Next 24 hours: Positive vibes carry over into Monday

Today’s report: Take it with a grain of salt

Friday’s market moves were somewhat perplexing. We saw a massive wave of risk on flow and broad based US Dollar selling. There was nothing in the US jobs report to have accounted for such intense moves, and if anything, the numbers continued to support the case for the Fed to keep with its hawkish, less investor friendly approach.

Wake-up call

- China news

- Dealers report

- Offshore Yuan

- Hawkish RBA

- 10x better

- Global sentiment

- Inflation headache

- Dealers report

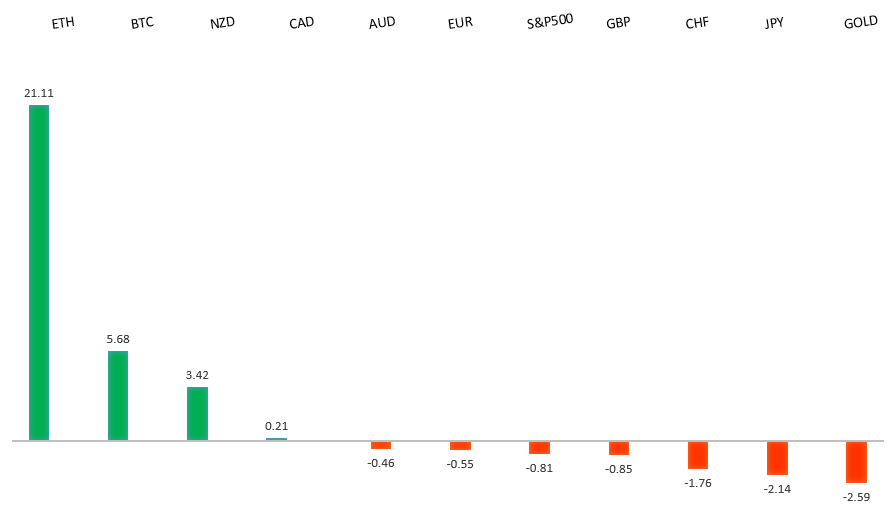

Peformance chart: 30 Day Performance vs. US dollar (%)

Suggested reading

- 12 Money Lessons From Warren Buffett & Charlie Munger, H. Kelly, Morningstar (November 3, 2022)

- Some Investors See Opportunities of a Lifetime, J. Segal, Institutional Investor (November 4, 2022)

Chart talk: Technical & fundamental highlights

Choose pair:

EURUSD – technical overview

Technical studies are turning up from oversold territory, suggesting additional setbacks should be limited in favour of some form of a meaningful correction and consolidation. A weekly close back above 1.0100 will take the immediate pressure off the downside.EURUSD – fundamental overview

A lot of the latest recovery in the Euro was driven off macro factors, with the news of the China reopening fueling broad based currency demand and selling of the US Dollar. ECB officials were out talking hawkish, and Euro area PMIs were revised higher, which also helped to add additional bid to the single currency. Key standouts on Monday’s calendar come from German industrial production, German and Eurozone construction PMIs, US consumer credit, and Fed speak.EURUSD - Technical charts in detail

GBPUSD – technical overview

Signs have emerged of the market wanting to put in a longer-term base after collapsing to a record low in September. A break above the September high at 1.1739 will solidify the recovery. Until then, look for setbacks to be well supported ahead of 1.0800.GBPUSD – fundamental overview

The Pound got a big boost on Friday from the China reopening news, which inspired broad based demand for currencies and selling of the US Dollar. At the same time, there are plenty of offers reported into rallies given the exceptionally tough spot the BOE finds themselves in. The central bank is caught between a rock and a hard place as it tries to navigate between slower growth and rocketing inflation. Key standouts on Monday’s calendar come from German industrial production, German and Eurozone construction PMIs, US consumer credit, and Fed speak.USDJPY – technical overview

Technical studies are looking quite stretched on the longer-term chart, warning of consolidation and correction in the days and weeks ahead. Look for additional upside from here to be well capped on rallies above 150.00. Next key support comes in at 145.43.USDJPY – fundamental overview

News of the China reopening inspired the largest daily advance on record in the offshore Yuan, which in turn opened plenty of demand for the correlated Yen. Monetary policy divergence between the Fed and BOJ should continue to weigh on the Yen, though with technicals extended and currencies broadly coming back bid, we could see additional Yen demand over the coming sessions. Key standouts on Monday’s calendar come from German industrial production, German and Eurozone construction PMIs, US consumer credit, and Fed speak.AUDUSD – technical overview

Overall pressure remains on the downside with the market confined to a well defined downtrend. A break back above 0.6682 would be required to take the pressure off the downside. Until then, scope exists for deeper setbacks towards 0.6000.AUDUSD – fundamental overview

The Australian Dollar performed well into the previous weekly close, getting a boost from a hawkish RBA statement on monetary policy, and then getting another boost from the news of the China reopening. Key standouts on Monday’s calendar come from German industrial production, German and Eurozone construction PMIs, US consumer credit, and Fed speak.USDCAD – technical overview

A recent surge back above 1.3000 signals an end to a period of bearish consolidation and suggests the market is in the process of carving out a more significant longer-term base. Next key resistance now comes in up into the 1.4000 area. Setbacks should be very well supported down into the 1.3000 area.USDCAD – fundamental overview

It was no surprise to see the Canadian Dollar rallying sharply on Friday, this on the back of a blowout Canada employment report which came out 10 times better than expected. Meanwhile, broad based currency gains and US Dollar selling also added to the Loonie bid after reports came out talking about a China reopening. Key standouts on Monday’s calendar come from German industrial production, German and Eurozone construction PMIs, US consumer credit, and Fed speak.NZDUSD – technical overview

Overall pressure remains on the downside with the focus on a retest of the critical low from 2020 at 0.5469. A break back above 0.6162 would be required to take the immediate pressure off the downside.NZDUSD – fundamental overview

New Zealand economic data has been stronger of late, while inflation continues to climb, all of which has resulted in Kiwi outperformance against its peers. At the same time, the news of the China reopening has been taken as a big positive for the global economy, also helping to prop the risk correlated commodity currency. Key standouts on Monday’s calendar come from German industrial production, German and Eurozone construction PMIs, US consumer credit, and Fed speak.US SPX 500 – technical overview

Longer-term technical studies are in the process of unwinding from extended readings off record highs. Look for rallies to be well capped in favor of lower tops and lower lows. Back above 4000 will be required at a minimum to take the immediate pressure off the downside. Next major support comes in around 3200.US SPX 500 – fundamental overview

We've finally reached a point in the cycle where the Fed recognizes unanchored inflation expectations pose a greater downside risk than over-tightening. This is significant, as it means less investor friendly monetary policy that risks potential recession in the months ahead. Overall, we expect inflation to continue to be a problem in Q4 2022 and Q1 2023 that results in downside pressure into rallies.GOLD (SPOT) – technical overview

The 2019 breakout above the 2016 high at 1375 was a significant development, opening the door for fresh record highs. Setbacks should now be well supported above 1600 on a monthly close basis ahead of the next major upside extension.GOLD (SPOT) – fundamental overview

The yellow metal continues to be well supported on dips with solid demand from medium and longer-term accounts. These players are more concerned about inflation risk and a less upbeat global growth outlook. All of this should keep the commodity well supported, with many market participants also fleeing to the hard asset as the grand dichotomy of record high equities and record low yields comes to an unnerving climax.