| ||

| 9th April 2026 | view in browser | ||

| Geopolitics dominate as ceasefire resets market tone | ||

| Global markets have been running with a clear risk-on tone, driven almost entirely by the landmark US-Iran two-week ceasefire agreement tied to the reopening of the Strait of Hormuz. This diplomatic breakthrough has rapidly removed the geopolitical risk premium that had been weighing on sentiment for weeks, shifting flows decisively away from safe-haven assets and into riskier ones. | ||

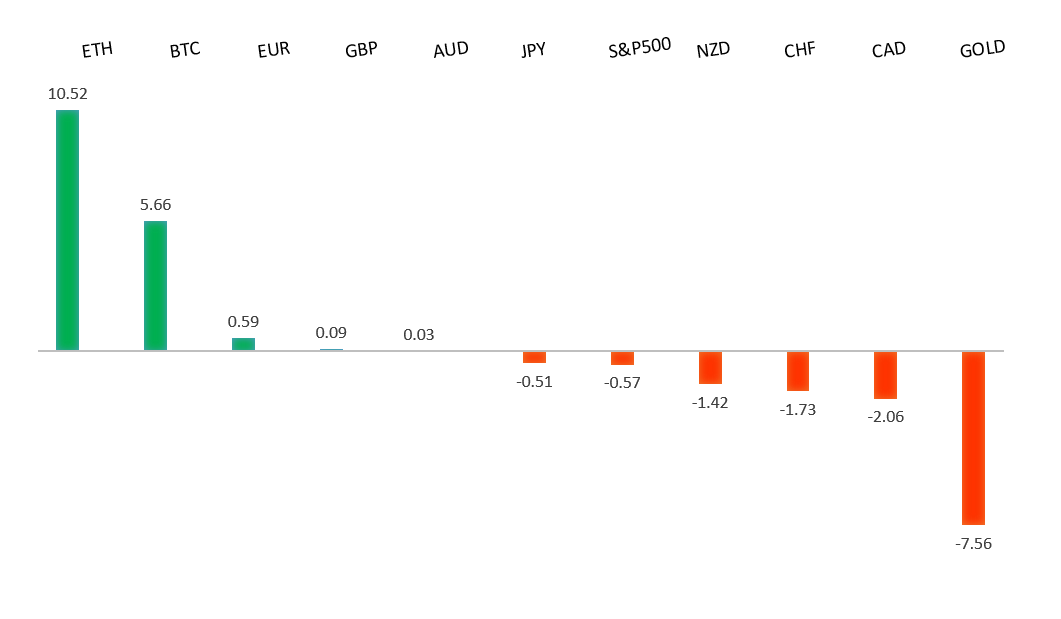

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1722 - 8 April high - Strong R1 1.1700 - Figure - Medium S1 1.1590 - 8 April low - Medium S2 1.1504 - 3 April low - Strong | ||

| EURUSD: fundamental overview | ||

| The euro has been primarily supported by diplomatic breakthroughs in the Middle East, including a US-Iran agreement on a two-week ceasefire that includes potential reopening of the Strait of Hormuz, which has eased safe-haven demand for the US dollar and lowered fears of prolonged energy price shocks weighing on eurozone growth. This geopolitical de-escalation has been reinforced by resilient eurozone economic signals, such as moderate inflation around 2.5% driven by prior energy pressures, helping sustain the European Central Bank’s relatively cautious and data-dependent stance compared to mixed US indicators and ongoing Federal Reserve rate path uncertainty. Overall, reduced geopolitical risk premiums have shifted flows in favor of the euro on fundamental grounds. | ||

