| ||

| 6th May 2025 | view in browser | ||

| Dollar steady, US equity futures under pressure | ||

| The U.S. dollar remains largely unchanged, while U.S. stock futures, led by a 0.5% decline in the NASDAQ, trade modestly lower, as markets digest mixed global signals. | ||

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

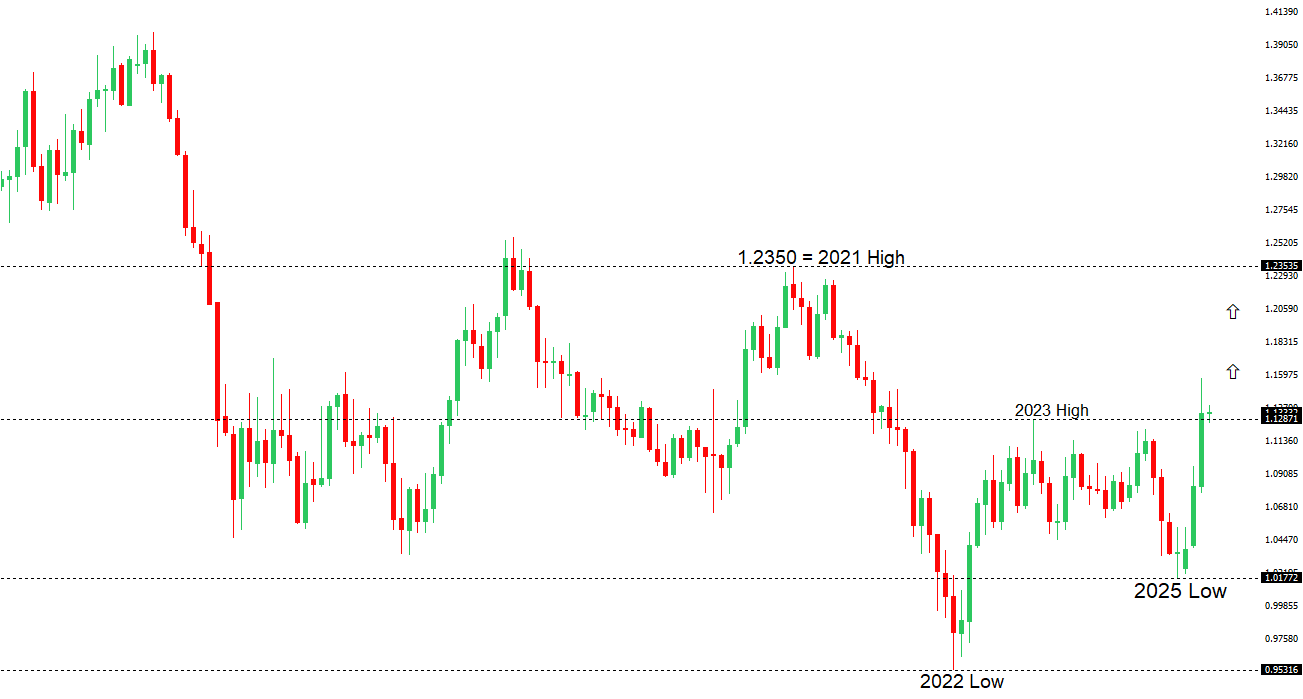

| EURUSD: technical overview | ||

| The Euro has finally broken out from a multi-month consolidation off a critical longer-term low. This latest push through the 2023 high lends further support to the case for a meaningful bottom, setting the stage for a bullish structural shift and the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported below 1.1000. | ||

| ||

| R1 1.1574 - 21 April/2025 high - Strong R1 1.1426 - 28 April high - Medium S1 1.1266 - 1 May low - Medium S2 1.1148 - 3 April high - Strong | ||

| EURUSD: fundamental overview | ||

| The European Central Bank, as echoed by Governing Council member Stournaras and President Lagarde, is poised to continue its data-dependent rate cuts amid persistent uncertainty. At the same time, the Euro should still be supported on a more dovish Fed track, driven by expected Federal Reserve rate reductions and economic strain from U.S. tariff policies. KKR & Co.’s Henry Kravis has expressed confidence in European leadership, particularly praising German Chancellor Friedrich Merz, French President Emmanuel Macron, and Italian PM Giorgia Meloni, signaling Europe as an attractive investment destination. Eurozone investor sentiment has improved significantly, with the May Sentix Investor Confidence Index rising to -8.1, bolstered by the European Commission’s steady response to U.S. trade actions and expectations of continued ECB rate cuts. Upcoming March PPI data, projected to decline to -1.40% month-on-month, reflects easing energy costs and normalizing supply chains, though sticky core inflation at 2.7% year-on-year underscores persistent service-driven price pressures. | ||

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, the door is now open for a deeper setback below the 2024 low at 139.58 over the coming sessions exposing a retest of the 2023 low. Rallies should be well capped below 150.00. | ||

| ||

| R2 148.28 - 9 April high - Strong R1 145.93 - 2 May high - Medium S1 143.73 - 2 May low - Medium S1 141.97 - 29 April low - Medium | ||

| USDJPY: fundamental overview | ||

| The Bank of Japan’s decision to delay its 2% inflation target and cut growth forecasts to 0.5% amid global trade uncertainties has diminished expectations for near-term rate hikes, with USDJPY facing resistance in recent sessions as markets await Federal Reserve guidance from the May 7 FOMC meeting, where 78 basis points of rate cuts are priced in for 2025. Despite stalled U.S.-Japan trade talks, with the U.S. rejecting Japan’s full tariff exemption but open to reducing the 14% Japan-specific tariff, Chief Negotiator Ryosei Akazawa remains optimistic about a June agreement, potentially paving the way for the BOJ to resume rate hikes, with Bloomberg Economics projecting a target rate of 1.25% by next year. The strengthening of Asian currencies, particularly the undervalued Chinese yuan, could support further yen appreciation, while upcoming BOJ March meeting minutes and Thursday’s household spending data will provide additional insights, though Japanese markets are closed again today for holidays. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6500 - Psychological - Strong R1 0.6482 - 5 May/2025 high - Medium S1 0.6344 - 24 April low - Medium S1 0.6275 - 14 April low - Strong | ||

| AUDUSD: fundamental overview | ||

| Prime Minister Albanese’s resounding election victory has strengthened Australia’s political stability, providing a temporary lift to the Australian dollar, while markets await progress in U.S.-China trade talks, with the strengthening Chinese yuan—now below its 200-day moving average—potentially bolstering Aussie as a regional proxy. The Federal Reserve’s upcoming May 7 FOMC meeting, expected to maintain current rates despite tariff-related economic pressures, will be scrutinized for signs of a shift toward rate cuts, with markets anticipating 78 basis points of reductions in 2025. In Australia, persistent inflationary pressures, evidenced by April’s Melbourne Institute Inflation at 3.3% year-on-year and rising consumer inflation expectations to 4.2%, alongside disappointing March household spending, suggest that the Reserve Bank of Australia’s projected 104 basis points of rate cuts for 2025 may be overly optimistic, as weak consumption signals caution for economic growth. | ||

| Suggested reading | ||

| Wall Street’s $5 Trillion Robot Bet, J. Remsburg, Investor Place (May 2, 2025) Is Software Holding the U.S. Hostage?, I. King, Banyan Hill (May 5, 2025) | ||