| ||

| 12th March 2026 | view in browser | ||

| Oil risk premium returns, dollar firms | ||

| Oil is back on the bid amid escalating Middle East tensions and tanker attacks, boosting the U.S. dollar and putting USDJPY near intervention-watch levels, while markets turn to U.S. jobless claims and key global data for the next macro signal. | ||

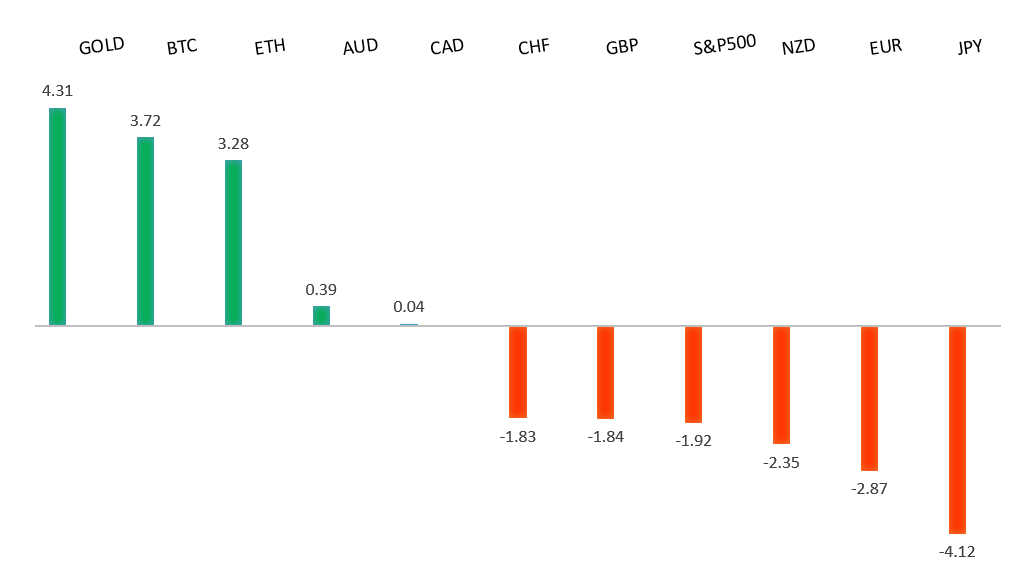

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1400. | ||

| ||

| R2 1.1707 - 3 March high - Strong R1 1.1668 - 10 March high - Medium S1 1.1507 - 9 March/2026 low - Medium S2 1.1469 - 5 November low - Strong | ||

| EURUSD: fundamental overview | ||

| The euro is back under pressure into Thursday, though price action remains largely range-bound. The macro backdrop has turned slightly more supportive for the euro as the Iran war revives inflation concerns just as the ECB believed conditions were stabilizing. Comments from Peter Kazimir warning that upside inflation risks now “clearly dominate” have prompted markets to price in the possibility of an ECB rate hike by mid-year, with talk of further easing fading. Meanwhile, Isabel Schnabel reiterated that policy is currently in a “good place” but flagged the conflict as an upside inflation risk through energy prices, suggesting policymakers will likely stay on hold for now. Even with potential oil supply relief from coordinated reserve releases, persistent energy volatility and rising inflation expectations point to a higher euro inflation risk premium and a comparatively less dovish ECB than the Fed in the quarters ahead. | ||

