| ||

| 16th June 2026 | view in browser | ||

| Central banks take the baton as geopolitics fade from the driver’s seat | ||

| Markets are increasingly looking beyond the Middle East ceasefire framework and refocusing on central bank divergence, with the BOJ’s hike failing to lift the yen, the RBA maintaining a cautious hawkish hold, risk assets supported by easing oil prices, and investors awaiting fresh guidance from the Federal Reserve. | ||

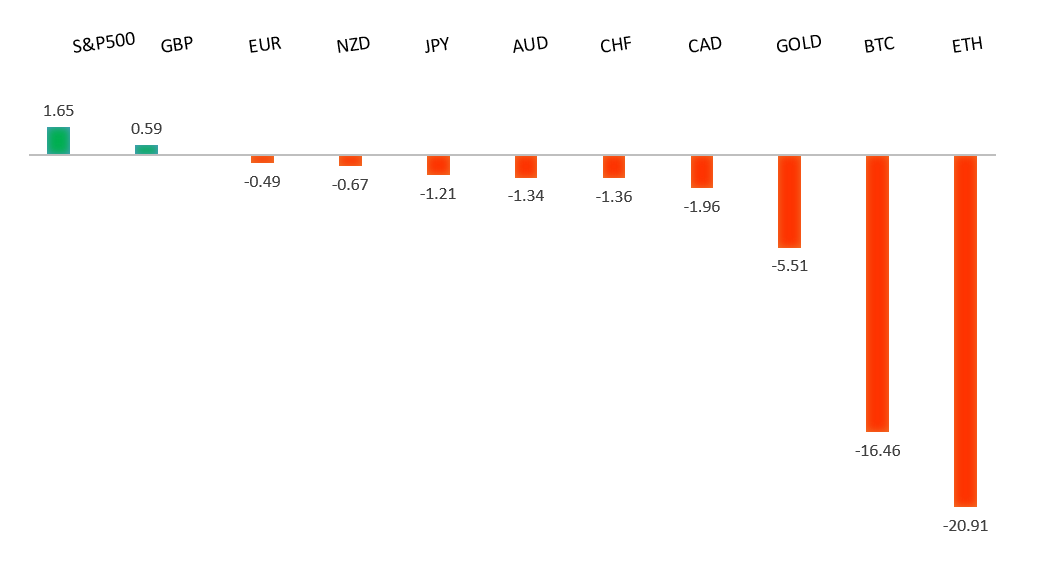

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1686 - 29 May high - Strong R1 1.1646 - 4 June high - Medium S1 1.1557 - 12 June low - Medium S2 1.1500 - 8 June low - Strong | ||

| EURUSD: fundamental overview | ||

| The euro remains underpinned by a combination of improving global risk sentiment and expectations that the European Central Bank may still have further tightening to deliver, even as the Federal Reserve is widely anticipated to leave rates unchanged this week. The latest catalyst supporting EURUSD has been optimism surrounding a US-Iran agreement aimed at reopening the Strait of Hormuz and initiating a fresh round of nuclear negotiations, easing concerns over a prolonged disruption to global energy supplies and weighing on safe-haven demand for the US Dollar. While lingering uncertainty over the final details of the agreement has tempered enthusiasm somewhat, the broader improvement in market sentiment has continued to favor the shared currency. At the same time, investors remain mindful that the ECB has maintained a relatively hawkish bias amid persistent underlying inflation pressures, with markets still pricing in the possibility of additional policy tightening in the months ahead. Attention now turns to the Federal Reserve, where policymakers are expected to keep rates steady, with the tone of Chair Warsh’s guidance and any signals around the timing of future policy adjustments likely to determine whether the dollar can regain traction or allow the euro to extend its recent gains. | ||

