Next 24 hours: Major currencies cool off

Today’s report: Market responds aggressively to US inflation data

It comes as no surprise to see the market reaction to Tuesday’s round of softer than expected US inflation data. As we’ve highlighted many times throughout the year, investors are looking for any and every excuse to pressure the Federal Reserve into reconsidering its higher for longer policy stance in favor of a more investor friendly, accommodative adjustment.

Wake-up call

- Eurozone trade

- UK inflation

- Yield differential

- China data

- Local developments

- sentiment improves

- about inflation

- Global outlook

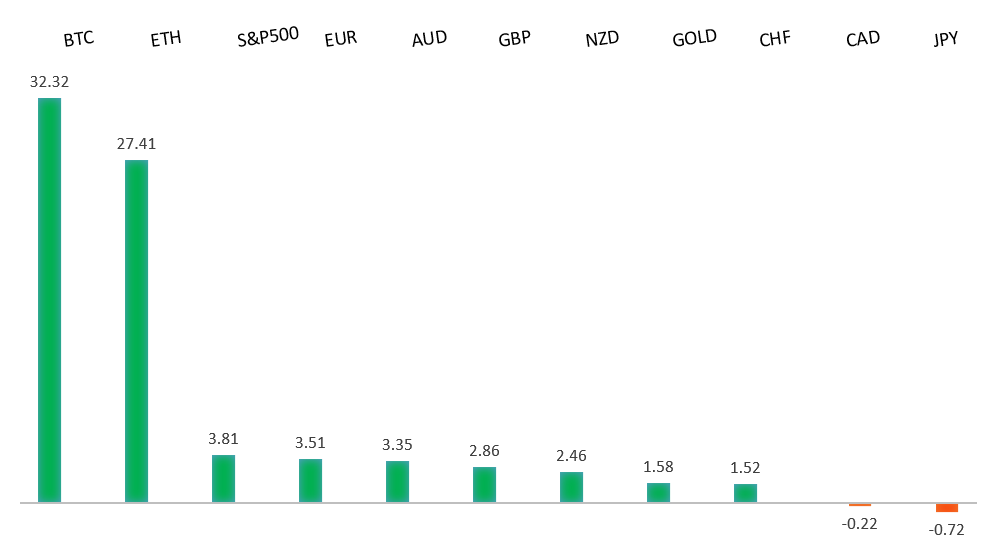

Peformance chart: 30 Day Performance vs. US dollar (%)

Suggested reading

- How Can Economists Say They're 'Capitalists'?, J. Calhoun, Alhambra (November 9, 2023)

- The Top Shortlisted Companies 2023, N. Hawcock, Financial Times (November 15, 2023)

Chart talk: Technical & fundamental highlights

Choose pair:

EURUSD – technical overview

The Euro has been in a multi-month consolidation since bottoming out in 2022. Setbacks have since been exceptionally well supported on dips below 1.0500, with a higher platform sought out ahead of the next major upside extension. Look for a push through the yearly high at 1.1276 to strengthen the constructive outlook and extend the recovery run towards 1.2000. Only back below 1.0400 negates.EURUSD – fundamental overview

The Euro got an initial boost from solid ZEW reads before accelerating to the topside on the back of the softer US inflation data. Key standouts on Wednesday’s calendar come from German wholesale prices, UK inflation, Eurozone trade, Eurozone industrial production, Canada manufacturing sales, US retail sales, US producer prices, and US business inventories.EURUSD - Technical charts in detail

GBPUSD – technical overview

Signs have emerged of the market wanting to put in a longer-term base after collapsing to a record low in September 2022. The November 2022 monthly close back above 1.2000 strengthens this prospect. Any setbacks should now be well supported ahead of 1.2000. Next key resistance comes in at 1.2681.GBPUSD – fundamental overview

The Pound was already feeling better about decent UK jobs and wages numbers, before then enjoying another big push on the back of the softer than expected US inflation data. Key standouts on Wednesday’s calendar come from German wholesale prices, UK inflation, Eurozone trade, Eurozone industrial production, Canada manufacturing sales, US retail sales, US producer prices, and US business inventories.USDJPY – technical overview

