| ||

| 3rd June 2025 | view in browser | ||

| Global trade tensions and monetary policy shifts | ||

| The US dollar and bonds remain weak as fears of “de-dollarization” persist, driven by escalating trade tensions and the proposed “One Big Beautiful Bill,” which includes Section 899 allowing taxes on foreign holders of US treasuries from countries with “unfair” tax practices. | ||

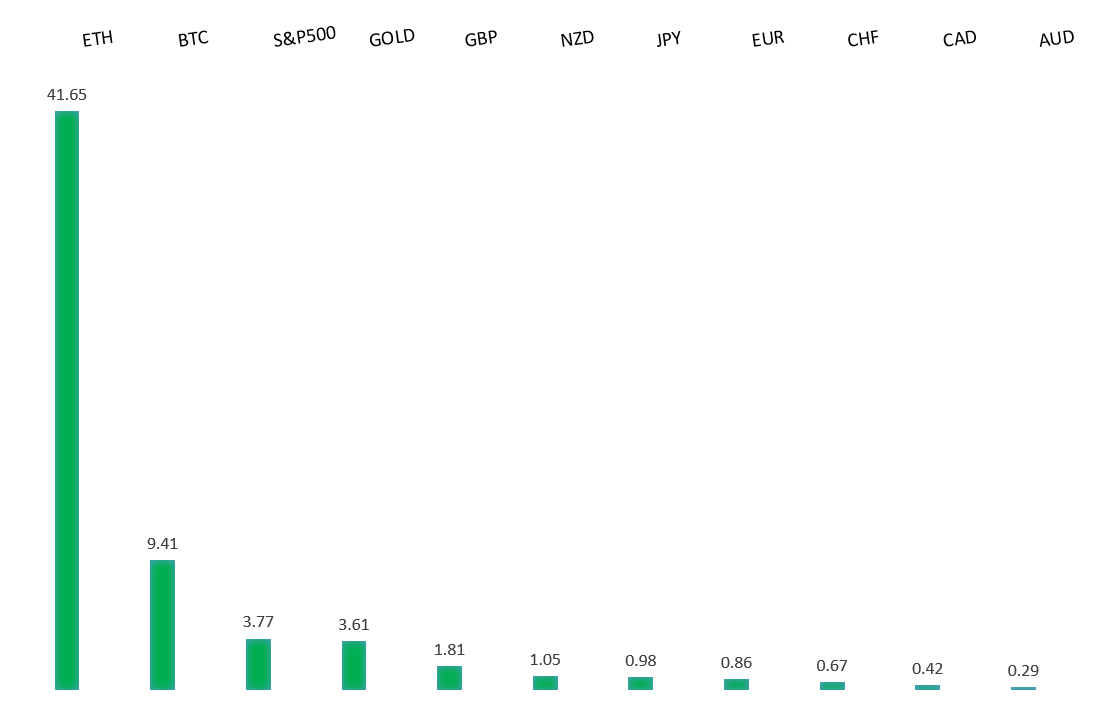

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro has finally broken out from a multi-month consolidation off a critical longer-term low. This latest push through the 2023 high lends further support to the case for a meaningful bottom, setting the stage for a bullish structural shift and the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported below 1.1000. | ||

| ||

| R2 1.1474 - 11 April high - Medium R1 1.1455 - 3 June high - Medium S1 1.1210 - 29 May low - Medium S2 1.1065 - 12 May low - Strong | ||

| EURUSD: fundamental overview | ||

| The European Central Bank is likely to cut interest rates on Thursday to counter trade tensions and slowing economic growth, as inflation nears the ECB’s 2% target. Market expectations suggest a total of 56 basis points in rate cuts this year, potentially lowering rates to 1.75%, with the ECB nearing the end of its rate-cutting cycle. As the ECB eases, the Fed may also begin loosening policy later in 2025, potentially narrowing the interest rate gap and supporting the euro. The EU has criticized Trump’s proposed 50% tariffs on steel and aluminum, warning of retaliatory measures if trade talks fail. | ||

