| ||

| 23rd April 2026 | view in browser | ||

| Uncertainty lingers, data looms | ||

| Macro remains cautious with euro weakness, steady dollar tone, and geopolitics driving volatility, as markets look ahead to key global PMI data and US indicators for direction. | ||

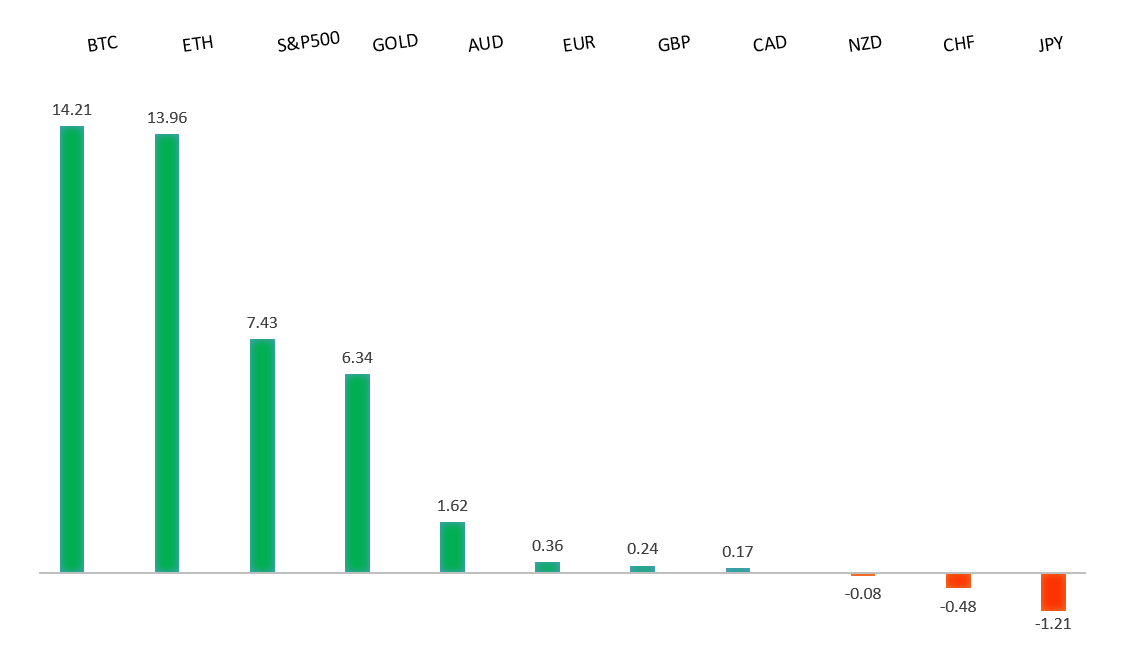

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

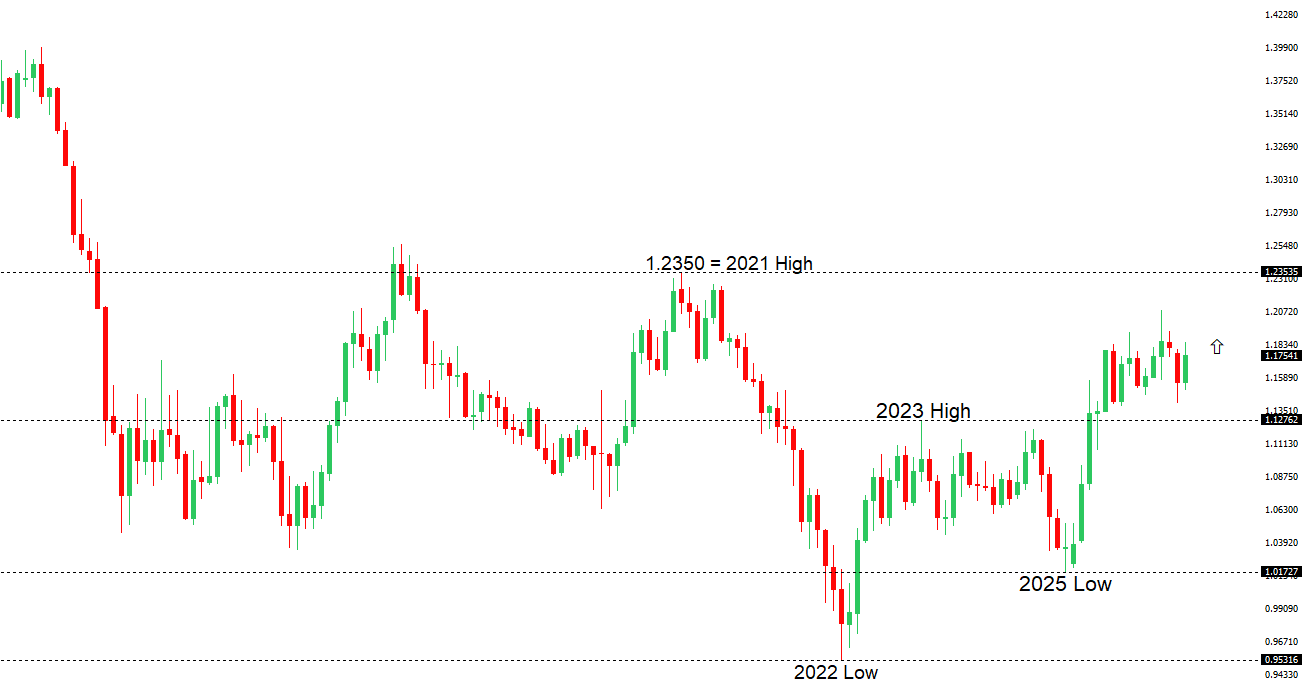

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1850 - 17 April high - Strong R1 1.1800 - Figure - Medium S1 1.1677 - 10 April low - Medium S2 1.1650 - 9 April low - Strong | ||

| EURUSD: fundamental overview | ||

| The euro is trading heavy across the board, pressured by a combination of deteriorating growth expectations and elevated geopolitical risk, with Germany’s downgrade to its outlook reinforcing concerns about the region’s economic momentum. At the same time, the European Central Bank remains sidelined amid persistent uncertainty, limiting policy support for the currency, while Middle East tensions continue to weigh on sentiment and amplify downside risks through energy channels. Price action has also been shaped by large option expires anchoring key levels in EURUSD and other crosses, helping to contain volatility but reinforcing a soft tone, with only EURCHF showing relative resilience amid signs of potential Swiss National Bank involvement to curb franc strength. | ||

