| ||

| 23rd February 2026 | view in browser | ||

| Tariff shock weighs on dollar | ||

| Global markets start the day with the dollar under pressure following the US tariff ruling, oil softer amid renewed geopolitical tensions, and incoming data from Europe and the US reinforcing a fragile but still expanding global economy against a backdrop of ongoing trade and political uncertainty. | ||

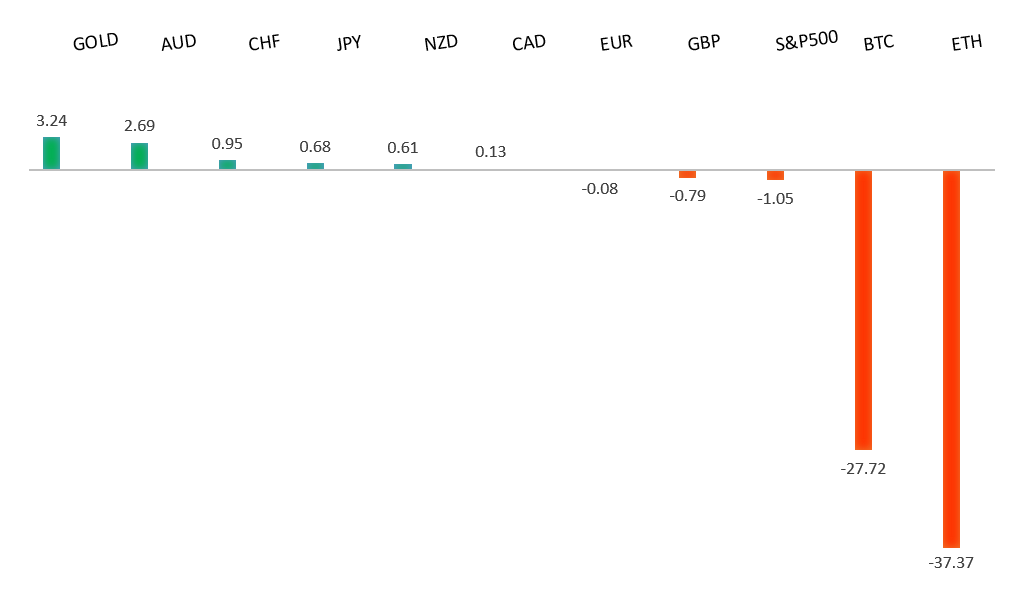

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1500. | ||

| ||

| R2 1.2081 - 27 Janaury/2026 high - Strong R1 1.1929 - 10 February high - Medium S1 1.1742 - 19 February low - Medium S2 1.1728 - 23 January low - Medium | ||

| EURUSD: fundamental overview | ||

| Euro-area data and market pricing suggest the euro remains mildly constructive but vulnerable in the near term, with downside risks increasingly driven by geopolitics and US trade policy rather than domestic fundamentals. Rising US-Iran tensions, elevated war risks in Europe, and renewed tariff uncertainty have strengthened the dollar’s safe-haven appeal, while options markets show growing demand for downside euro protection. Many analysts warn EURUSD could drift lower toward the mid-1.16 area if geopolitical tensions or trade pressures intensify, with rallies likely capped unless external risks ease. Meanwhile, upcoming euro-area data—particularly Germany’s IFO survey—is expected to show only modest improvement, reinforcing the view of a fragile, sideways economy rather than a clear recovery. | ||