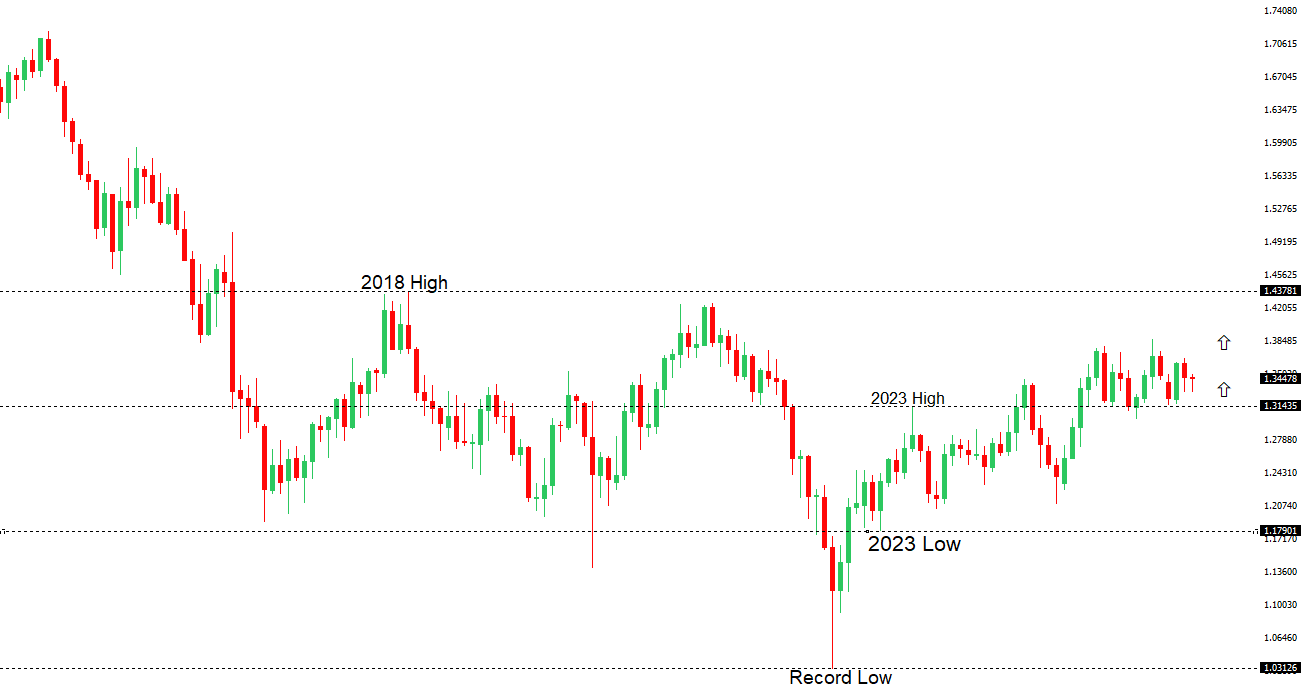

| GBPUSD: technical overview | ||

| The Pound remains exceptionally well supported on dips into the 1.3000 area, with the price largely consolidating above the psychological barrier and previous resistance turned support in the form of the 2023 high. Look for the market to continue be well supported on dips ahead of the next major upside extension through the yearly high at 1.3870 and towards a retest of the 2018 high at 1.4377 further up. Only a monthly close below 1.3000 negates. | ||

| ||

| R2 1.3509 - 25 May high - Strong R1 1.3486 - 29 May high - Medium S1 1.3383 - 12 June low - Strong S2 1.3302 - 18 May low - Strong | ||

| GBPUSD: fundamental overview | ||

| The Pound remains caught between shifting global risk sentiment and a pivotal week of central bank and economic event risk. Sterling initially benefited from improved market mood following reports of a US-Iran agreement to reopen the Strait of Hormuz, which helped drive a rally in risk-sensitive assets and weighed on the US Dollar. However, that optimism has faded somewhat as investors await further details surrounding the proposed deal and turn their focus toward the Federal Reserve’s policy decision. The Fed is widely expected to leave rates unchanged this week, but with US inflation proving sticky and labor market conditions remaining resilient, markets continue to price a hawkish bias that has lent underlying support to the Greenback. On the domestic front, the Pound faces an important test from upcoming UK CPI data and the Bank of England meeting, with policymakers also expected to keep rates on hold. Nevertheless, the UK inflation backdrop remains relatively elevated and Sterling has generally outperformed many of its G10 peers in recent weeks on expectations that the BoE may need to maintain restrictive policy settings for longer than previously anticipated. In the near term, GBPUSD appears to be trading more as a function of broad US Dollar dynamics and global risk appetite, but this week’s combination of UK inflation data, the BoE decision and the Fed’s updated guidance is likely to determine whether the Pound can regain momentum above the mid-1.34s or extend its consolidation around the 1.3400 area. | ||

