| ||

| 12th May 2025 | view in browser | ||

| US-China trade talk progress boosts sentiment | ||

| Asian markets have kicked the week off on a positive note, driven by progress in U.S.-China trade negotiations held in Switzerland. The White House signaled an upcoming trade agreement, with the U.S. Treasury Secretary and Chinese Vice Premier noting significant advancements, boosting regional market sentiment. | ||

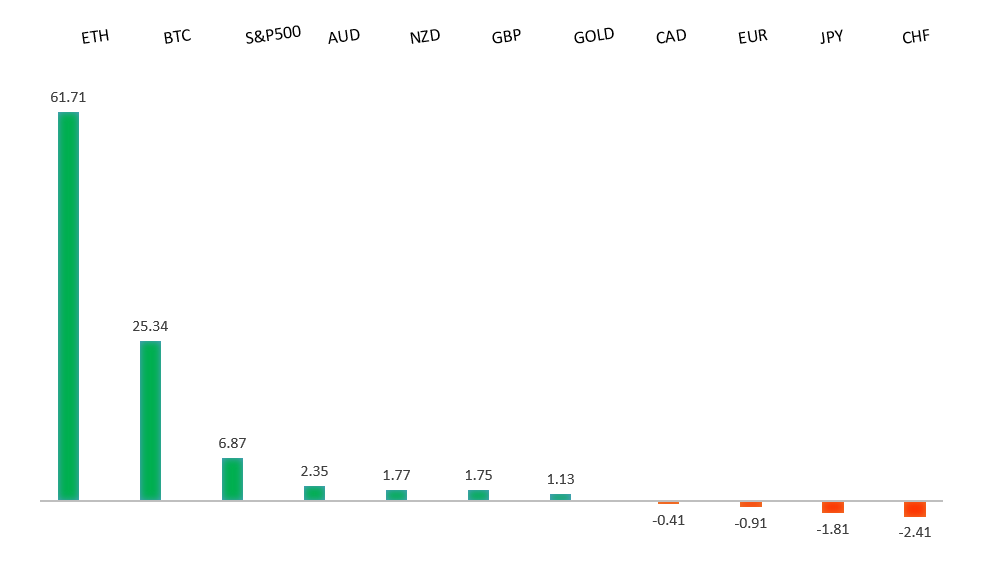

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro has finally broken out from a multi-month consolidation off a critical longer-term low. This latest push through the 2023 high lends further support to the case for a meaningful bottom, setting the stage for a bullish structural shift and the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported below 1.1000. | ||

| ||

| R1 1.1574 - 21 April/2025 high - Strong R1 1.1382 - 2 May high - Medium S1 1.1181 - 11 April low - Medium S2 1.1148 - 3 April high - Strong | ||

| EURUSD: fundamental overview | ||

| Ukraine, supported by European nations and U.S. President Trump, has called for a 30-day unconditional ceasefire to facilitate peace negotiations, with new sanctions threatened against Russia if rejected. Russian President Putin proposed direct talks with Ukraine in Istanbul on May 15, and Ukraine’s President Zelenskiy, backed by Trump, will attend to pursue a potential ceasefire agreement. A de-escalation in the Russia-Ukraine conflict and U.S.-China trade tensions could boost Eurozone prospects, strengthening EURUSD. ECB officials, including Simkus and Rehn, anticipate weaker economic growth and support further rate cuts if disinflation persists, though hawkish members like Schnabel caution about inflation risks from rising protectionism and defense spending. Germany and Eurozone’s May ZEW Survey Expectations are expected to show cautious improvement after April’s sharp decline, driven by trade uncertainties, with Germany’s Current Situation Index reflecting slight gains from fiscal stimulus. | ||