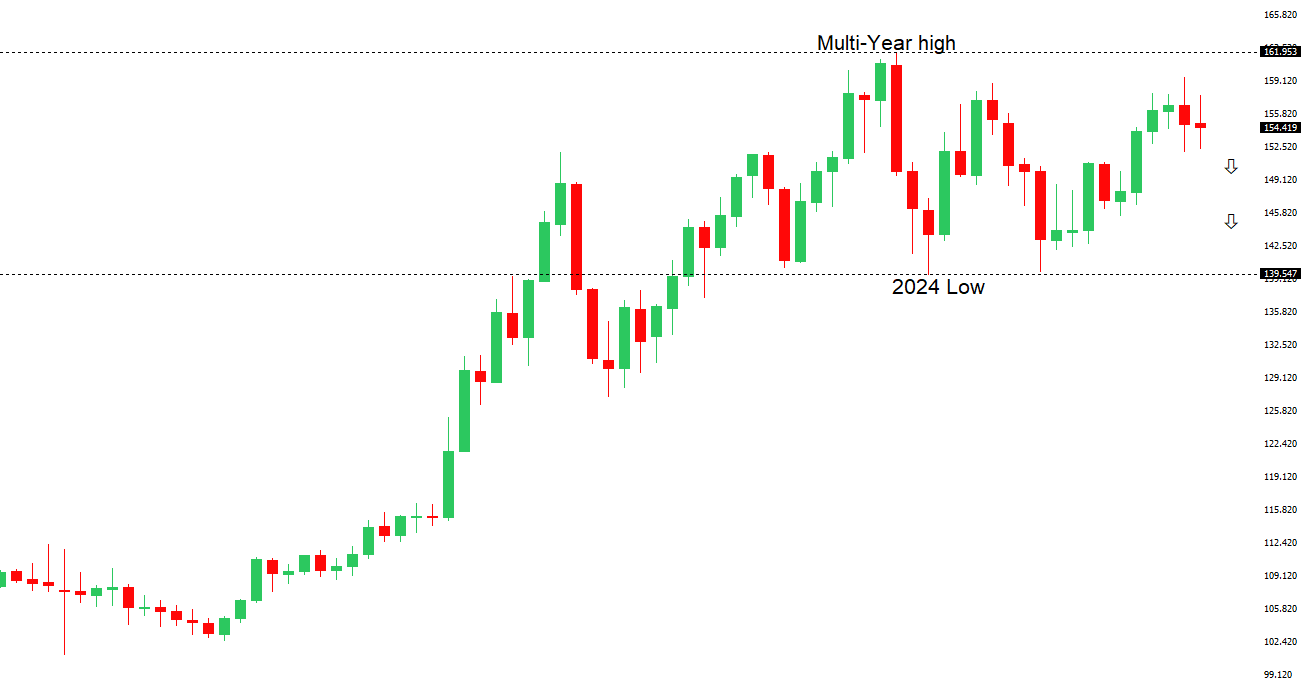

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, rallies should be well capped ahead of 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. The recent break below 154.39 strengthens the outlook. | ||

| ||

| R2 156.30 - 10 February high - Medium R1 155.65 - 20 February high - Medium S1 152.24 - 12 February low - Medium S2 151.97 - 28 January/2026 low - Strong | ||

| USDJPY: fundamental overview | ||

| USDJPY remains supported above the late-January low after pulling back from its early-February peak, with price now consolidating around 155. Prime Minister Sanae Takaichi’s first major policy speech signaled a shift away from austerity toward more expansionary, investment-led fiscal policy, though framed carefully to reassure markets about debt sustainability and currency stability. While the outlook is seen as mildly negative for the yen over time due to looser fiscal conditions, her emphasis on stability and caution against excessive weakness may limit downside risks. Meanwhile, former BOJ official Makoto Sakurai noted the central bank could raise rates as early as March if yen depreciation intensifies, with gradual tightening expected longer term as policymakers balance inflation risks against financial stability concerns. Key upcoming data include Tokyo CPI and Retail Sales, which could influence policy expectations. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7158 - 2023 high - Strong R1 0.7147 - 12 February/2026 high - Strong S1 0.7007 - 9 February low - Medium S2 0.6897 - 6 February low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian Dollar continues to find strong support above the 9 February low, with consistent buying seen, leaving room for a rebound toward the 0.7147–0.7158 area if this base holds. Australia’s labor market remains tight, with unemployment at 4.1%, solid job gains, and firm wage growth, reinforcing concerns that inflation pressures will persist. Combined with ongoing fiscal support and expectations that the RBA may raise rates further—potentially keeping them above those in the U.S.—the policy outlook favors the AUD, especially as USD sentiment has softened amid tariff-related uncertainty and shifting Fed expectations. Near-term direction will hinge on upcoming Australian inflation data and guidance from the RBA Governor, both critical for shaping expectations around additional tightening or a pause. | ||

| Suggested reading | ||

| Market Effects of War With Iran: Likely Immaterial, Fisher Investments (February 20, 2026) What to Make of This Very Weird Market, J. Mackintosh, The Wall Street Journal (February 19, 2026) | ||