| ||

| 9th June 2026 | view in browser | ||

| Risk returns, but the hard part lies ahead | ||

| Markets head into Tuesday with risk sentiment improving as investors look through recent geopolitical tensions, while turning their attention to key US inflation data, an expected ECB rate hike, persistent BOJ tightening speculation, and the sustainability of AI-driven gains in global equity markets. | ||

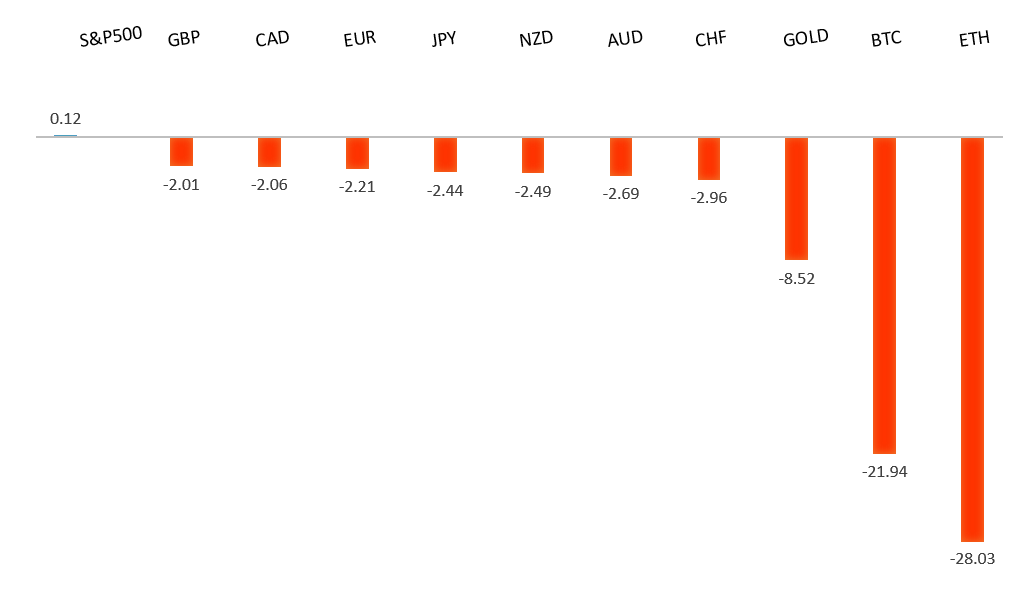

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1646 - 4 June high - Medium R1 1.1576 - 21 May low - Medium S1 1.1500 - 8 June low - Medium S2 1.1443 - 30 March low - Medium | ||

| EURUSD: fundamental overview | ||

| The euro has been trading with a mixed bias, supported by expectations that the ECB will deliver another 25bp rate hike this week after Eurozone inflation accelerated to 3.2%, reinforcing the central bank’s hawkish stance and keeping the prospect of additional tightening on the table. Recent data has also been modestly encouraging, with Eurozone Sentix investor confidence improving in June, suggesting sentiment is becoming less pessimistic despite ongoing growth concerns. At the same time, upside in the single currency has been capped by renewed geopolitical uncertainty in the Middle East, with investors gravitating toward the safe-haven US Dollar after comments from Israeli Prime Minister Netanyahu indicated the conflict with Iran and Hezbollah may not yet be over. Looking ahead, the market’s focus is squarely on Thursday’s ECB decision and President Lagarde’s guidance on the policy outlook, while Wednesday’s US CPI report could also prove pivotal for EURUSD by influencing expectations around the Federal Reserve path and broader US Dollar direction. | ||

| GBPUSD: technical overview | ||

| The Pound remains exceptionally well supported on dips into the 1.3000 area, with the price largely consolidating above the psychological barrier and previous resistance turned support in the form of the 2023 high. Look for the market to continue be well supported on dips ahead of the next major upside extension through the yearly high at 1.3870 and towards a retest of the 2018 high at 1.4377 further up. Only a monthly close below 1.3000 negates. | ||

| ||

| R2 1.3509 - 25 May high - Strong R1 1.3400 - Figure - Medium S1 1.3302 - 18 May low - Strong S2 1.3219 - 13 March low - Medium | ||

| GBPUSD: fundamental overview | ||

| The pound is finding solid underlying support on dips, backed by the UK’s one of the highest policy rates in the G7 (tied with the US at 3.75%) and a resilient inflation outlook that keeps the Bank of England from cutting rates aggressively. Despite a stronger-than-expected US jobs report reinforcing expectations of a more restrictive Federal Reserve that could even hike later in 2026, the yield advantage and BoE’s cautious stance continue to provide a firm floor for Sterling. While the BoE remains mindful of weakening growth, elevated energy prices are expected to keep inflation risks tilted higher toward 4%, limiting the scope for rapid easing and reinforcing rate support for the pound. The recent Israel-Lebanon ceasefire has improved risk sentiment and reduced safe-haven flows into the dollar, offering further tailwinds for GBPUSD on dips, even as lingering geopolitical tensions around Iran, the Gulf, and the Strait of Hormuz maintain a cautious backdrop. With traders now looking toward Friday’s UK GDP data for signs of resilience and tomorrow’s US inflation and labor market releases for Fed clues, the overall setup leaves GBPUSD well-supported on weakness while remaining capped by superior US fundamentals, favoring a range-bound to modestly constructive bias. | ||