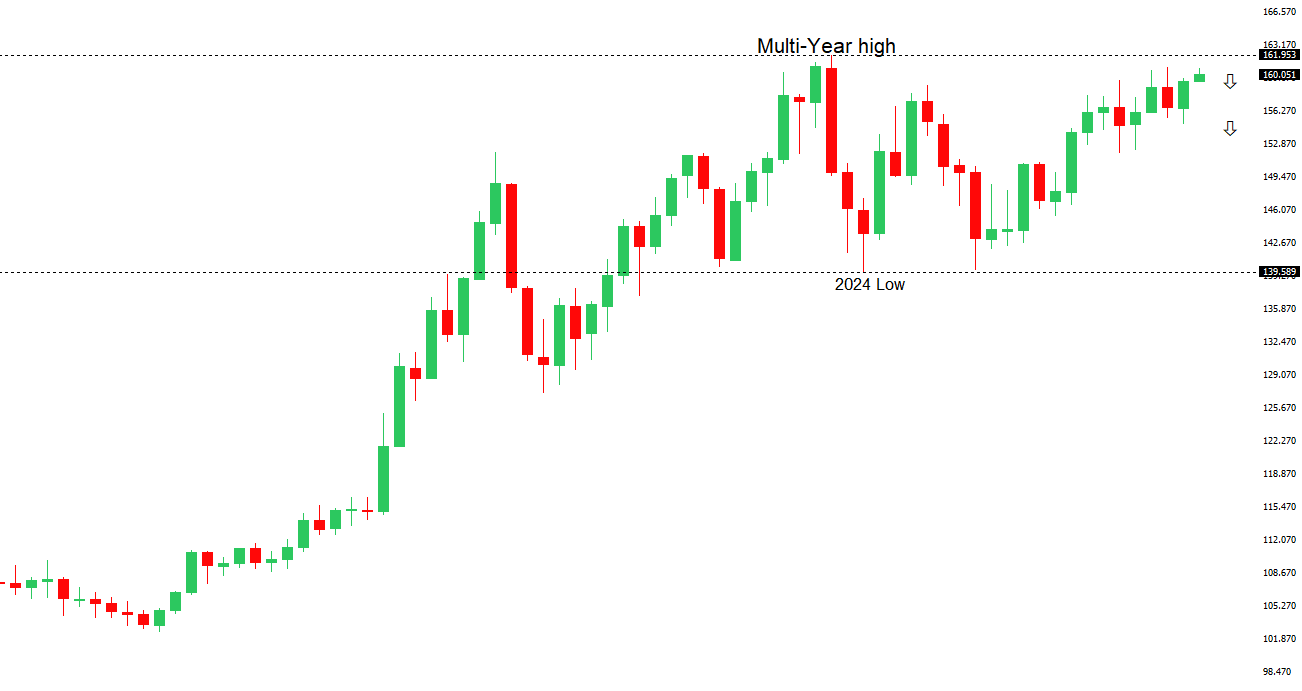

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped above 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 160.00 negates. | ||

| ||

| R2 160.73 - 30 April/2026 high - Strong R1 160.60 - 11 June high - Strong S1 159.54 - 11 June low - Medium S2 158.59 - 20 May low - Medium | ||

| USDJPY: fundamental overview | ||

| The Yen remains primarily driven by the Bank of Japan’s decision to raise interest rates by 25 basis points to 1.0%, marking another step in the gradual normalization of monetary policy as policymakers respond to persistent inflationary pressures and stronger wage dynamics. The BoJ maintained a hawkish tilt, signaling that further rate increases remain possible should economic activity and prices evolve in line with its forecasts, while warning that underlying inflation risks could overshoot its 2% target amid rising energy costs and broadening price pressures. However, the Yen’s gains have been limited as the rate hike was fully priced in by markets, with investors instead focusing on guidance from Deputy Governor Uchida following Governor Ueda’s hospitalization. Expectations that the BoJ will proceed cautiously from here, combined with concerns that the Japanese government may adopt a more expansionary fiscal stance to cushion households from elevated living costs, have tempered prospects for an aggressive tightening cycle. As a result, USDJPY has remained anchored above the psychologically important 160 level, with traders balancing the supportive impact of higher Japanese rates against lingering uncertainty over the pace of future BoJ hikes, fiscal policy developments, and external risks stemming from Middle East tensions and their potential impact on global energy prices. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7201 - 29 May high - Strong R1 0.7100 - Figure - Medium S1 0.6979 - 11 June low - Medium S2 0.6963 - 8 April low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian Dollar has been driven by a combination of a still-hawkish Reserve Bank of Australia, improving global risk sentiment and evolving expectations around the outlook for both China and the US Dollar. The RBA left the cash rate unchanged at 4.35% as expected, with Governor Bullock stressing that inflation remains too high and reiterating that policymakers remain prepared to tighten further if required, even though the Board did not consider a rate increase at this meeting. While Bullock acknowledged that recent easing in geopolitical tensions and softer inflation expectations were welcome developments, she emphasized that upside inflation risks persist and that demand still needs to moderate before price pressures can return sustainably to target. Domestically, the Australian economy continues to show resilience, supported by solid demand, a rebound in the trade surplus and inflation that is proving sticky enough to justify the RBA’s cautious stance, although softer GDP growth and signs of labor market cooling have tempered expectations for additional tightening. Externally, the Aussie remains highly sensitive to swings in global sentiment, with optimism surrounding the US-Iran peace agreement and the reopening of the Strait of Hormuz providing support to risk-sensitive assets. Meanwhile, China has shifted from being a major growth engine to more of a stabilizing force for Australia, with mixed activity data offset by an improving trade backdrop. Overall, the broader fundamental backdrop for the Australian Dollar remains constructive, underpinned by the RBA’s hawkish bias and resilient domestic conditions, but further gains are likely to depend on continued improvement in global risk appetite, steady Chinese demand and a softer US Dollar environment. | ||

| Suggested reading | ||

| Arson attacks targeting Keir Starmer properties originated in Russia, M. Johnson, FT (June 15, 2026) Despite Recent Market Moves, ’26 Has Been Calm, Fisher Investments (June 12, 2026) | ||