| ||

| 25th June 2026 | view in browser | ||

| Dollar catches its breath as macro crosscurrents build | ||

| The US dollar is taking a breather after its recent rally as markets balance hawkish global central bank signals, easing oil prices, resilient AI-driven equity optimism and ongoing geopolitical uncertainty heading into another eventful session. | ||

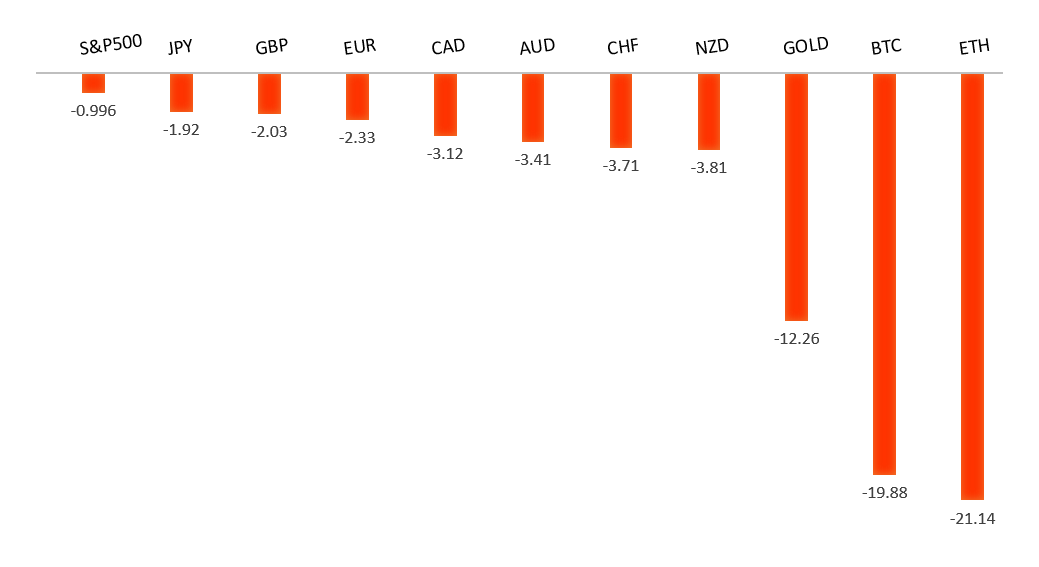

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

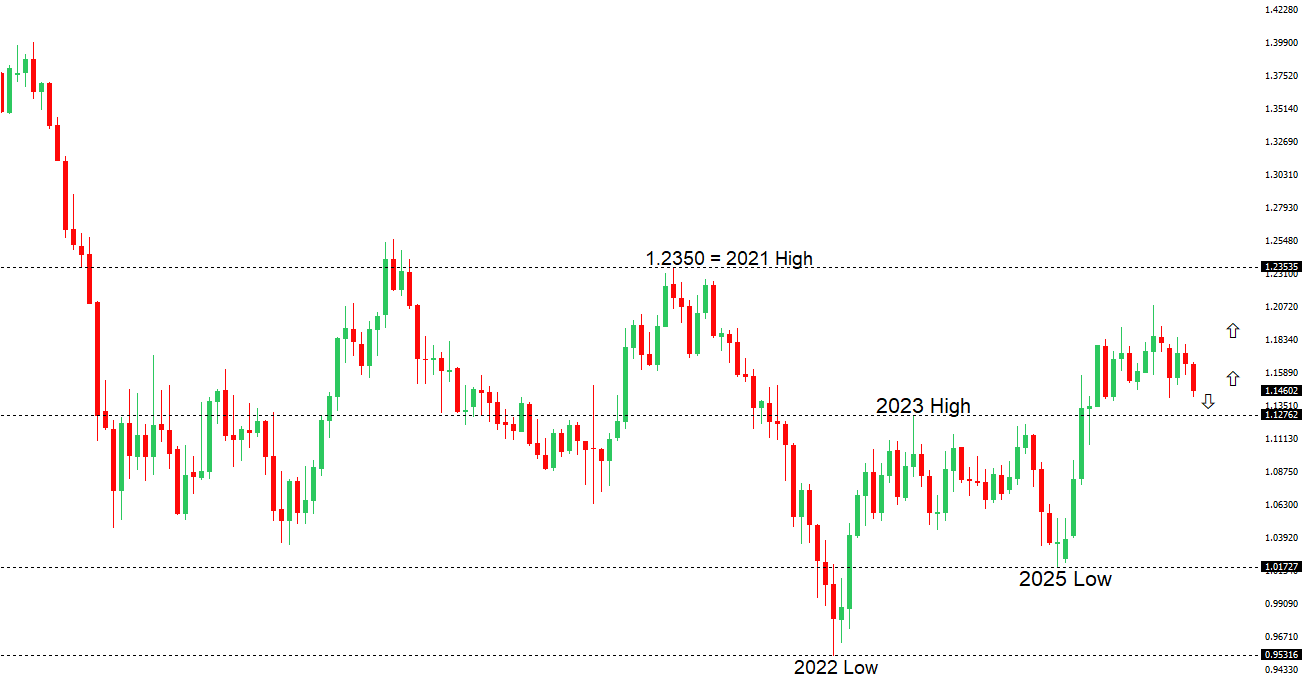

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1529 - 18 June high - Medium R1 1.1440 - 23 June high - Medium S1 1.1325 - 24 June/2026 low - Medium S2 1.1300 - Figure - Medium | ||

| EURUSD: fundamental overview | ||

| The euro remains under pressure against the US dollar, with EURUSD hovering around one-year lows as markets continue to favor the greenback on expectations that the Federal Reserve could keep policy tighter for longer, particularly if today’s US PCE inflation data reinforces the recent run of firm inflation and resilient economic activity. While the ECB has shifted to a more hawkish tone in recent weeks and remains alert to upside inflation risks, that has been outweighed by widening US yield support and stronger demand for the dollar. For now, the euro is finding some support around the 1.1350 area as investors await the PCE report, with a hotter-than-expected reading likely to strengthen Fed tightening expectations and add further downside pressure on EURUSD. | ||

