| ||

| 26th May 2026 | view in browser | ||

| Diplomacy keeps the macro panic contained | ||

| Markets are cautiously stabilizing as investors increasingly price a managed diplomatic resolution to the Iran-Hormuz conflict, driving a pullback in oil and haven assets while leaving FX and equities trading in a more measured risk-sensitive environment. | ||

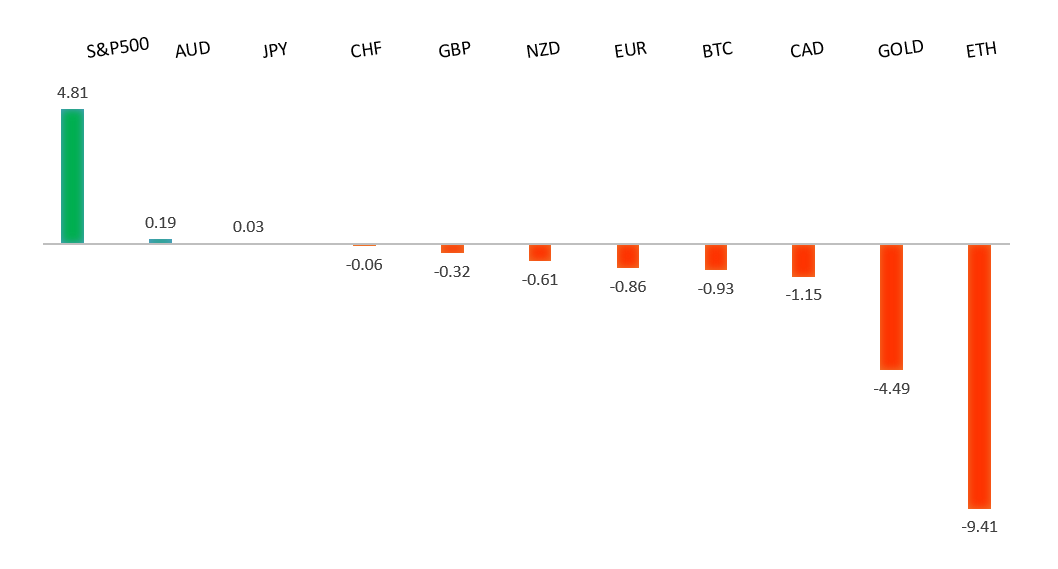

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1797 - 6 May high - Medium R1 1.1722 - 14 May high - Medium S1 1.1576 - 21 May low - Medium S2 1.1504 - 3 April low - Strong | ||

| EURUSD: fundamental overview | ||

| The euro has come under modest pressure in recent trade as renewed uncertainty around the fragile US-Iran ceasefire has driven a broader safe-haven bid into the US dollar. Reports that US forces carried out defensive strikes in southern Iran after ceasefire violations have kept markets cautious, while concerns over the Strait of Hormuz and broader Middle East energy security continue to cloud sentiment. At the same time, the euro has found some underlying support from a more hawkish shift at the ECB, as policymakers increasingly acknowledge that the latest energy shock risks prolonging inflation pressures across the Eurozone. ECB officials including Isabel Schnabel have argued that “looking through” another inflation spike is no longer an option, warning that rising energy costs are beginning to spill over into the wider consumption basket even as growth risks deteriorate. Markets have consequently moved to price a high probability of another ECB rate hike, helping to offset some of the euro’s geopolitical-driven weakness. | ||

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped above 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 160.00 negates. | ||

| ||

| R2 159.53 - 17 April low - Medium R1 159.36 - 21 May high - Medium S1 157.29 - 14 May low - Medium S2 155.02 - 6 May low - Strong | ||

| USDJPY: fundamental overview | ||

| The yen has remained under pressure against the dollar as a combination of external and domestic fundamentals continues to favor the greenback. Heightened geopolitical uncertainty surrounding the Middle East has undercut the traditional safe-haven appeal of the yen, with markets increasingly focused on the negative implications of elevated energy prices and supply disruptions for Japan’s import-dependent economy. At the same time, the dollar has found renewed support from resilient US economic data and persistent inflation, reinforcing expectations that the Fed will keep rates higher for longer. On the domestic side, while BOJ Deputy Governor Himino reiterated that the Bank of Japan still intends to continue raising rates and gradually normalize policy, he stressed that the timing and pace of tightening would depend heavily on how Middle East developments affect Japan’s economy and inflation outlook. That conditional approach has tempered expectations for aggressive BOJ tightening, especially as policymakers remain cautious about financial conditions and bond market stability. Markets also remain alert to the risk of official FX intervention should yen weakness accelerate further beyond current levels. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7278 - 6 May/2026 high - Strong R1 0.7222 - 17 April high - Medium S1 0.7079 - 19 May low - Medium S2 0.6963 - 8 April low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian Dollar has come under renewed pressure amid a broader deterioration in global risk sentiment following fresh US military strikes on southern Iran. The escalation in geopolitical tensions has supported safe-haven demand for the US Dollar and weighed on risk-sensitive currencies like the Aussie, particularly given Australia’s close exposure to global growth and commodity demand dynamics. At the same time, markets remain cautious ahead of Australia’s April CPI report, where headline inflation is expected to ease modestly from 4.6% YoY to 4.4%, though any upside surprise could revive expectations that the RBA will need to maintain a relatively hawkish policy stance for longer. More broadly, the AUD has also been influenced by shifting China sentiment and commodity price dynamics, with investors continuing to monitor the outlook for Chinese demand, iron ore prices, and the trajectory of US yields, all of which remain key external drivers for the Australian currency. | ||

| Suggested reading | ||

| What’s Not to Like About Rising Bond Yields?, S. Kirchner, Institutional Economics (May 23, 2026) Making a Case for Bond Yields Entering the Danger Zone, R. Forsyth, Barron’s (May 22, 2026) | ||