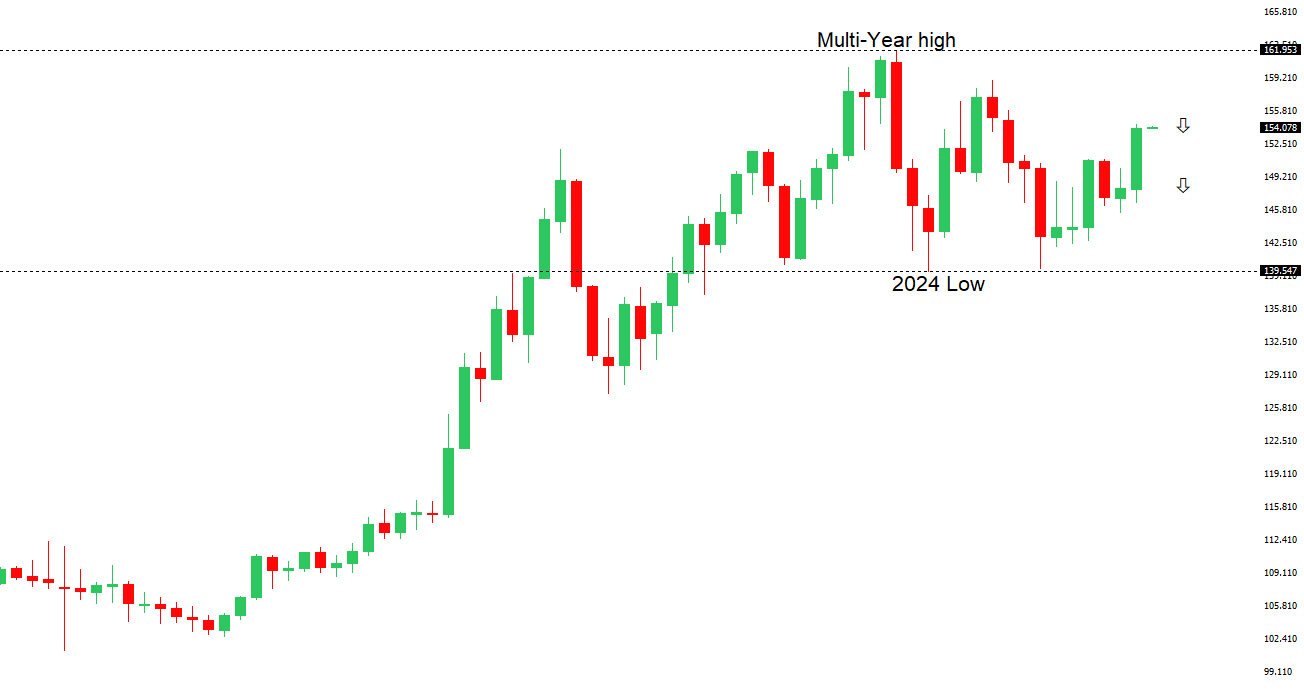

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, the door is now open for a deeper setback below the 2024 low at 139.58, exposing a retest of the 2023 low. Rallies should be well capped below 155.00. | ||

| ||

| R2 154.80 - 12 February high - Strong R1 154.49 - 4 November high - Medium S1 151.54 - 29 October low - Medium S2 149.38 - 17 October low - Strong | ||

| USDJPY: fundamental overview | ||

| PM Sanae Takaichi’s new national growth strategy, due next summer, stressed cautious monetary tightening and fiscal expansion, signaling prolonged ultra-loose policies and delaying BOJ rate hikes; markets reacted negatively, driving the yen to fresh lows against the dollar as traders sold it for carry trades. Finance Minister Satsuki Katayama issued urgent verbal warnings on currency moves, capping USDJPY amid global equity sell-offs, while two large US investment houses see no near-term intervention—last seen in 2024 at 158–162—unless volatility spikes. BOJ minutes showed a 7–2 vote to hold rates at 0.5%, with dissenters pushing hikes to anchor 2% inflation; Governor Ueda, facing his first split, signaled a potential December hike if wage momentum builds, as labor aims for >5% increases—September data Thursday (expected 2.5% YoY scheduled pay) will be key. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6629 - 1 October high - Strong R1 0.6618 - 29 October high - Medium S1 0.6458 - 5 November low - Medium S1 0.6440 - 14 October low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Reserve Bank of Australia held its cash rate steady at 3.60% this week, as widely expected, citing persistent core inflation, robust household spending, and a resurgent housing market as reasons to remain cautious on further easing amid economic uncertainty. With recent data signaling ongoing price pressures and no clear signals on future moves, markets see little chance of a December cut without sharper cooling in inflation and demand. The Australian dollar showed little reaction, staying weak amid broader risk-off sentiment fueled by AI bubble fears—highlighted by Michael Burry’s $1 billion+ put options on Nvidia and Palantir, plus bubble warnings from Morgan Stanley and Goldman Sachs CEOs—along with worries over the prolonged U.S. government shutdown. Unless risk aversion intensifies, AUDUSD is likely to stabilize. | ||

| Suggested reading | ||

| How Germany Became World’s Worst-Performing Economy, M. Moutii, AIER (November 3, 2025) Amid All This Enthusiasm, Cash May Be Wise, J. Calhoun, Alhambra (November 2, 2025) | ||