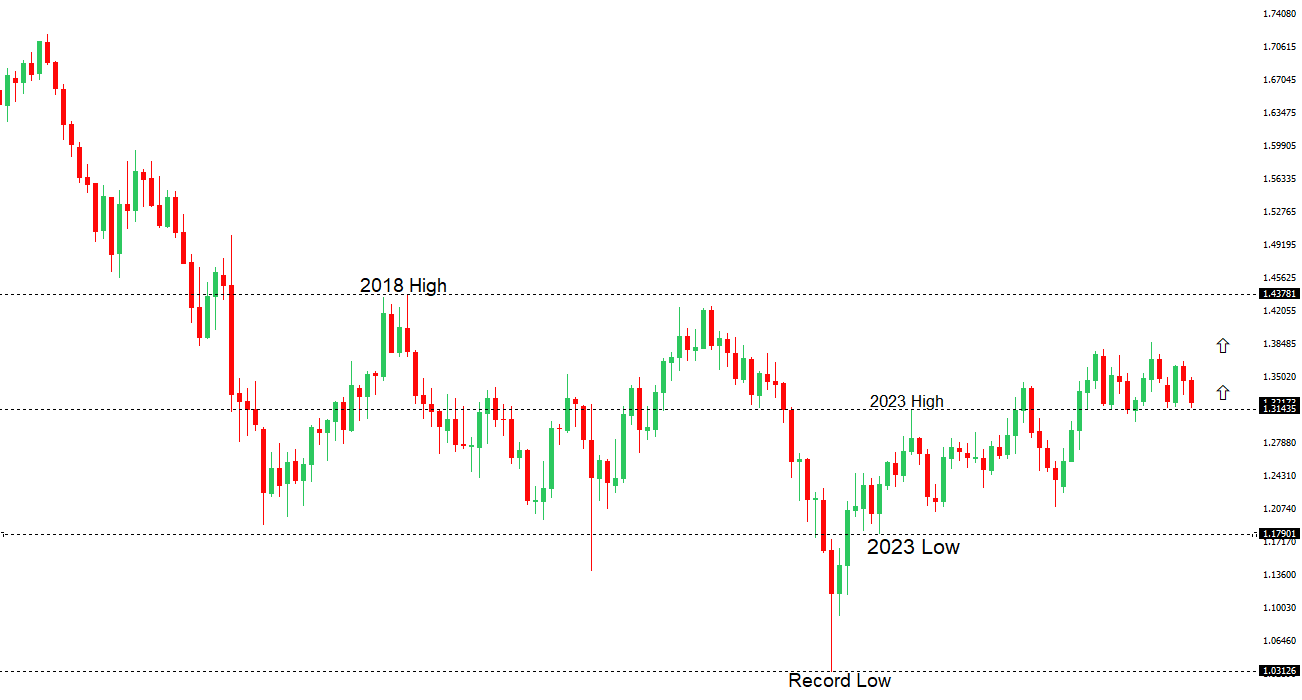

| GBPUSD: technical overview | ||

| The Pound remains exceptionally well supported on dips into the 1.3000 area, with the price largely consolidating above the psychological barrier and previous resistance turned support in the form of the 2023 high. Look for the market to continue be well supported on dips ahead of the next major upside extension through the yearly high at 1.3870 and towards a retest of the 2018 high at 1.4377 further up. Only a monthly close below 1.3000 negates. | ||

| ||

| R2 1.3325 - 18 June high - Medium R1 1.3274 - 22 June high - Medium S1 1.3140 - 24 June/2026 low - Medium S2 1.3100 - Figure - Medium | ||

| GBPUSD: fundamental overview | ||

| Sterling remains under pressure against the US Dollar as UK political uncertainty continues to weigh on sentiment following Prime Minister Keir Starmer’s resignation, with investors now focused on the leadership transition and the potential for a more expansionary fiscal agenda under a new government. At the same time, the widening policy divergence between the Bank of England and an increasingly hawkish Federal Reserve continues to favor the Dollar, as markets have sharply increased expectations for further US rate hikes after recent Fed messaging. While the pound has managed to stabilize above the mid-1.31s after its recent sell-off, upside remains limited ahead of the latest US PCE inflation data, which could further reinforce the higher-for-longer US rates narrative if inflation surprises to the upside. Broader risk sentiment has also remained cautious, leaving sterling vulnerable as political uncertainty at home combines with a stronger US Dollar backdrop. | ||

