| ||

| 28th October 2025 | view in browser | ||

| US-China thaw sparks risk-on rally | ||

| A recent “very successful” framework agreed by U.S. and Chinese officials for the upcoming Trump-Xi summit in South Korea has sparked optimism, lifting risk assets and raising hopes for a meaningful easing of trade tensions, with both leaders also planning follow-up talks in Washington and Beijing and even reviewing a global peace framework. | ||

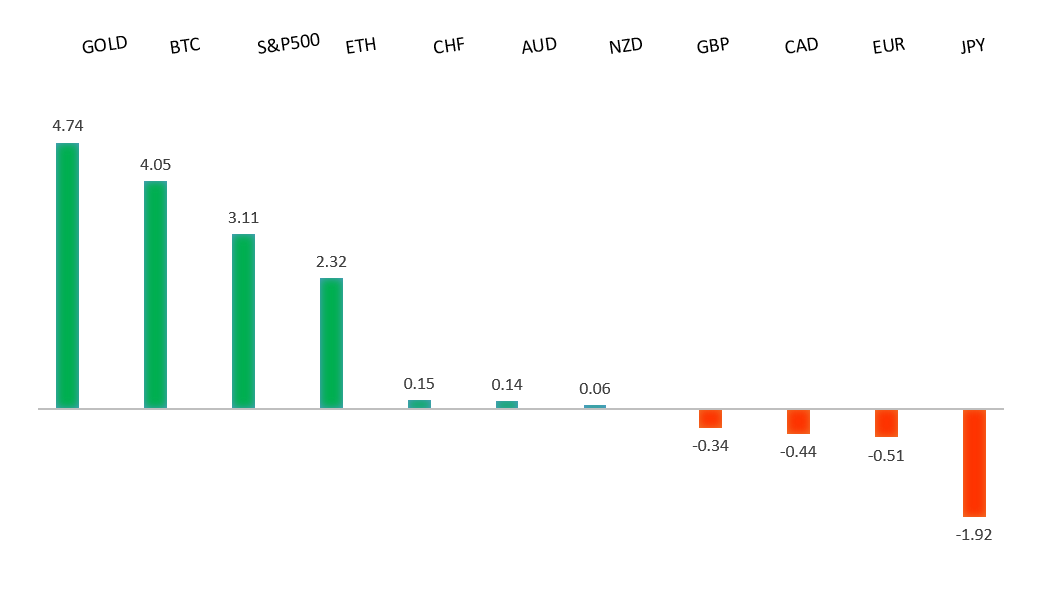

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

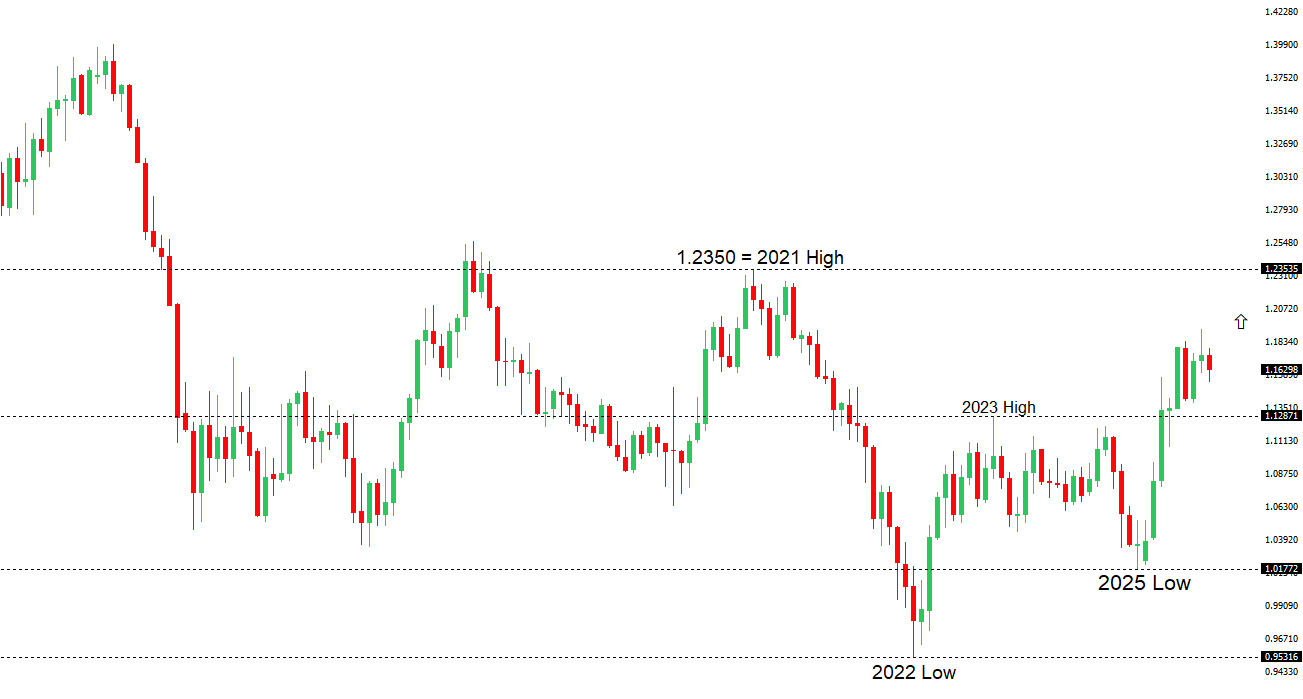

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1779 - 1 October high -Strong R1 1.1729 - 17 October high - Medium S1 1.1542 - 9 October low - Medium S2 1.1528 - 5 August low - Strong | ||

| EURUSD: fundamental overview | ||

| The ECB is confident in its “Goldilocks” scenario, expecting U.S. tariff effects to be short-lived and offset by Germany’s fiscal stimulus, supporting unchanged rates at the October 30 meeting, with President Lagarde likely to stress policy is “in a good place”—signaling stability, patience, and inflation largely under control—while cautioning on geopolitical risks; this ECB-Fed rate divergence and anticipated U.S.-China trade de-escalation should keep EURUSD bullish. German business sentiment improved in October, with the Ifo index rising to 88.4 (above forecasts) on stronger future expectations led by services, aligning with PMI data showing the fastest private-sector growth in over two years, though Q3 GDP likely stagnated, while consumer confidence continues a slow recovery with November GfK forecast at -22.0 (from -22.3), supported by better wage outlooks and inflation easing to 2.5%, despite ongoing household caution. | ||

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, the door is now open for a deeper setback below the 2024 low at 139.58, exposing a retest of the 2023 low. Rallies should be well capped below 155.00. | ||

| ||

