| ||

| 10th June 2026 | view in browser | ||

| Caught between Hormuz and the Fed | ||

| Markets come into Wednesday balancing an escalating US-Iran conflict and its inflationary implications against still-resilient global growth, with all eyes now on US CPI as investors assess whether rising energy costs will reinforce the case for higher-for-longer interest rates. | ||

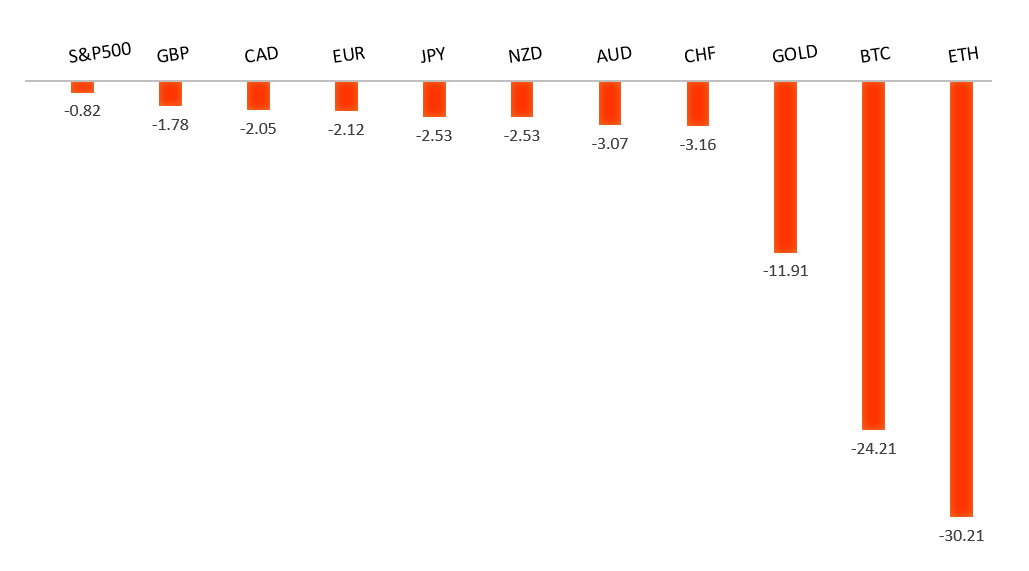

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1646 - 4 June high - Medium R1 1.1576 - 21 May low - Medium S1 1.1500 - 8 June low - Medium S2 1.1443 - 30 March low - Medium | ||

| EURUSD: fundamental overview | ||

| The Euro has traded in a relatively tight range, with EURUSD consolidating around the 1.1550 area as investors await the latest US CPI report for fresh direction. While the single currency continues to draw support from expectations that the European Central Bank will deliver a 25 basis point rate hike at Thursday’s meeting amid persistent inflation concerns, gains have been tempered by a cautious market mood ahead of key event risk from both the ECB and the Federal Reserve outlook. Recent easing in Middle East tensions has helped stabilize risk sentiment and reduce demand for traditional safe havens, although lingering geopolitical uncertainty continues to underpin the US Dollar at times. As a result, the near-term path for the Euro is being driven largely by the balance between a still relatively hawkish ECB, shifting US rate expectations following stronger US economic data, and the outcome of upcoming inflation figures that could reshape the outlook for Fed policy. Markets are widely expecting the ECB to raise rates this week, with attention likely to shift toward President Lagarde’s guidance on whether further tightening remains on the table later this year. | ||

| GBPUSD: technical overview | ||

| The Pound remains exceptionally well supported on dips into the 1.3000 area, with the price largely consolidating above the psychological barrier and previous resistance turned support in the form of the 2023 high. Look for the market to continue be well supported on dips ahead of the next major upside extension through the yearly high at 1.3870 and towards a retest of the 2018 high at 1.4377 further up. Only a monthly close below 1.3000 negates. | ||

| ||

| R2 1.3509 - 25 May high - Strong R1 1.3400 - Figure - Medium S1 1.3302 - 18 May low - Strong S2 1.3219 - 13 March low - Medium | ||

| GBPUSD: fundamental overview | ||

| The Pound has been trading largely as a function of broader US Dollar dynamics, with investors balancing geopolitical developments, shifting central bank expectations, and a mixed domestic backdrop. An easing in direct hostilities between Israel and Iran has helped temper safe-haven demand for the Dollar, offering Sterling some support, although lingering uncertainty surrounding Iran’s nuclear program and the Strait of Hormuz continues to underpin defensive positioning in FX markets. At the same time, stronger-than-expected US labor market data and expectations for firmer US inflation have reinforced the view that the Federal Reserve could maintain a hawkish bias for longer, limiting GBPUSD upside. On the UK side, a sharp rebound in May BRC retail sales provided a rare positive surprise for the domestic economy, though markets have been reluctant to extrapolate too much from the data given concerns that April GDP likely contracted and growth momentum remains fragile. The Bank of England also finds itself in a difficult position, with policymakers increasingly acknowledging that higher energy costs could keep inflation elevated even as economic activity softens. While some officials have signaled concern about broadening price pressures, the market expects the BoE to remain on hold at its upcoming meeting, leaving Sterling without a strong domestic policy catalyst. As a result, attention remains firmly fixed on incoming US CPI data and Friday’s UK GDP release, both of which have the potential to reshape expectations for the Fed and the BoE and drive the next meaningful move in the Pound. | ||

