| ||

| 24th April 2026 | view in browser | ||

| Fragile calm into Friday | ||

| Markets remain cautiously defensive as geopolitical risks and higher oil keep the dollar supported, while focus shifts to key data from Germany, Canada and the US for fresh direction into the weekend. | ||

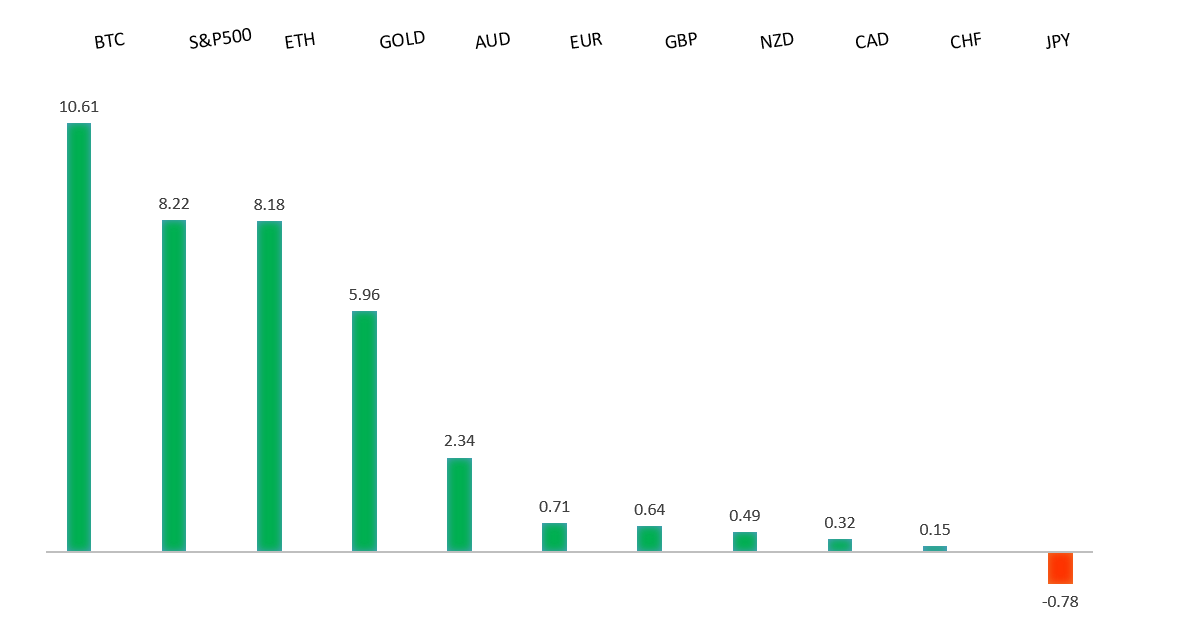

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

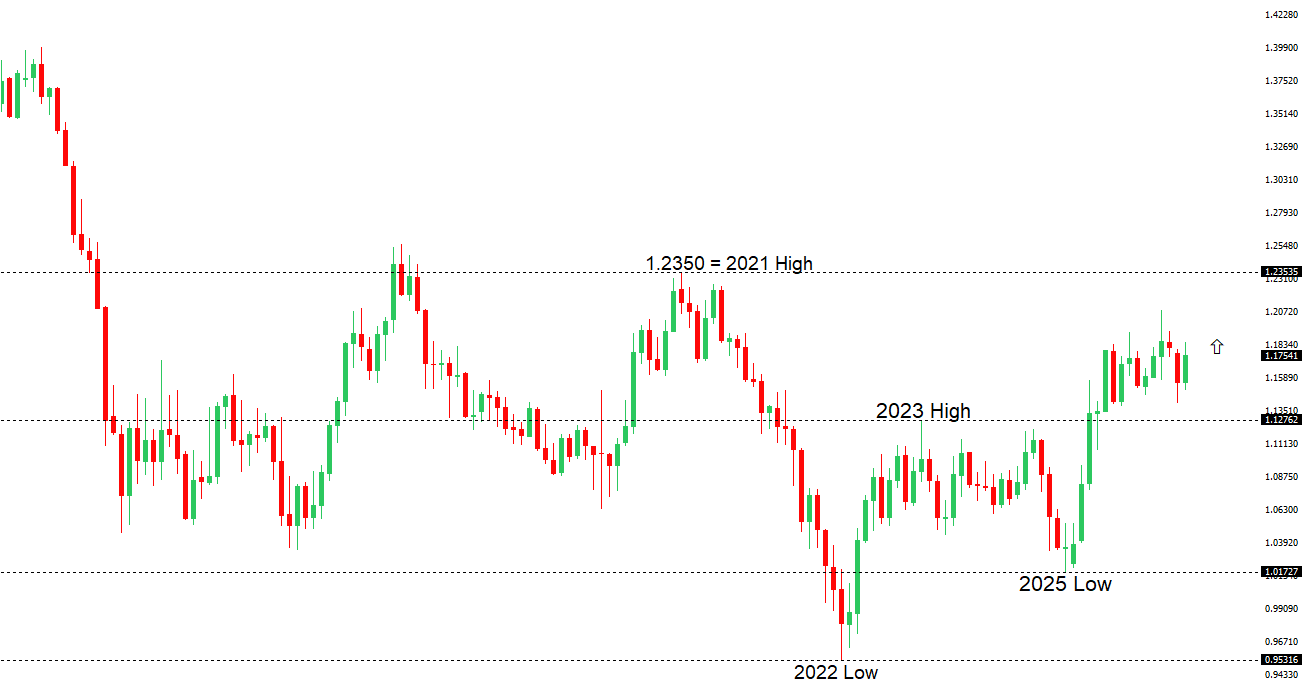

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1850 - 17 April high - Strong R1 1.1800 - Figure - Medium S1 1.1669 - 23 April low - Medium S2 1.1650 - 9 April low - Strong | ||

| EURUSD: fundamental overview | ||

| The euro has come under pressure as rising oil prices and renewed dollar strength amplify concerns around the eurozone’s vulnerability to geopolitical and energy shocks, particularly as maritime tensions around the Strait of Hormuz keep supply disruption risks elevated. Softer regional fundamentals have added to the downside bias, with recent PMI data pointing to contraction and weakening services momentum, while Germany’s downgraded growth outlook reinforces concerns that the region is slipping toward a stagflationary mix of weak growth and sticky inflation. Against that backdrop, the European Central Bank remains constrained, with limited scope to offer support as growth deteriorates and energy risks linger, leaving the euro pressured by both deteriorating domestic fundamentals and widening divergence against a dollar supported by higher yields and safe-haven demand. | ||

