| ||

| 19th September 2025 | view in browser | ||

| Dollar recovery could be short-lived | ||

| Recent U.S. economic data shows a mixed picture: jobless claims dropped to 231,000, signaling labor market stability despite slower hiring due to tariff uncertainties and tighter immigration policies. | ||

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

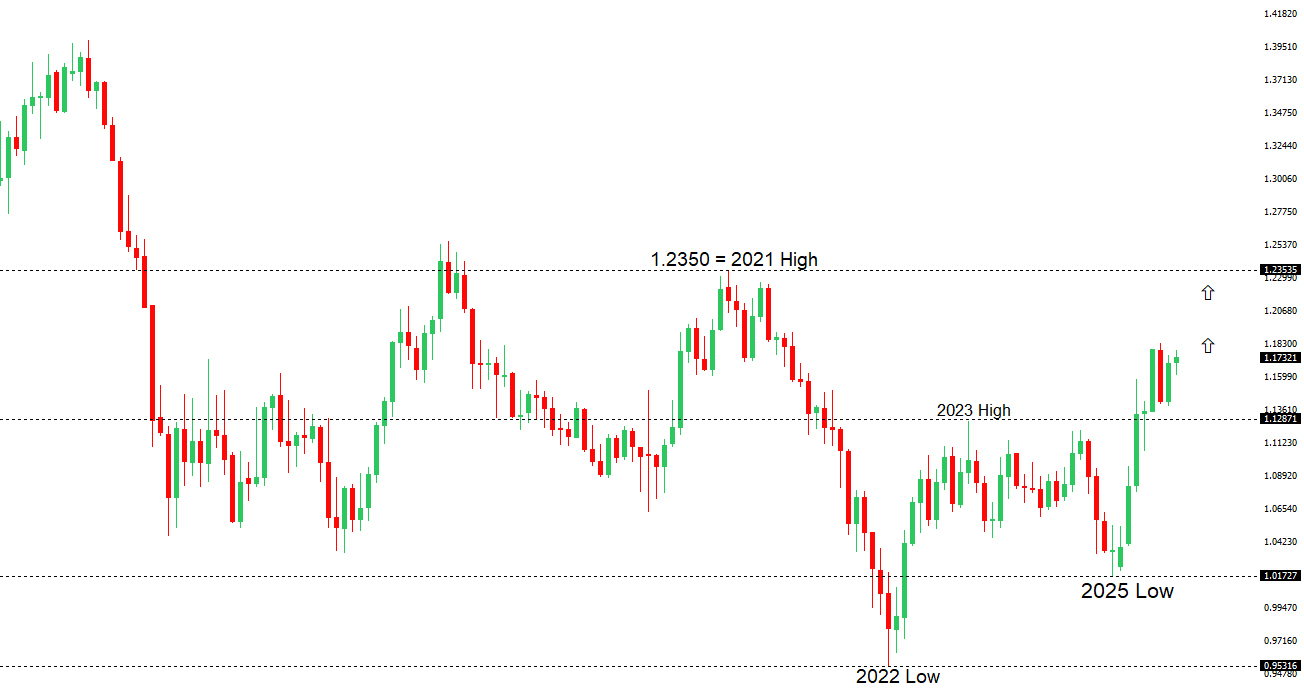

| EURUSD: technical overview | ||

| The Euro has broken out from a multi-month consolidation off a critical longer-term low. This latest push through the 2023 high (1.1276) lends further support to the case for a meaningful bottom, setting the stage for a bullish structural shift and the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.2000 - Psychological - Strong R1 1.1919 - 16 September/2025 high - Medium S1 1.1758 - 16 September low - Medium S2 1.1660 - 11 September low - Medium | ||

| EURUSD: fundamental overview | ||

| The euro recently dipped from a four-year high of 1.1919 after the U.S. Federal Reserve cut rates by 25 basis points and signaled two more cuts in 2025, though the broader uptrend from suggests this pullback may be temporary. Analysts now expect the European Central Bank to lean toward a rate hike by June 2026 rather than further cuts, driven by a strong euro and diverging monetary policies with the Fed, supporting a EURUSD trading range of 1.17–1.20. ECB official Jose Luis Escriva noted that U.S. policy shifts under President Trump could weaken the dollar’s global dominance, giving the euro a chance to gain ground if Europe modernizes its financial systems and introduces a digital currency. Meanwhile, Germany plans to triple borrowing to €425 billion in 2025, including €90.5 billion in Q4, to fund infrastructure and defense, moving away from fiscal restraint but risking higher interest costs and future budget challenges. Recent Eurozone data shows a weaker current account, improved construction output, and a low debt-to-GDP ratio, supporting Germany’s investment push despite potential financial pressures. | ||