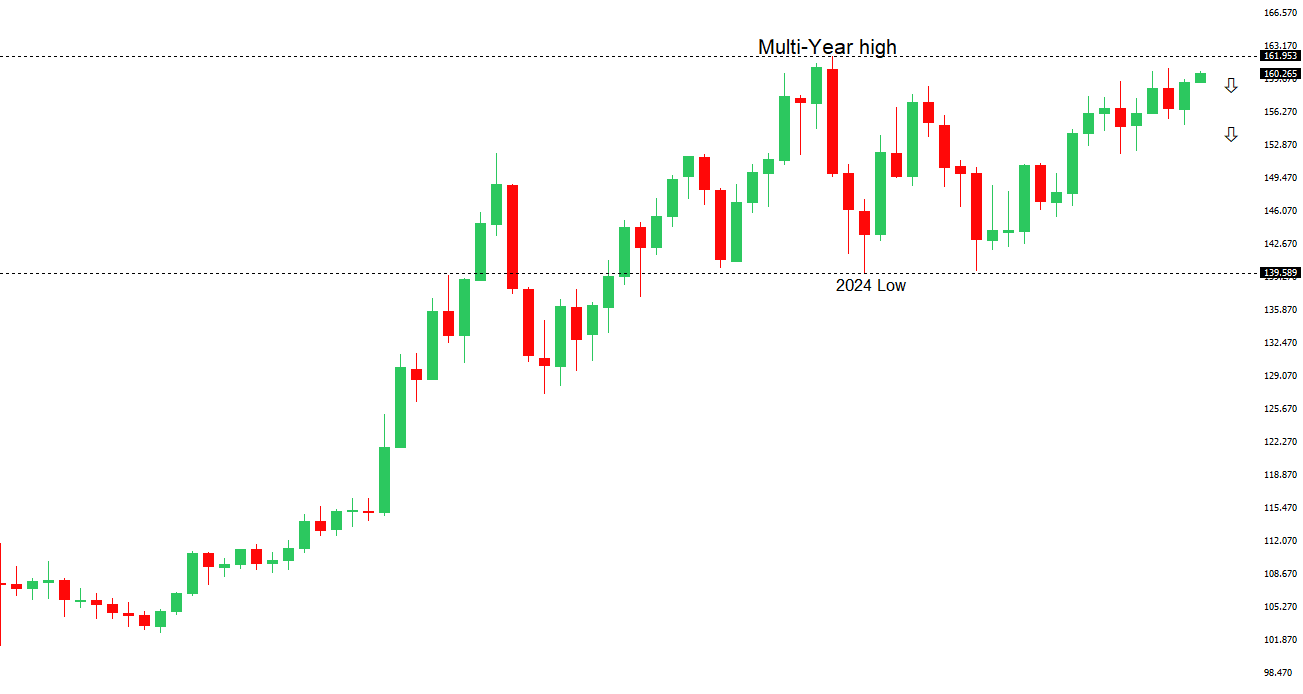

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped above 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 160.00 negates. | ||

| ||

| R2 160.73 - 30 April/2026 high - Strong R1 160.45 - 9 June high - Strong S1 159.37 - 3 June low - Medium S2 158.59 - 20 May low - Medium | ||

| USDJPY: fundamental overview | ||

| The Yen remains under pressure as escalating tensions in the Middle East continue to weigh on Japan’s economic outlook and support safe-haven demand for the US Dollar, keeping USDJPY pinned near the critical 160.50 intervention zone. Although Japan’s latest Producer Price Index surprised to the upside, reinforcing expectations that the Bank of Japan will continue normalizing policy, markets remain unconvinced that additional tightening alone will be sufficient to materially narrow the still-wide US-Japan yield differential. Investors are increasingly treating an expected BoJ rate hike to 1.00% at next week’s meeting as a foregone conclusion, with some economists projecting rates could rise further later this year. However, stronger US data, reduced expectations for Federal Reserve easing, and concerns that higher energy prices stemming from Middle East disruptions will disproportionately hurt energy-importing Japan have continued to undermine the Yen. At the same time, repeated warnings from Japanese officials that they stand ready to act against excessive currency moves, particularly with USDJPY trading back near levels that previously triggered record intervention, are helping to limit more aggressive Yen selling. Attention now turns to upcoming US inflation data, with hotter-than-expected CPI or PPI readings likely to reinforce the higher-for-longer Fed narrative and potentially push USDJPY further into intervention territory, while softer inflation outcomes could offer the Yen a temporary reprieve. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7201 - 29 May high - Strong R1 0.7100 - Figure - Medium S1 0.7005 - 9 June low - Medium S2 0.6963 - 8 April low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian Dollar remains under pressure following mixed Chinese inflation data that offered little fresh directional impetus. China’s May CPI rose 1.2% annually, slightly below expectations, suggesting domestic demand remains uneven, while stronger-than-expected producer prices pointed to firmer industrial activity and resilience in parts of the manufacturing sector. Given China’s status as Australia’s largest trading partner, these data points remain important for the Aussie through trade and commodity demand channels, although the market reaction has been muted. More broadly, sentiment toward the AUD continues to be shaped by global risk dynamics, with renewed US strikes on Iran boosting safe-haven demand for the US Dollar and tempering hopes for a lasting Middle East peace deal. At the same time, the Australian currency is finding some support from expectations the RBA will maintain a relatively hawkish bias compared with several of its global peers, particularly as policymakers remain alert to persistent domestic inflation pressures. Looking ahead, traders are likely to remain cautious ahead of the latest US inflation data, which could significantly influence Federal Reserve expectations, Treasury yields, and broader risk appetite, all of which remain key drivers for the direction of AUDUSD. | ||

| Suggested reading | ||

| Wall Street Races “Onchain,” & the Scramble Begins, E. Ekshian, RCM (June 9, 2026) An Average Economy: Not Great, Not Terrible, J. Calhoun, Alhambra (June 4, 2026) | ||