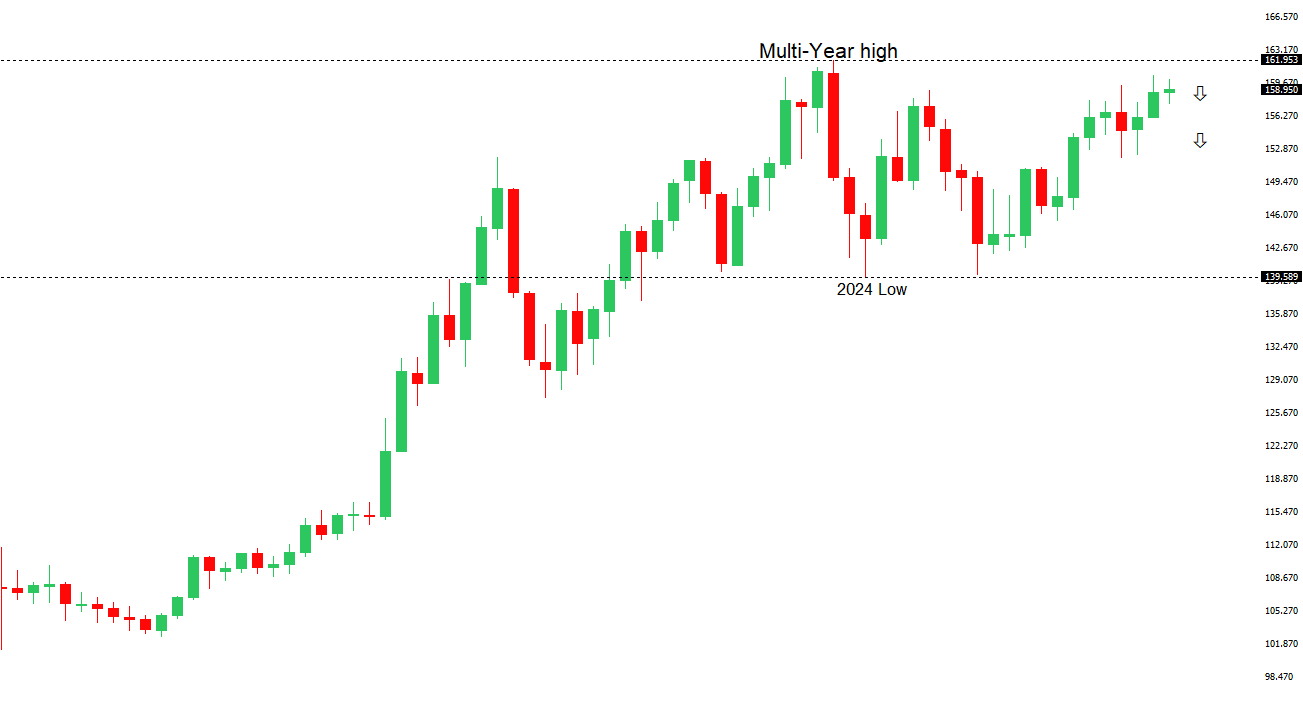

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped above 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 160.00 negates. | ||

| ||

| R2 160.46 - 30 March/2026 high - Strong R1 160.03 - 7 April high - Medium S1 158.00 - Figure - Medium S2 157.51 - 19 March low - Strong | ||

| USDJPY: fundamental overview | ||

| The yen has remained under pressure as rising Middle East tensions and elevated oil prices worsen Japan’s terms-of-trade outlook, reinforcing a fundamental headwind for a major energy importer and weighing on the currency. At the same time, expectations for an imminent Bank of Japan rate hike have been pushed back as policymakers adopt a more cautious stance amid geopolitical uncertainty, narrowing support for the yen even as markets still look for a hawkish signal later this year. The move in USDJPY toward 160 has also kept intervention risk in focus, with Japanese officials stepping up rhetoric to lean against excessive currency weakness, while firmer US yields and resilient dollar demand have added to policy divergence pressures, leaving the yen caught between external headwinds, delayed tightening expectations, and intermittent support from intervention concerns. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7222 - 17 April/2026 high - Strong R1 0.7200 - Figure - Medium S1 0.7111 - 23 April low - Medium S2 0.6963 - 8 April low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar has softened as renewed geopolitical caution has weighed on broader risk sentiment, pressuring high-beta currencies as investors rotate more defensively amid uncertainty around the Middle East ceasefire and rising energy risks. At the same time, focus is building on upcoming inflation data, with Australia’s Q1 CPI seen as a key test for the Reserve Bank of Australia policy outlook, where a firm print could reinforce expectations for a more hawkish stance and offer support to the currency. For now though, external headwinds—including a firmer US dollar, cautious global sentiment, and concern around China-linked growth demand—are dominating, leaving the Aussie trading defensively even as domestic policy expectations remain an important medium-term anchor. | ||

| Suggested reading | ||

| Stocks Are At All-Time Highs For Good Reason, S. Varghese, Carson Group (April 22, 2026) Why Tariffs Won’t Fix China’s Trade Surplus, C. Packard, Cato (April 22, 2026) | ||