| ||

| 9th July 2026 | view in browser | ||

| From Fed focus to frontline risk | ||

| Geopolitical tensions in the Middle East continue to dominate markets, driving oil sharply higher and keeping risk sentiment cautious, while a largely expected hawkish Fed Minutes prompted a “sell-the-fact” pullback in the US dollar and helped fuel a late rebound in US equities. | ||

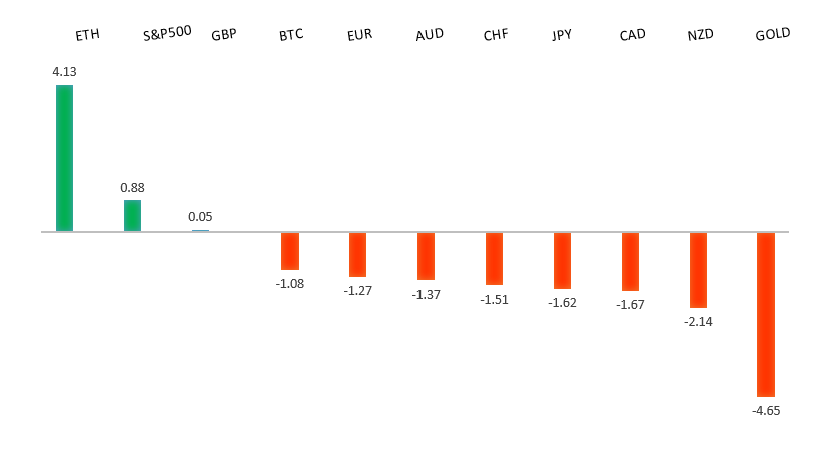

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1529 - 18 June high - Medium R1 1.1473 - 2 July high - Medium S1 1.1325 - 24 June/2026 low - Medium S2 1.1300 - Figure - Medium | ||

| EURUSD: fundamental overview | ||

| The euro is trading with a modestly firmer tone against the US dollar after recovering from earlier losses as broad-based dollar selling outweighed support for the greenback from renewed geopolitical tensions and a hawkish set of Federal Reserve minutes. While the Fed reinforced a higher-for-longer policy message and kept the prospect of further tightening on the table if inflation remains stubborn, markets focused more on softer US growth expectations and recent signs of labor market cooling, limiting the dollar’s upside. On the euro side, expectations that the European Central Bank may need to keep policy restrictive have been supported by comments from ECB policymakers, including Schnabel and Panetta, who warned that heightened tensions in the Middle East and the risk of energy supply disruptions through the Strait of Hormuz could sustain inflationary pressures despite a fragile growth backdrop. That combination of persistent inflation risks and cautious central bank rhetoric has helped underpin the single currency, although escalating US-Iran tensions and the resulting risk-off mood continue to cap upside as investors weigh the implications of higher energy prices and slower global growth. | ||

| GBPUSD: technical overview | ||

| The Pound remains exceptionally well supported on dips into the 1.3000 area, with the price largely consolidating above the psychological barrier and previous resistance turned support in the form of the 2023 high. Look for the market to continue be well supported on dips ahead of the next major upside extension through the yearly high at 1.3870 and towards a retest of the 2018 high at 1.4377 further up. Only a monthly close below 1.3000 negates. | ||

| ||

| R2 1.3461 - 15 June high - Medium R1 1.3411 - 8 July high - Medium S1 1.3262 - 2 July low - Medium S2 1.3212 - 30 June low - Medium | ||

| GBPUSD: fundamental overview | ||

| The pound has found renewed support as broad-based US Dollar weakness offsets lingering geopolitical uncertainty and mixed domestic fundamentals, allowing GBPUSD to push back above the 1.3400 level. Markets continue to price a more hawkish path from the Bank of England, with expectations for at least one additional rate hike this year firming amid persistent services inflation and renewed upside risks to energy prices following the escalation in Middle East tensions. However, sterling’s gains remain tempered by evidence of a slowing UK economy, including softer activity, easing wage growth and a weakening labor market, reinforcing the difficult balancing act facing policymakers between containing inflation and supporting growth. Political developments are also in focus following Prime Minister Starmer’s resignation, although expectations of policy continuity under likely successor Andy Burnham have helped limit market uncertainty. Meanwhile, the latest FOMC minutes reinforced the prospect of US rates remaining higher for longer, but a subsequent pullback in the US Dollar has ultimately allowed sterling to regain the upper hand despite the broader backdrop of elevated geopolitical risks. | ||

| USDJPY: technical overview | ||

| The major pair has extended its run to fresh multi-decade highs, with the latest push through 160.00 opening the door for further upside towards 165.00-170.00. At the same time, daily studies are looking quite stretched, suggesting we could see a healthy correction on the horizon. A break back below 160.48 would now strengthen the case for a larger pullback. Until then, the market will continue to be focused on additional gains. | ||

| ||

| R2 163.00 - Figure - Medium R1 162.84 - Multi-Year high/1 July 2026 - Strong S1 161.00 - Figure - Medium S2 160.48 - 3 July low - Medium | ||

| USDJPY: fundamental overview | ||

| The yen remains under pressure as a widening US-Japan yield differential continues to favor the dollar, with hawkish Federal Reserve minutes reinforcing expectations that US interest rates will stay higher for longer and lifting Treasury yields. While renewed US-Iran tensions and concerns over the Strait of Hormuz have supported safe-haven demand for the greenback, the yen has failed to benefit meaningfully as investors remain focused on the Bank of Japan’s still-accommodative policy outlook. Dovish comments from BoJ board member Asada, who reiterated that clearer evidence of demand-driven inflation is needed before backing further rate hikes, reinforced expectations that any additional policy tightening will be gradual. At the same time, Japan’s dependence on imported energy leaves the yen vulnerable to higher oil prices stemming from geopolitical risks. Nevertheless, traders remain alert to the growing risk of official intervention as USDJPY trades near multi-decade highs, with speculative short-yen positioning still heavily stretched, raising the prospect of a sharp reversal should Japanese authorities decide to step into the market. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7089 - 15 June high - Strong R1 0.6979 - 11 June low - Medium S1 0.6865 - 30 June low - Medium S2 0.6833 - 30 March low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian dollar is trading in a relatively tight range as competing fundamental forces leave investors without a clear directional catalyst. On one hand, the currency continues to find support from the Reserve Bank of Australia’s still-hawkish policy stance, with policymakers maintaining that inflation remains too high to rule out further tightening despite recent signs of easing price pressures. On the other hand, the release of hawkish Federal Reserve minutes has reinforced expectations that US interest rates could remain higher for longer, limiting the Aussie’s upside by supporting the US dollar. Heightened geopolitical tensions in the Middle East have also created offsetting effects, weighing on broader risk sentiment while simultaneously boosting commodity prices, which offers some support to Australia’s terms of trade as a major energy exporter. However, with iron ore and Chinese demand remaining the key drivers of Australia’s external outlook, investors are now looking to China’s latest inflation data for clearer signals on the health of domestic demand and the broader economic recovery. Until either Chinese data or incoming US economic releases materially shift interest rate expectations, the Australian dollar is likely to remain driven by the balance between resilient commodity prices, global risk appetite and the evolving policy outlook from both the RBA and the Federal Reserve. | ||

| Suggested reading | ||

| Palantir: profits, procurement and power, J. Miller, Financial Times (July 8, 2026) Nothing in Investing is “Doing Nothing”, J. Wiggins, Behavioural Investment (July 8, 2026) | ||