The market remains confined to a strong uptrend, with sights set on a retest and break of the multi-year high from 2022 at 151.95. A push through this level will open the next major upside extension towards 155.00. Key support comes in at 147.30, with only a break below to delay the constructive outlook.USDJPY – fundamental overview

Finally, some relief for the Yen, with the currency recovering on the back of yield differentials moving out of the US Dollar's favor following a softer round of US inflation data. On the Japan data front, the economy contracted by more than expected, though this event was mostly shrugged off with respect to market reaction and Yen moves. Key standouts on Wednesday’s calendar come from German wholesale prices, UK inflation, Eurozone trade, Eurozone industrial production, Canada manufacturing sales, US retail sales, US producer prices, and US business inventories.AUDUSD – technical overview

There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.6200 would give reason for rethink. Back above 0.6523 will take the immediate pressure off the downside and strengthen case for a bottom.AUDUSD – fundamental overview

The Australian wage price index came in a little higher than forecast, while China data was decidedly above forecast as reflected through industrial production and retail sales reads. This in conjunction with the softer US inflation data and renewed risk on flow have contributed to the latest surge in the Australian Dollar. Key standouts on Wednesday’s calendar come from German wholesale prices, UK inflation, Eurozone trade, Eurozone industrial production, Canada manufacturing sales, US retail sales, US producer prices, and US business inventories.USDCAD – technical overview

Above 1.3000 signals an end to a period of longer-term bearish consolidation and suggests the market is in the process of carving out a more significant longer-term base. Next key resistance now comes in up into the 1.4000 area. Setbacks should be very well supported down into the 1.3000 area.USDCAD – fundamental overview

Like all currencies, the Canadian Dollar put in a rally on Tuesday on the back of the softer than expected US inflation data. At the same time, the outlook in Canada is less upbeat of late, with the household debt burden and restrained spending dominating local news flow. Key standouts on Wednesday’s calendar come from German wholesale prices, UK inflation, Eurozone trade, Eurozone industrial production, Canada manufacturing sales, US retail sales, US producer prices, and US business inventories.NZDUSD – technical overview

Overall pressure remains on the downside with the market once again stalling out on a run up into the 0.6500 area. At the same time, there are some signs of the market wanting to put in a longer-term base. Ultimately, a break back above 0.6056 would be required to take the immediate pressure off the downside and encourage this prospect. A monthly close below 0.5800 will intensify bearish price action.NZDUSD – fundamental overview

The New Zealand Dollar has benefitted greatly from the latest round of soft US inflation data and concurrent wave of broad based US Dollar selling and risk on flow. Key standouts on Wednesday’s calendar come from German wholesale prices, UK inflation, Eurozone trade, Eurozone industrial production, Canada manufacturing sales, US retail sales, US producer prices, and US business inventories.US SPX 500 – technical overview

Longer-term technical studies are in the process of unwinding from extended readings off record highs. Look for rallies to be well capped in favor of lower tops and lower lows. A monthly close back above 4500 will be required to take the immediate pressure off the downside. Next key support comes in at 4308.US SPX 500 – fundamental overview

Investors continue to struggle with the reality of a higher for longer Fed policy track in the face of ongoing worry around inflation, while also contending with geopolitical risk. Overall, we expect inflation to continue to be a problem in 2023 that results in downside pressure into rallies despite recent data and market expectations that would argue otherwise.GOLD (SPOT) – technical overview

The 2019 breakout above the 2016 high at 1375 was a significant development, opening the door for fresh record highs. Setbacks should now be well supported above 1600 on a monthly close basis ahead of the next major upside extension. Next major resistance comes in at 2100, above which opens the next extension towards 2500.GOLD (SPOT) – fundamental overview

The yellow metal continues to be well supported on dips with solid demand from medium and longer-term accounts. These players are more concerned about inflation risk and a less stable and upbeat global growth outlook. All of this should keep the commodity well supported, with many market participants also fleeing to the hard asset as the grand dichotomy of record high equities and record low yields comes to an unnerving climax.