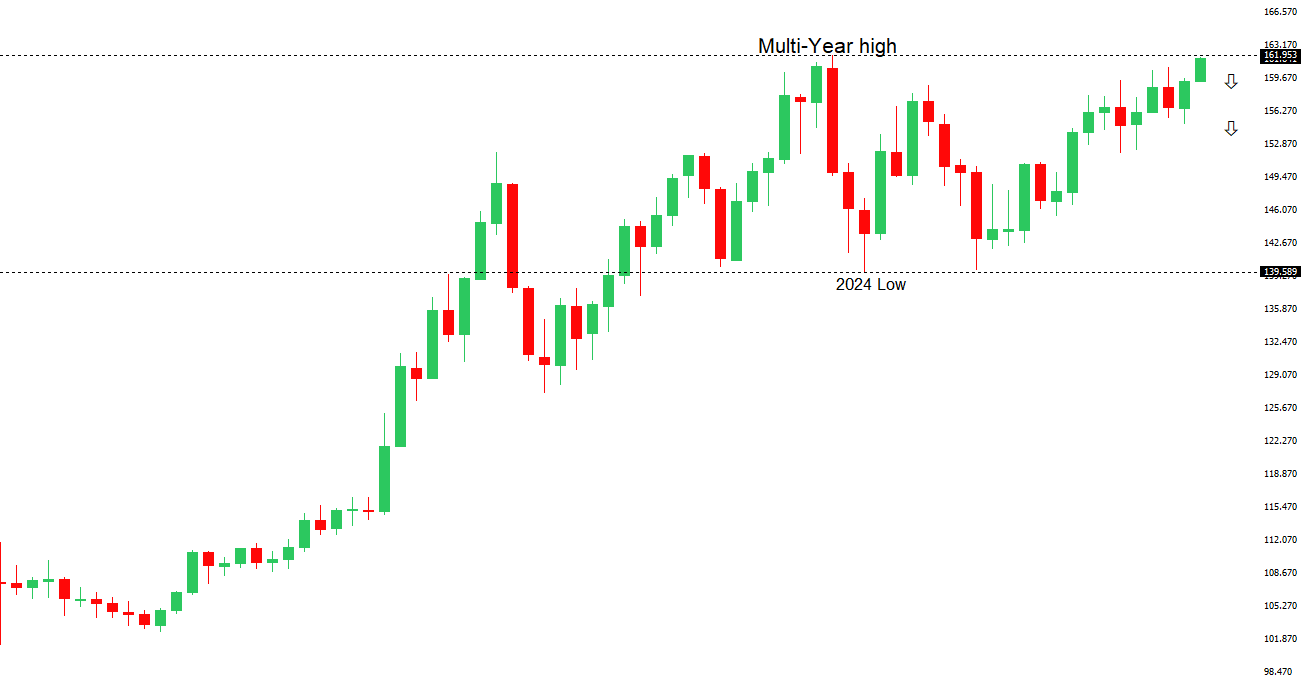

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped below 162.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 162.00 negates. | ||

| ||

| R2 161.96 - Multi-Year high/2024 - Very Strong R1 161.93 - 22 June/2026 high - Strong S1 160.41 - 18 June low - Medium S2 159.54 - 11 June low - Strong | ||

| USDJPY: fundamental overview | ||

| The Yen remains under pressure, with USDJPY trading just below the 162.00 level and close to four-decade highs as the wide US-Japan interest rate differential continues to favor the US Dollar and keep carry trades attractive. While recent comments from Bank of Japan officials have reinforced expectations for further policy tightening, including board member Naoki Tamura’s view that rates should gradually move toward a neutral level around 2%, markets still see Japanese rates remaining well below US levels for the foreseeable future. At the same time, the BoJ’s June Summary of Opinions highlighted growing concern over inflation risks and a willingness among some policymakers to raise rates more quickly if needed. The Yen has found only modest support from renewed intervention warnings, with Japanese officials reiterating they stand ready to act against excessive currency moves and reports of close coordination between Tokyo and Washington helping to temper, but not reverse, Yen weakness. Attention now turns to the US PCE inflation report, which could reshape expectations for the Federal Reserve’s policy path and drive the next major move in USDJPY, while easing oil prices have provided only limited relief by slightly reducing concerns over imported inflation in Japan. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7089 - 15 June high - Strong R1 0.6979 - 11 June low - Medium S1 0.6882 - 24 June low - Medium S2 0.6833 - 30 March low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar remains under modest pressure as broad US Dollar strength, driven by expectations that the Federal Reserve’s next policy move is more likely to be a rate hike than a cut, continues to dominate sentiment. Markets have priced in elevated odds of additional Fed tightening, while investors are awaiting the latest US PCE inflation data for fresh direction on the US rates outlook. Domestically, however, the Australian backdrop remains relatively resilient after stronger-than-expected May employment data showed the economy added 40.3K jobs and the unemployment rate edged down to 4.4%, reinforcing the view that labor market conditions remain tight. That should help keep the Reserve Bank of Australia cautious on easing and provide some underlying support for the Aussie, although for now the currency continues to be driven more by the stronger US Dollar and broader global risk sentiment than by domestic fundamentals. | ||

| Suggested reading | ||

| The Yen Needs A Lot More Than Market Intervention, D. Lachman, AEIdeas (June 23, 2026) Magnificent 7 Correction May Signal a Healthy Stock Market, C. Ji, Marketwatch (June 23, 2026) | ||