| ||

| 18th August 2025 | view in browser | ||

| Geopolitics jolt markets | ||

| The U.S. dollar climbed to session highs late Monday after a key White House meeting involving President Trump, Ukrainian President Zelensky, and European leaders. | ||

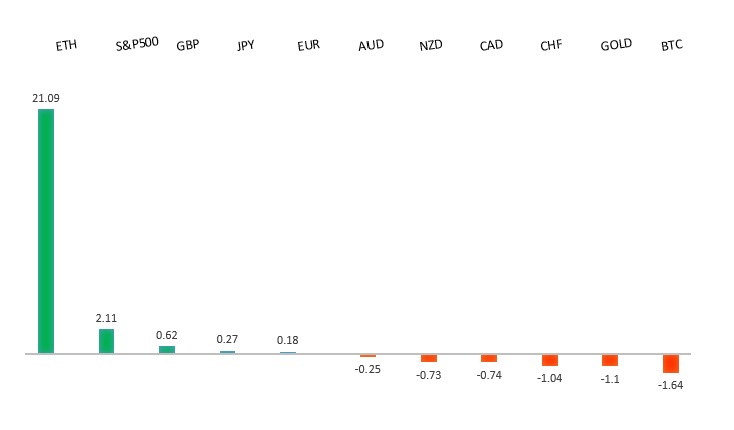

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro has broken out from a multi-month consolidation off a critical longer-term low. This latest push through the 2023 high (1.1276) lends further support to the case for a meaningful bottom, setting the stage for a bullish structural shift and the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1000. | ||

| ||

| R2 1.1789 - 24 July high - Medium R1 1.1731 - 13 August high - Medium S1 1.1528 - 5 August low - Medium S2 1.1392 - 1 August low - Strong | ||

| EURUSD: fundamental overview | ||

| Former President Trump has shifted toward Russia’s position in the Ukraine conflict, urging President Zelensky to accept a peace deal that involves conceding Crimea and abandoning NATO aspirations, while placing the burden of failed talks on Ukraine. With the U.S. holding key leverage through military aid, Ukraine faces pressure to agree to terms favoring Russia, which could set a precedent that might makes right but may also lower energy prices, benefiting the euro in the short term. Meanwhile, disappointing Eurozone trade data signals potential economic challenges, though recovery is expected, and divergent monetary policies between the ECB and the Fed could support a stronger euro through 2026. | ||

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, the door is now open for a deeper setback below the 2024 low at 139.58, exposing a retest of the 2023 low. Rallies should be well capped below 152.00. | ||

| ||

| R2 150.92 - 1 August high - Strong R1 148.52 - 12 August high - Medium S1 146.21 - 14 August low - Medium S2 145.85 - 24 July low - Strong | ||

| USDJPY: fundamental overview | ||

| Japan’s Q2 GDP growth bolsters its economic recovery and supports the Bank of Japan’s cautious move toward tighter monetary policy, with markets anticipating a potential rate hike in October if inflation remains high. Prime Minister Shigeru Ishiba, despite political setbacks, aims to leverage the positive economic data to strengthen his position. Rising US-Japan yield spreads and comments from US Treasury Secretary Bessent urging Japan to control inflation are supporting the yen, while upcoming July CPI data, expected to show inflation above 2%, could further fuel expectations for a BOJ rate hike. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6600 - Figure - Medium R1 0.6569 - 14 August high - Medium S1 0.6419 - 1 August low - Medium S1 0.6373 - 23 June low - Strong | ||

| AUDUSD: fundamental overview | ||

| Analysts expect the Reserve Bank of Australia to cautiously continue its gradual rate-cutting cycle, with the big four banks forecasting the Official Cash Rate to drop to 3.35% by the end of 2025, likely starting in November 2024 and possibly followed by another cut in early 2026, depending on inflation (2%-3%) and unemployment (4.3%-4.5%). The RBA’s cautious approach contrasts with a more dovish outlook for the U.S. Federal Reserve, which markets expect to cut rates by 53 basis points by year-end, compared to 36 basis points for the RBA, potentially supporting the Australian Dollar. Federal Reserve Chair Powell’s upcoming Jackson Hole speech and U.S. PMI data on August 21 could significantly influence Aussie, alongside Australian consumer confidence data. | ||

| Suggested reading | ||

| How bots came for our workflows and drudgery, I. Berwick, Financial Times (August 18, 2025) Powell’s Legacy and Fed Independence On the Line, N. Goodkind, Barron’s (August 15, 2025) | ||