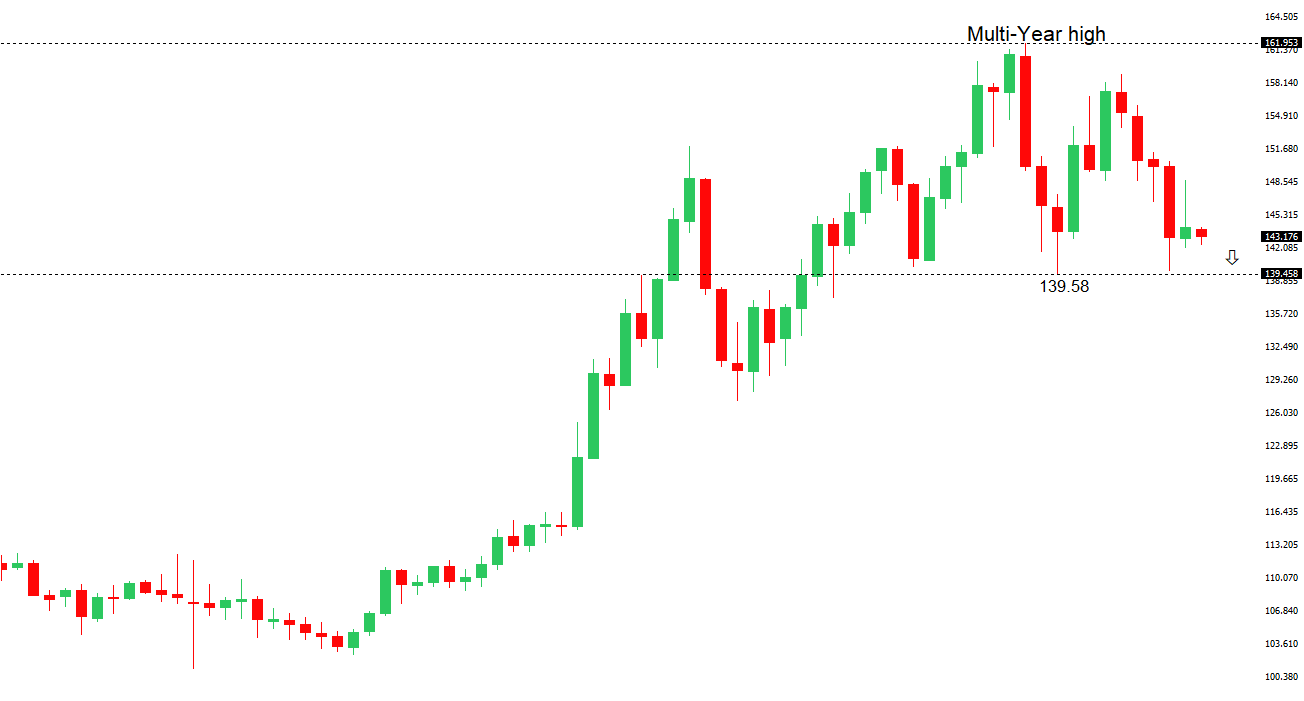

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, the door is now open for a deeper setback below the 2024 low at 139.58 over the coming sessions exposing a retest of the 2023 low. Rallies should be well capped below 150.00. | ||

| ||

| R2 148.65 - 12 May high - Medium R1 146.29 - 29 May high - Medium S1 142.11 - 27 May low - Medium S2 141.97 - 29 April low - Medium | ||

| USDJPY: fundamental overview | ||

| The Yen has been gaining strength from safe-haven flows as markets react to President Trump’s proposed tariff hike on steel and aluminum from 25% to 50%, highlighting ongoing trade tensions with China. The Bank of Japan is preparing for higher interest rates by setting aside full provisions for bond transaction losses, signaling a shift from ultra-loose monetary policy, which could boost Yen demand as higher Japanese government bond yields attract capital. However, former BOJ board member Makoto Sakurai suggests that if JGB yields surge, the BOJ may pause its gradual reduction of bond purchases, while Governor Ueda’s cautious remarks indicate that trade uncertainties and economic impacts could delay rate hikes until late 2025, pending clearer data on business investment and wage growth. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6550 - 25 November 2024 high - Strong R1 0.6538 - 26 May/2025 high - Medium S1 0.6344 - 24 April low - Medium S1 0.6275 - 14 April low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar is attempting to hold gains above its 200-day moving average amid broad U.S. dollar weakness, but caution persists due to China’s Caixin Manufacturing PMI slipping into contraction and dovish Reserve Bank of Australia Minutes suggesting a potential 50bps rate cut as a buffer against global trade risks. Australia’s Q1 2025 GDP is expected to grow 0.4% quarter-on-quarter, down from 0.6%, with modest improvement forecast in coming quarters, supported by potential further RBA easing to boost consumer demand and housing. However, weaker-than-expected Q1 company profits and a wider current account deficit may temper business investment, though a stronger-than-expected inventory build offers a slight boost to GDP. | ||

| Suggested reading | ||

| Why the A.I. Job Apocalypse May Already Be Here, K. Roose, NY Times (May 30, 2025) Trump Cannot Quiet Reality, Neither Can the Federal Reserve, J. Tamny, Forbes (June 1, 2025) | ||