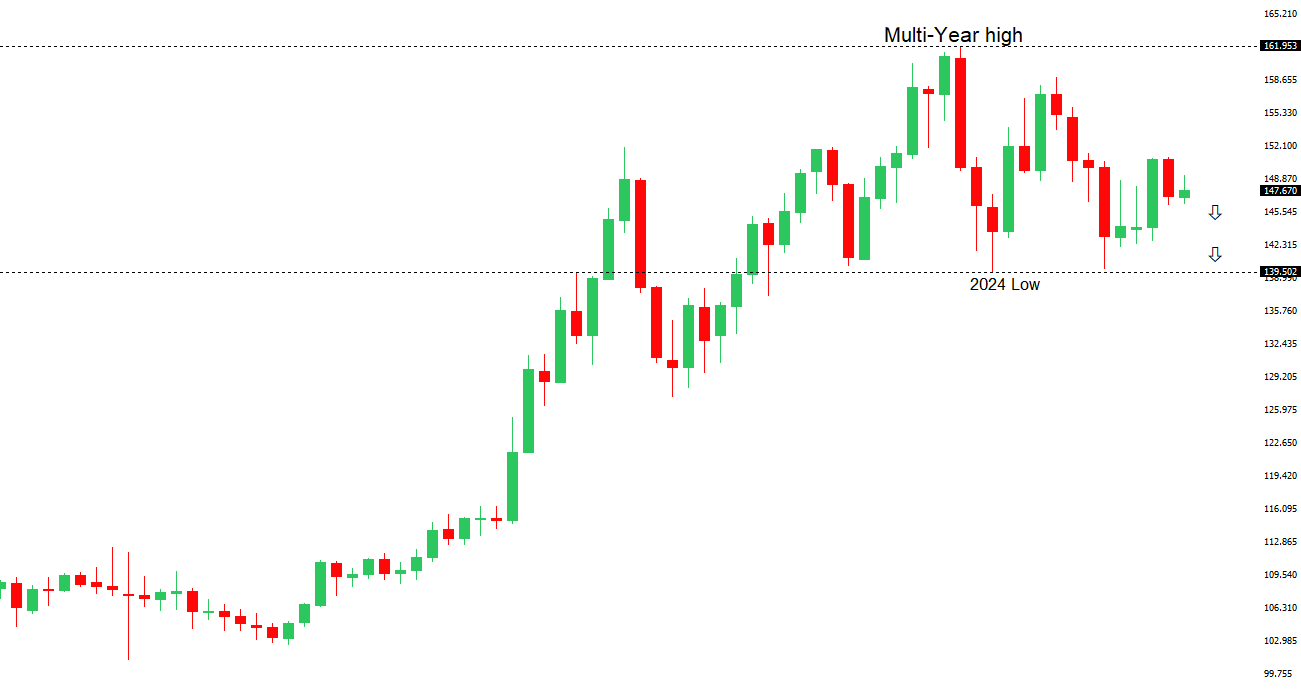

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, the door is now open for a deeper setback below the 2024 low at 139.58, exposing a retest of the 2023 low. Rallies should be well capped below 152.00. | ||

| ||

| R2 150.92 - 1 August high - Strong R1 149.14 - 3 September high - Medium S1 146.28 - 16 September low - Medium S2 145.48 - 17 September low - Strong | ||

| USDJPY: fundamental overview | ||

| The recent decline in the USDJPY exchange rate reversed after the Federal Reserve’s meeting prompted dollar short covering, with widening US-Japan yield gaps pushing the pair higher. The Bank of Japan maintained its 0.5% benchmark rate, though two dissenters and steady economic indicators, including 2.7% headline inflation and 3.3% core inflation, support expectations for a potential rate hike by October or December. Governor Ueda’s upcoming press conference will be closely watched for hints of tighter policy, which could strengthen the yen, especially if he signals a hawkish stance, though political uncertainties, like a potential Sanae Takaichi win in the LDP race, could favor continued easing and yen weakness. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6707 - 17 September/2025 high - Strong R1 0.6700 - Figure - Medium S1 0.6580 - 10 September low - Medium S1 0.6483 - 2 September low - Medium | ||

| AUDUSD: fundamental overview | ||

| Recent Australian labor data for August showed a cooling job market, with employment dropping by 5,400 (against an expected gain of 21,000) and the unemployment rate holding at 4.2%. A significant decline in full-time jobs (-40,900) was partially offset by part-time job gains (+35,500), while the participation rate fell to 66.8%, signaling reduced labor demand and workforce engagement. This weakening labor market, coupled with potential risks to household income and consumer spending, strengthens the case for the Reserve Bank of Australia to implement further rate cuts in November, following a recent cut to 3.60%. Despite a tight job market, the RBA is likely to adopt a cautious approach to balance economic growth and inflation, while a weaker USD supports Australia’s commodity-driven economy, presenting opportunities for AUDUSD appreciation. | ||

| Suggested reading | ||

| It’s Trump’s Federal Reserve Now, Wall Street Journal (September 17, 2025) A Seasonal Market Pattern Worth Observing, M. Hulbert, MarketWatch (September 18, 2025) | ||