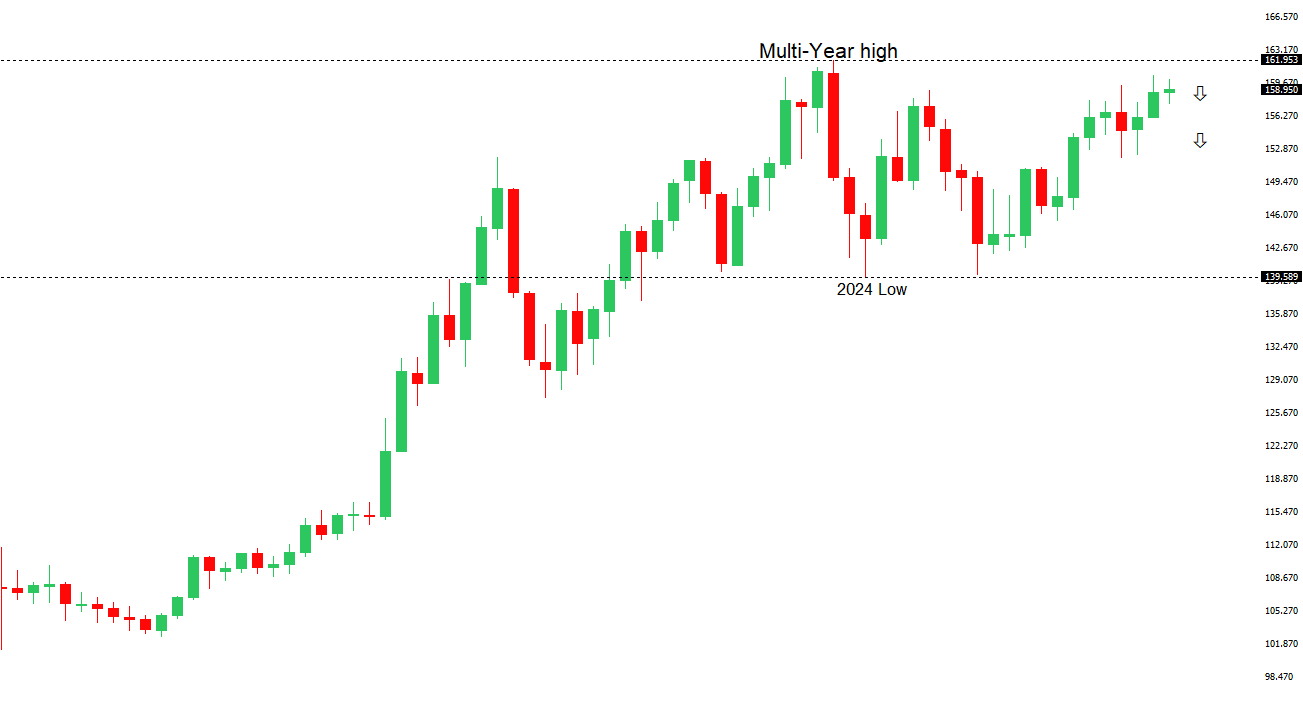

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped above 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 160.00 negates. | ||

| ||

| R2 160.46 - 30 March/2026 high - Strong R1 160.03 - 7 April high - Medium S1 158.00 - Figure - Medium S2 157.51 - 19 March low - Strong | ||

| USDJPY: fundamental overview | ||

| The yen has been trading in a choppy, mixed fashion today, with macro headwinds still dominating. Higher oil prices and ongoing disruptions around the Strait of Hormuz continue to weigh by worsening Japan’s terms of trade, while intermittent geopolitical headlines—such as talk of a US–Iran ceasefire extension—have offered only brief support via a softer dollar. Today’s stronger-than-expected Japan flash manufacturing PMI, which showed the fastest expansion in several years, has had limited positive impact, as the strength appears driven more by front-loaded production tied to supply-chain concerns than underlying demand. Overall, the yen remains on the back foot, with energy dynamics and persistent policy divergence between the Fed and the Bank of Japan continuing to drive the narrative. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7222 - 17 April/2026 high - Strong R1 0.7200 - Figure - Medium S1 0.7115 - 20 April low - Medium S2 0.6963 - 8 April low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar has been trading defensively, weighed by a combination of geopolitical risk and shifting domestic dynamics, with the Iran conflict driving heightened currency volatility and prompting a sharp increase in hedging activity among Australian corporates and super funds. This surge in hedging demand reflects growing concern about downside AUD risk, particularly given Australia’s sensitivity to global commodity prices and external shocks. While domestic data has shown some resilience, including improved PMI readings, the broader tone is being capped by cautious global sentiment and expectations that the Reserve Bank of Australia will remain measured in its policy stance. At the same time, ongoing strength in the US dollar and uncertainty around China-linked demand continue to limit upside momentum, leaving the AUD pressured and highly reactive to shifts in global risk appetite. | ||

| Suggested reading | ||

| Good Investors Require Distinguishing Good & Bad Growth, C. Wood, Grow or Die (April 21, 2026) When Risk and Fear Rally Together: The Stock/Gold Conundrum, T. Wilson, RCM (April 22, 2026) | ||