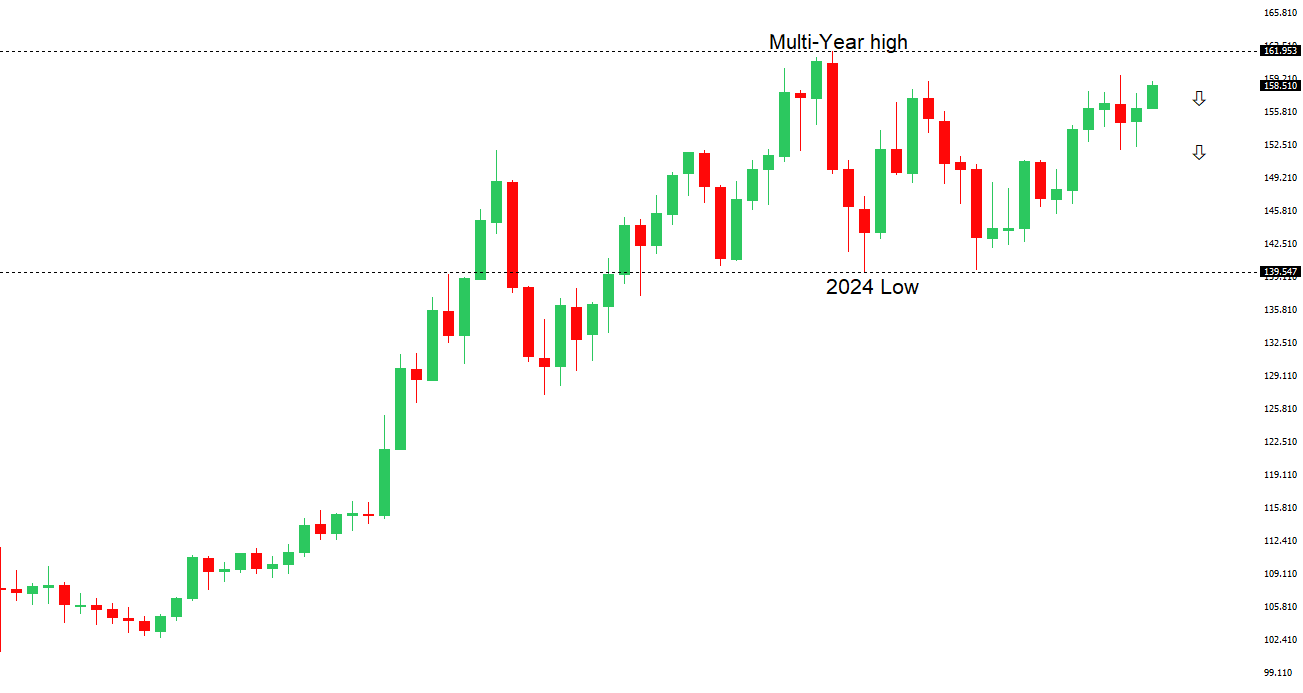

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped ahead of 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. | ||

| ||

| R2 159.46 - 14 January/2026 high - Strong R1 159.24 - 12 March high - Medium S1 157.27 - 10 March low - Medium S2 156.45 - 5 March low - Strong | ||

| USDJPY: fundamental overview | ||

| The major pair is holding just below the January 14 YTD high of 159.45 as the yen continues to struggle. Japan’s decision to release 80 million barrels from its strategic reserves as part of a coordinated IEA effort highlights policymakers’ focus on containing energy-driven inflation amid Middle East tensions, though the yen remains weighed down by Japan’s heavy reliance on imported energy. Business sentiment has softened slightly but remains expansionary, while higher oil prices and stagflation pressures are reinforcing expectations for more fiscal support. At the same time, strong demand at the latest 5-year JGB auction and softer rate-hike expectations have capped yields, keeping policy divergence and carry dynamics tilted against the yen, with markets still comfortable holding USDJPY despite intervention warnings. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7200 - Figure - Medium R1 0.7188 - 11 March/2026 high - Medium S1 0.6944 - 3 March low - Medium S2 0.6897 - 6 February low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar is cooling off today, giving back Wednesday’s gain that had taken the currency to its highest level against the Buck since June 2022. Still, expectations for a near-term RBA rate hike continue to provide support into dips. Consumer inflation expectations rose to 5.2% in March, the highest since July 2023, while CPI remains above the RBA’s target and risks remain skewed higher amid the recent oil supply shock. With inflation projected to stay elevated for longer and major banks now anticipating a 25bp hike next week, markets are pricing roughly a 70% chance of tightening, helping underpin AUD strength alongside strong commodity prices and a widening Australia–U.S. yield spread. | ||

| Suggested reading | ||

| Why Is It So Hard to Predict Financial Markets?, J. Wiggins, Behavioural Investment (March 10, 2026) Five Scenarios For How The War With Iran Might End, H. Scribner, Axios (March 10, 2026) | ||