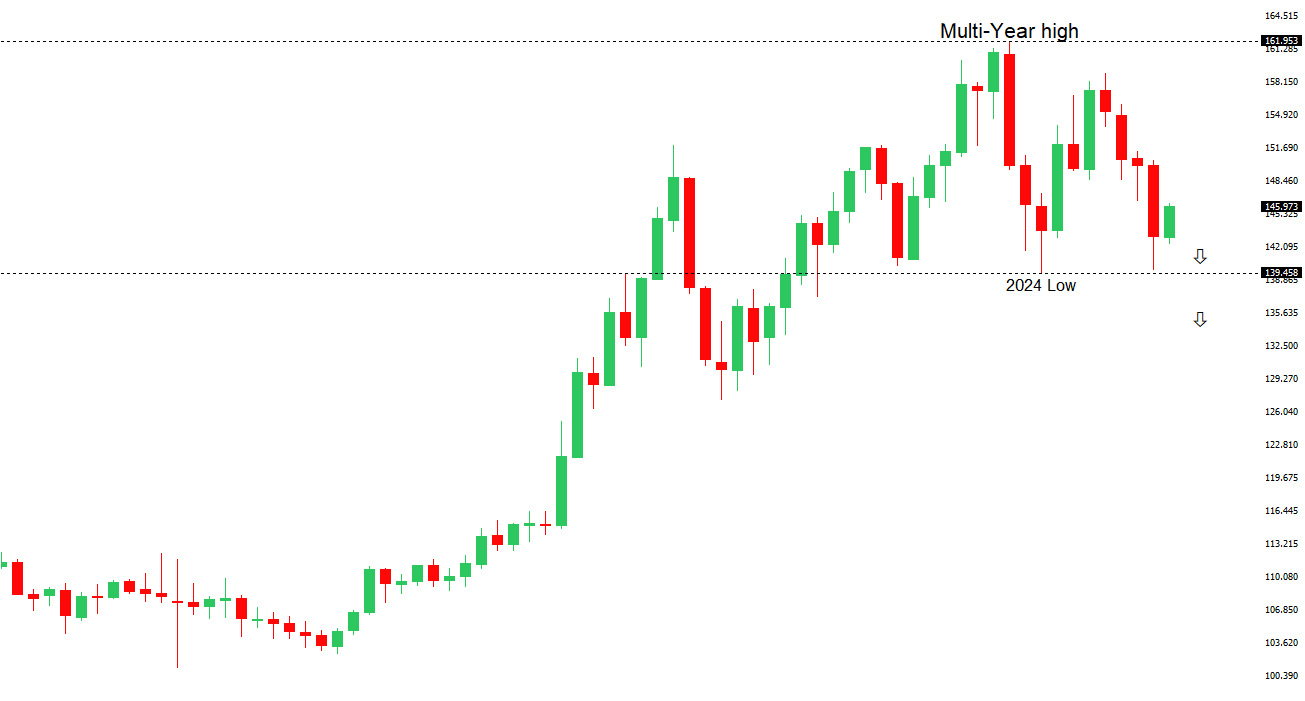

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, the door is now open for a deeper setback below the 2024 low at 139.58 over the coming sessions exposing a retest of the 2023 low. Rallies should be well capped below 150.00. | ||

| ||

| R2 148.28 - 9 April high - Strong R1 146.29 - 12 May high - Medium S1 142.35 - 6 May low - Medium S1 141.97 - 29 April low - Medium | ||

| USDJPY: fundamental overview | ||

| The Yen may remain sensitive to U.S.-China trade developments, with potential de-escalation reducing yen haven demand. Japan’s March nominal wages grew 2.1% year-on-year, below expectations, while real wages fell 2.1%, and April exports slowed to 2.3% growth, signaling caution for BOJ rate hikes amid trade uncertainties. Despite weak data, BOJ Governor Ueda emphasizes raising rates if economic conditions align, with inflation pressures persistent, but trade talks with the U.S. face challenges as Japan seeks tariff relief. U.S.-Japan negotiations have stalled, with the U.S. rejecting full tariff exemptions and focusing only on reducing Japan’s 14% specific tariff, while further talks are planned for May and a potential leaders’ meeting at the G7 summit in June. Japan’s PM Ishiba aims for a trade deal by July, coinciding with the end of a 90-day tariff pause and Japan’s elections. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6550 - 25 November high - Strong R1 0.6515 - 7 May/2025 high - Medium S1 0.6344 - 24 April low - Medium S1 0.6275 - 14 April low - Strong | ||

| AUDUSD: fundamental overview | ||

| Iron ore prices are sliding toward the $80s per ton as China’s steel association confirms mill production cuts, pressuring the Australian dollar due to iron ore’s role as Australia’s key export. Markets are optimistic about U.S.-China trade de-escalation and a potential Russia-Ukraine ceasefire, boosting global equity futures and supporting antipodean currencies. With inflation within the RBA’s target range, a rate cut is anticipated at the May 20 meeting, though Governor Bullock stresses data-driven decisions amid tariff-related growth and inflation risks. Australia’s economic ties to China suggest a slowdown may overshadow inflation concerns, with Chinese exports potentially redirecting to Australia, while OIS markets project 93 basis points of rate cuts in 2025. | ||

| Suggested reading | ||

| Warren Buffett Versus American Capitalism, J. Authers, Bloomberg (May 9, 2025) The Most Profitable Dividend Strategy Is the Simplest, S. Jakab, WSJ (May 9, 2025) | ||