| R2 154.80 - 12 February high - Strong R1 153.28 - 10 October high - Medium S1 149.38 - 17 October low - Medium S2 149.03 - 6 October low - Strong | ||

| USDJPY: fundamental overview | ||

| The USDJPY rally, driven by Japan’s new PM Sanae Takaichi’s expected fiscal expansion and monetary stimulus echoing Abenomics—plus the U.S.-Japan yield gap—remains fragile. Upside is limited by risks including potential fiscal discipline from coalition partner Ishin, a hawkish Bank of Japan signal at its October 29–30 meeting amid cost-of-living pressures, and Fed rate cuts eroding the dollar’s edge. Near-term, yen bears dominate as Trump endorses Takaichi’s defense spending hike to 2% of GDP by next March, and improved US-China ties post-APEC boost risk appetite, pressuring the safe-haven yen. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6629 - 1 October high - Strong R1 0.6573 - 10 October high - Medium S1 0.6471 - 16 October low - Medium S1 0.6440 - 14 October low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian Dollar rallied yesterday on news of a successful US-China framework for their upcoming summit in South Korea, sparking a risk-on market mood. The pair gained further support from RBA Governor Bullock’s cautious comments ahead of the November meeting, where she stressed balancing employment and sticky inflation (with unemployment at 4.5% and core inflation at 2.7%), noting Australia’s milder tightening cycle could mean shallower easing. Markets viewed her hawkish tone—emphasizing new forecasts and potential action on inflation deviations—as reducing the odds of a near-term rate cut from 64% to 38%. If the Fed delivers dovish guidance on Wednesday, AUDUSD could see a third boost, targeting a retest of the September 30 lower high around 0.6629. | ||

| Suggested reading | ||

| Wall Street, China Trample On Dollarization & Federal Reserve, J. Tamny, Forbes (October 26, 2025) The Red Flags That Signal the Faux Market Disruptors, S. McBride, RiskHedge (October 24, 2025) | ||