| ||

| 25th June 2025 | view in browser | ||

| Ceasefire holds, Fed rate cuts in focus | ||

| The Israel-Iran ceasefire continues to hold, easing geopolitical tensions, while markets focus on rising odds of Fed rate cuts by July, with Fed Chair Powell’s testimony today at 2:00 PM GMT expected to provide further clarity. | ||

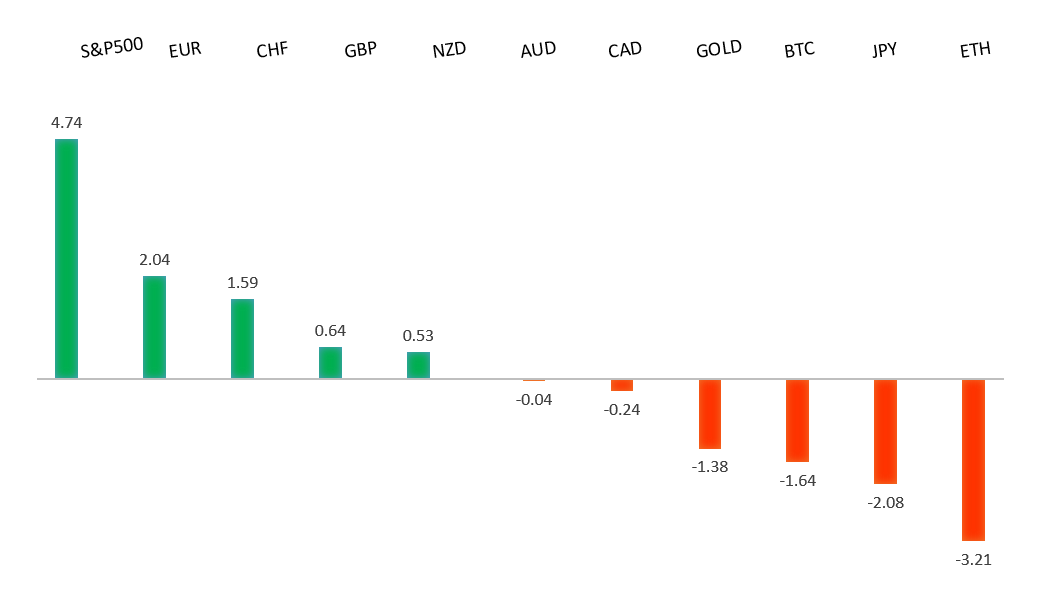

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro has finally broken out from a multi-month consolidation off a critical longer-term low. This latest push through the 2023 high lends further support to the case for a meaningful bottom, setting the stage for a bullish structural shift and the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported below 1.1000. | ||

| ||

| R2 1.1693 - 28 October 2024 high - Strong R1 1.1642 - 24 June/2025 high - Medium S1 1.1446 - 19 June low - Medium S2 1.1373 - 10 June low - Medium | ||

| EURUSD: fundamental overview | ||

| A recent OMFIF report forecasts that 16% of central banks will increase euro holdings in the next 12-24 months, potentially raising the euro’s global reserve share to 25% by decade’s end, driven by EU bond market expansion and rising demand in cross-currency swaps, which could make borrowing in euros costlier than dollars. Dovish Fed signals from Waller and Bowman, alongside weak U.S. data, boost expectations for 2025 rate cuts, while the ECB nears the end of its easing cycle with inflation near 2%, supporting EURUSD strength. Germany’s plan to borrow €118.5 billion in 2025 for public and military spending signals sustained fiscal stimulus, further bolstering the euro. Upcoming German Gfk Consumer Confidence data, expected to rise to -19.2, reflects cautious optimism but remains sensitive to geopolitical or economic shocks. | ||

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, the door is now open for a deeper setback below the 2024 low at 139.58 over the coming weeks, exposing a retest of the 2023 low. Rallies should be well capped below 150.00. | ||

| ||

| R2 148.65 - 12 May high - Medium R1 148.03 - 23 June high - Medium S1 144.32 - 18 June low - Medium S2 142.79 - 13 June low - Medium | ||

| USDJPY: fundamental overview | ||

| The Yen is recovering as oil prices ease following a ceasefire between Israel and Iran, reducing pressure on Japan’s energy-dependent economy after U.S. strikes on Iranian nuclear sites had driven oil higher. Dovish comments from Fed officials Waller and Bowman, hinting at a possible July rate cut, have weakened the USDJPY pair, while Japan’s tariff negotiator prepares for U.S. talks on June 26, aiming to secure a favorable trade deal to support BOJ rate hike expectations. BOJ’s Tamura advocates for decisive rate hikes if inflation risks rise, with Tokyo’s June CPI data on June 26 potentially adding pressure for action, as May’s PPI Services at 3.3% signals persistent domestic inflation. Declining department store sales (-7.0% YoY nationwide, -9.1% in Tokyo) highlight retail challenges, but markets expect tariff uncertainties to stabilize as Trump focuses on economic stimulus, potentially extending tariff deadlines. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6553 - 16 June/2025 high - Strong R1 0.6500 - Psychological - Medium S1 0.6373 - 23 June low - Medium S1 0.6344 - 24 April low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar is regaining ground, tracking the Chinese yuan’s strength (fixed at 7.1656, its highest since November), as Trump’s Israel-Iran ceasefire reduces the dollar’s geopolitical risk premium. Australia’s May CPI fell to 2.1%, below the expected 2.3%, with trimmed mean CPI dropping to 2.4% from 2.8%, signaling easing inflation pressures and increasing the likelihood of an RBA rate cut on July 8. Markets now await early July retail sales and household spending data, where weak figures could confirm the case for monetary easing. | ||

| Suggested reading | ||

| The fight to save Filipino chocolate, B. Harani, Financial Times (June 25, 2025) More Than Trump Grasps, the Fed Is Irrelevant, J. Calhoun, Alhambra (June 22, 2025) | ||