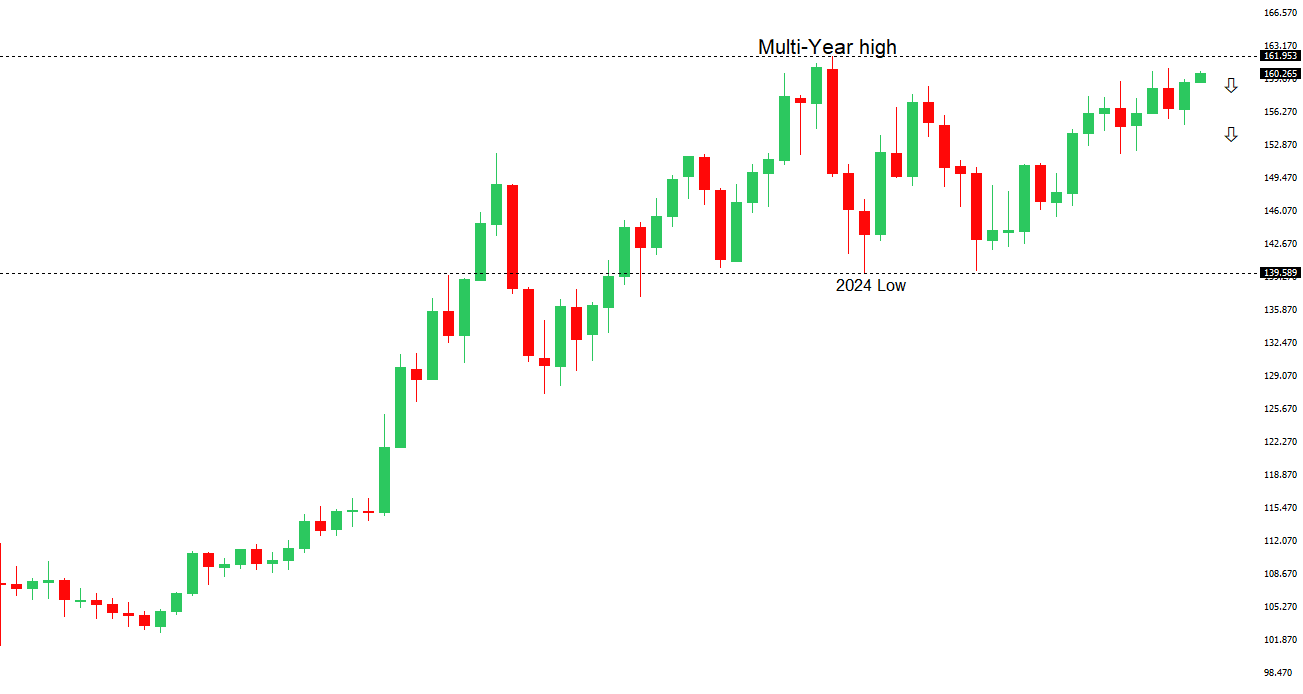

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped above 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 160.00 negates. | ||

| ||

| R2 160.73 - 30 April/2026 high - Strong R1 160.40 - 8 June high - Strong S1 159.37 - 3 June low - Medium S2 158.59 - 20 May low - Medium | ||

| USDJPY: fundamental overview | ||

| The yen remains primarily driven by the widening policy divergence between the Bank of Japan and the Federal Reserve, with stronger-than-expected US employment data reinforcing expectations that US rates will remain higher for longer and helping keep USDJPY above the psychologically important 160.00 level. At the same time, the yen continues to draw support from rising expectations for further BoJ policy normalization after stronger Japanese wage growth data reinforced the case for additional tightening later this month. However, the dominant theme remains growing intervention risk, with Japanese Finance Minister Katayama again warning that authorities stand ready to take decisive action against excessive currency weakness, while many market participants increasingly view the 160.00 area as a potential trigger point for official action. A modest easing in Israel-Iran tensions has also reduced safe-haven demand for both the US dollar and yen, leaving interest rate differentials and intervention concerns as the key drivers of price action ahead of this week’s US inflation data, which could significantly influence expectations for the Fed and the next move in USDJPY. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7201 - 29 May high - Strong R1 0.7100 - Figure - Medium S1 0.7018 - 8 June low - Medium S2 0.6963 - 8 April low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar is finding support from an improving global risk backdrop and encouraging Chinese economic data, with AUDUSD rebounding toward 0.7050 after recent two-month lows. Easing tensions in the Middle East have weighed on the US dollar as oil prices retreat and investors become more willing to embrace risk, providing a tailwind for the Aussie. At the same time, stronger-than-expected Chinese trade figures have reinforced the outlook for Australia’s largest trading partner, with exports and imports both accelerating sharply in May, highlighting resilient demand for commodities, semiconductors and AI-related hardware. Domestically, the broader fundamental picture remains constructive, supported by still-elevated inflation and a Reserve Bank of Australia that continues to signal a cautious, hawkish stance, keeping the prospect of lower rates distant for now. While Australia’s economy has shown some signs of moderation through softer growth and a cooling labor market, inflation remains above target and policymakers continue to emphasize that policy must stay restrictive. As a result, the medium-term outlook for the Aussie remains underpinned by relatively high Australian yields, resilient domestic fundamentals and stabilization in China, although near-term direction continues to depend heavily on global risk sentiment, US dollar dynamics and geopolitical developments. | ||

| Suggested reading | ||

| Investors Confront The Reality of the AI Business, B. Berkowitz, Axios (June 7, 2026) The Media Obsession With Nvidia & China, J. Tamny, Forbes (June 4, 2026) | ||