| ||

| 8th May 2025 | view in browser | ||

| Fed holds rates, flags tariff risks | ||

| The Fed’s recent decision to hold rates steady has highlighted tariff-driven risks, with the Fed Chair noting potential short-lived inflation but signaling a data-dependent stance, as markets price in 77 basis points of cuts by year-end, likely delayed until Q3 when tariff impacts become clearer. | ||

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

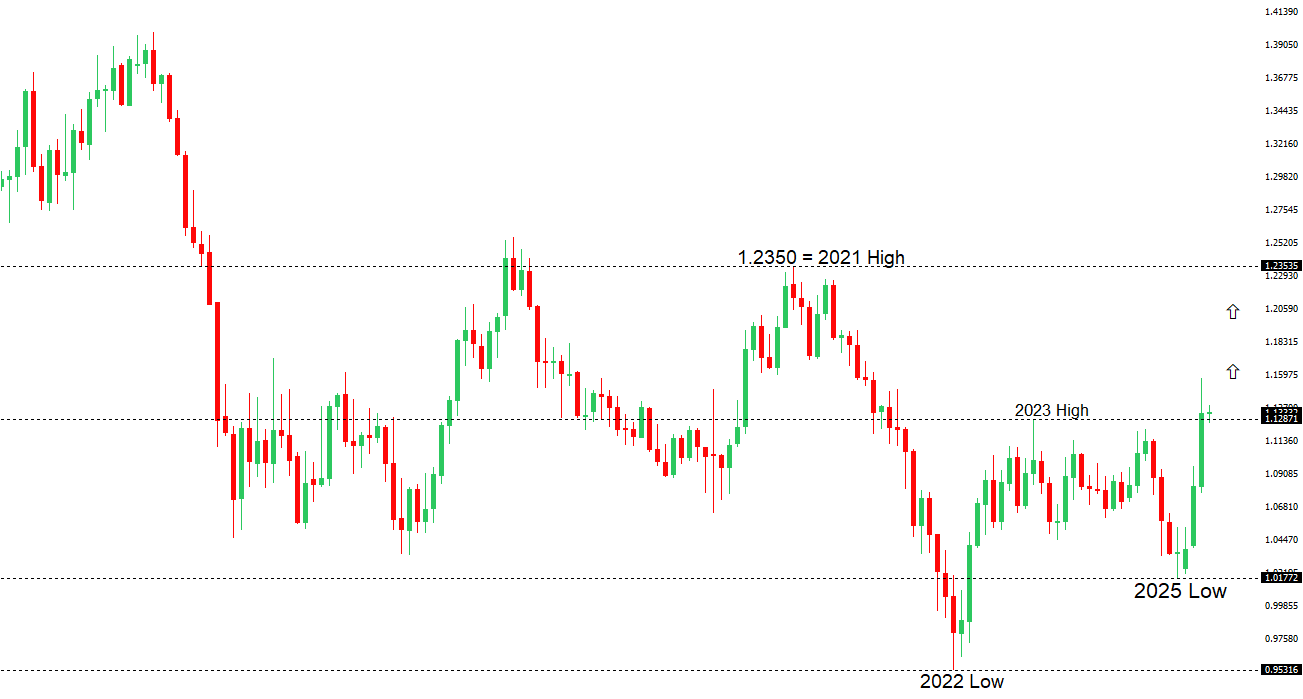

| EURUSD: technical overview | ||

| The Euro has finally broken out from a multi-month consolidation off a critical longer-term low. This latest push through the 2023 high lends further support to the case for a meaningful bottom, setting the stage for a bullish structural shift and the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported below 1.1000. | ||

| ||

| R1 1.1574 - 21 April/2025 high - Strong R1 1.1426 - 28 April high - Medium S1 1.1266 - 1 May low - Medium S2 1.1148 - 3 April high - Strong | ||

| EURUSD: fundamental overview | ||

| Asian currencies have paused their rally against the dollar, but the Bloomberg Asia Dollar Index’s clear uptrend suggests potential for further gains, possibly driving reserve flows into the Euro, Yen, and Gold as dollar-rich Asian nations look to hedge. Ukraine is contemplating shifting its currency, the hryvnia, from a dollar peg to a closer Euro alignment, reflecting its growing European ties and global trade fragmentation. In the Eurozone, March retail sales met expectations at -0.1% MoM and 1.6% YoY, signaling cautious consumer spending due to trade uncertainty and sluggish income growth, while Germany’s factory orders surged 3.6% MoM—exceeding the 1.3% forecast—hinting at industrial stabilization despite looming tariff threats, and its Construction PMI rose to 45.1, the highest in over two years, though still in contraction. | ||

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, the door is now open for a deeper setback below the 2024 low at 139.58 over the coming sessions exposing a retest of the 2023 low. Rallies should be well capped below 150.00. | ||

| ||

| R2 148.28 - 9 April high - Strong R1 145.93 - 2 May high - Medium S1 142.35 - 6 May low - Medium S1 141.97 - 29 April low - Medium | ||

| USDJPY: fundamental overview | ||

| The Bank of Japan’s March meeting minutes revealed a lack of consensus on the timing of future rate hikes, with board members expressing caution over the potential negative impacts of U.S. tariffs on Japan’s economy, some urging nimble action and others suggesting a shift to a neutral stance after a possible hike. Governor Ueda reaffirmed the BOJ’s intent to raise borrowing costs if economic projections hold, despite elevated inflation pressures, with outcomes heavily dependent on U.S.-Japan trade talks, where the U.S. has rejected Japan’s full tariff exemption, offering only to negotiate a reduction in the 14% Japan-specific tariff, though negotiator Ryosei Akazawa remains hopeful for a June agreement. The BOJ will release a summary of opinions from its April 30-May 1 meeting on May 13, shedding further light on its stance amid ongoing trade uncertainties. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6550 - 25 November high - Strong R1 0.6515 - 7 May/2025 high - Medium S1 0.6344 - 24 April low - Medium S1 0.6275 - 14 April low - Strong | ||

| AUDUSD: fundamental overview | ||

| We’ve seen some profit taking on the Australian Dollar as the U.S. and China begin trade war negotiations in Switzerland, with Treasury Secretary Bessent and China-skeptic negotiator Greer meeting Vice Premier He Lifeng. Outcomes remain uncertain and Trump, during David Perdue’s swearing-in as ambassador to China, denied U.S. initiation of talks and rejected tariff reductions. The ASEAN Plus Three group pledged to counter global trade shocks through increased regional trade, aligning with a broader Asian push to reduce dollar dependency, while the Bloomberg Asia Dollar Index’s pause doesn’t rule out further dollar hedging, potentially supporting the Yuan and, by extension, the Australian Dollar as a Yuan proxy. Certainly, China’s recent economic stimulus measures have been supporting the Australian Dollar as well. | ||

| Suggested reading | ||

| Can the office make a comeback?, Financial Times (May 6, 2025) Exclusive look at May’s Disruption Investor, S. McBride, RiskHedge (May 5, 2025) | ||