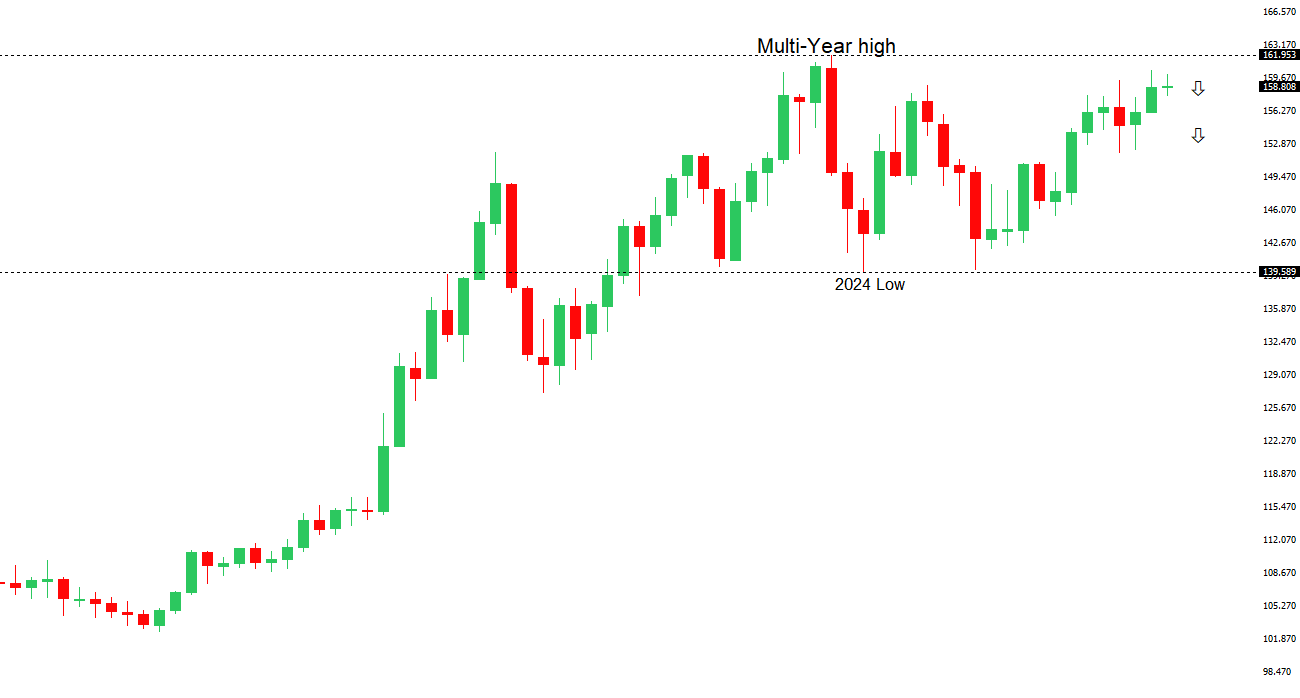

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped above 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 160.00 negates. | ||

| ||

| R2 160.46 - 30 March/2026 high - Strong R1 160.03 - 7 April high - Medium S1 157.89 - 8 April low - Medium S2 157.51 - 19 March low - Strong | ||

| USDJPY: fundamental overview | ||

| The yen has been primarily supported by diplomatic breakthroughs in the Middle East, including a US-Iran agreement on a two-week ceasefire with potential reopening of the Strait of Hormuz, which has eased geopolitical tensions, reduced safe-haven flows into the dollar, and lowered concerns over prolonged high energy prices that heavily burden Japan’s import-dependent economy. This de-escalation has offset some pressure from elevated oil costs and helped temper fears of imported inflation, while expectations of a near-term Bank of Japan rate hike and official warnings against excessive yen weakness have provided additional fundamental backing. Overall, the reduced risk premium from geopolitics has shifted flows in favor of the yen against the backdrop of persistent US dollar strength and mixed domestic economic signals. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7188 - 11 March/2026 high - Strong R1 0.7085 - 8 April high - Medium S1 0.6963 - 8 April low - Medium S2 0.6833 - 30 March low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar has been primarily supported by diplomatic breakthroughs in the Middle East, including a US-Iran agreement on a two-week ceasefire with potential reopening of the Strait of Hormuz, which has eased geopolitical tensions, boosted global risk sentiment, and lowered oil prices sharply. This development has reduced safe-haven demand for the US dollar while alleviating imported inflation pressures for Australia and supporting its commodity export outlook through improved risk appetite. The relief has complemented the Reserve Bank of Australia’s hawkish stance, with recent rate hikes to 4.10% and market expectations for potential further tightening in May amid still-elevated domestic inflation, helping sustain the AUD against mixed US economic signals and Federal Reserve policy uncertainty. Overall, the geopolitical de-escalation has shifted fundamental flows in favor of the risk-sensitive Australian dollar. | ||

| Suggested reading | ||

| The Upper Middle Class Trap, N. Maggiulli, Of Dollars and Data (April 7, 2026) Memories Of Good Investments, J. Klement, Klement on Investing (April 7, 2026) | ||