| ||

| 10th April 2026 | view in browser | ||

| Geopolitics flip to tailwind | ||

| Geopolitics remains firmly in the driver’s seat. The fragile US-Iran two-week ceasefire continues to hold with the Strait of Hormuz reopened, triggering another leg lower in oil prices and cementing the relief rally in risk assets. | ||

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1724 - 9 April high - Strong R1 1.1700 - Figure - Medium S1 1.1590 - 8 April low - Medium S2 1.1504 - 3 April low - Strong | ||

| EURUSD: fundamental overview | ||

| The euro has been supported by the ongoing fragile US-Iran ceasefire and the associated reopening of the Strait of Hormuz, which has eased immediate oil supply disruption fears and driven a sharp pullback in crude prices. This has reduced stagflation risks for the eurozone by limiting imported inflation pressures while preserving some growth resilience, leading to a relief move in risk assets and a dialing back of expectations for aggressive near-term ECB rate hikes. With no meaningful economic data releases or central bank commentary emerging to alter the narrative, the single currency has also benefited from softer safe-haven flows into the dollar and modestly improved European sentiment, though lingering doubts over the ceasefire’s durability continue to limit upside conviction. | ||

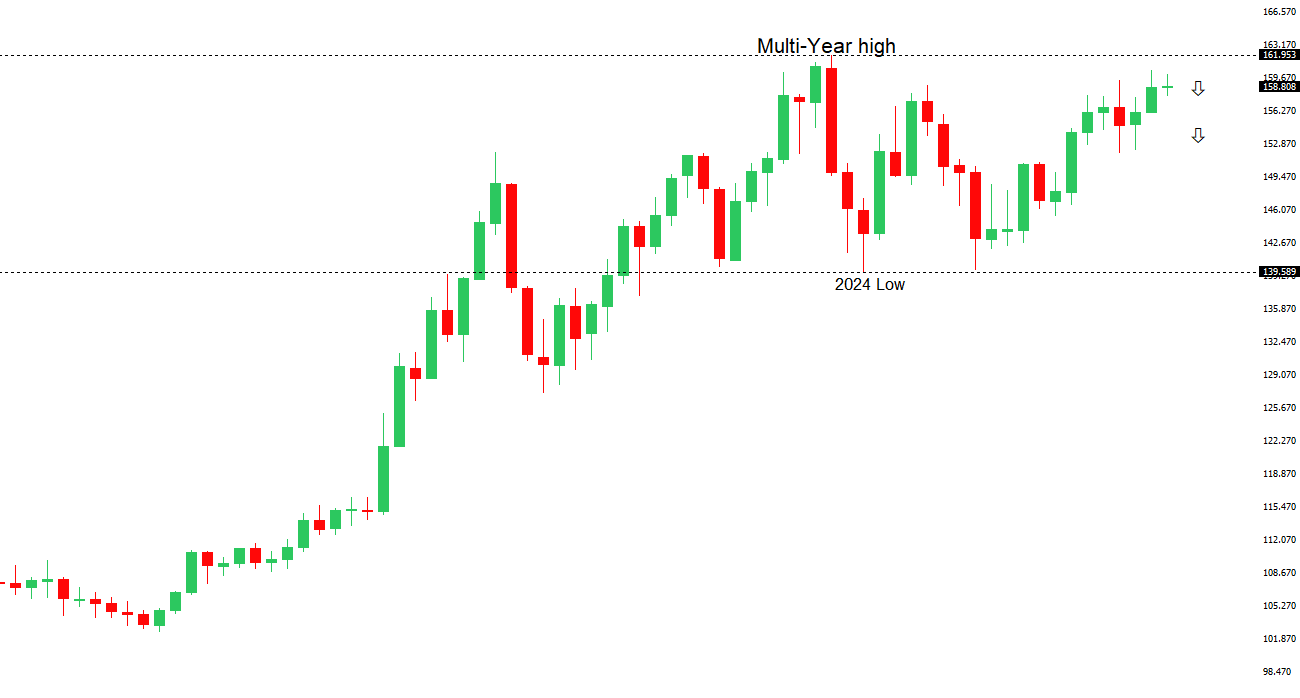

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped above 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 160.00 negates. | ||

| ||

| R2 160.46 - 30 March/2026 high - Strong R1 160.03 - 7 April high - Medium S1 157.89 - 8 April low - Medium S2 157.51 - 19 March low - Strong | ||

| USDJPY: fundamental overview | ||

| The Japanese yen has strengthened modestly amid the fragile US-Iran ceasefire and reopening of the Strait of Hormuz, which has triggered a sharp decline in oil prices and eased immediate energy supply disruption fears for Japan as a major net importer. Lower crude costs have reduced imported inflation pressures and supported risk sentiment, diminishing safe-haven demand for the dollar while highlighting the yen’s sensitivity to oil and geopolitical developments. With no major economic data releases and limited fresh central bank commentary, growing market expectations for a potential Bank of Japan rate hike as early as April—to address persistent inflation—have provided additional underlying support, though lingering doubts over the ceasefire’s durability continue to cap the yen’s gains. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7188 - 11 March/2026 high - Strong R1 0.7095 - 9 April high - Medium S1 0.6963 - 8 April low - Medium S2 0.6833 - 30 March low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar has been supported by the fragile US-Iran ceasefire and reopening of the Strait of Hormuz, which has triggered a sharp decline in oil prices and eased immediate energy supply disruption fears. As a major commodity exporter, Australia has benefited from improved global risk sentiment and reduced stagflation risks, weighing on safe-haven flows into the dollar and supporting carry trade appetite. However, lower crude costs have also tempered imported inflation pressures, leading markets to scale back expectations for aggressive near-term RBA rate hikes amid a more balanced growth and inflation outlook, which has helped cap the extent of the Aussie’s upside. | ||

| Suggested reading | ||

| The Decline and Fall of the Dollar Empire, B. Eichengreen, Project Syndicate (April 9, 2026) An Impossible Choice For The Fed?, H. McDonald, Carson Group (April 8, 2026) | ||