| ||

| 18th August 2025 | view in browser | ||

| Tariffs and labor woes cloud outlook | ||

| Last week’s U.S. retail sales for July rose by 0.5% month-over-month, signaling robust consumer activity and easing some concerns, though analysts warn that a softening labor market and potential tariff impacts could weaken spending later in 2025. | ||

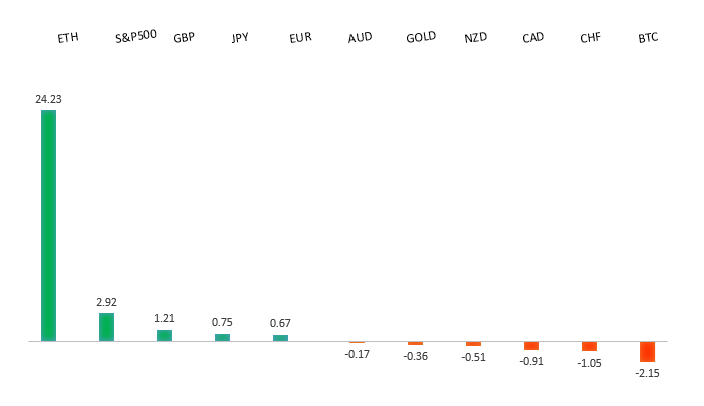

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro has broken out from a multi-month consolidation off a critical longer-term low. This latest push through the 2023 high (1.1276) lends further support to the case for a meaningful bottom, setting the stage for a bullish structural shift and the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1000. | ||

| ||

| R2 1.1789 - 24 July high - Medium R1 1.1731 - 13 August high - Medium S1 1.1528 - 5 August low - Medium S2 1.1392 - 1 August low - Strong | ||

| EURUSD: fundamental overview | ||

| Markets expect the Federal Reserve to cut rates at least three times by Q1 2026, while the ECB is likely to hold rates steady in September, awaiting updated projections. Some analysts suggest the ECB might hike rates later, driven by Germany’s fiscal stimulus, contrasting with the Fed’s easing path, which could boost the euro against the dollar. Key upcoming data, including Eurozone PMI and US PMI figures, along with the Jackson Hole symposium, will influence EURUSD movements. Two major US banks are bullish on the euro, targeting $1.20 by year-end and $1.22 by mid-2026, citing US inflation risks and growth moderation. Geopolitical developments, particularly from the Trump-Putin summit and follow-up talks with European leaders, could impact the dollar’s strength, with potential peace deals favoring the euro unless significant Ukrainian territorial losses raise long-term concerns. | ||

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, the door is now open for a deeper setback below the 2024 low at 139.58, exposing a retest of the 2023 low. Rallies should be well capped below 152.00. | ||

| ||

| R2 150.92 - 1 August high - Strong R1 148.52 - 12 August high - Medium S1 146.21 - 14 August low - Medium S2 145.85 - 24 July low - Strong | ||

| USDJPY: fundamental overview | ||

| Japan’s strong Q2 GDP growth supports the Bank of Japan’s cautious move toward gradual rate hikes, likely in October, if inflation remains high, with July’s CPI expected to stay elevated at 3.1%-3.3%. Prime Minister Ishiba, despite political setbacks, aims to leverage the positive economic outlook to stabilize his leadership. The narrowing yield spread between US and Japanese bonds, along with US Treasury Secretary Bessent’s comments urging Japan to manage inflation, supports the yen, though concerns linger about potential market volatility from rapid BOJ policy shifts. Additionally, Japan’s approval of a yen-backed stablecoin is expected to boost demand for government bonds and strengthen the yen’s role in the digital economy. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6600 - Figure - Medium R1 0.6569 - 14 August high - Medium S1 0.6419 - 1 August low - Medium S1 0.6373 - 23 June low - Strong | ||

| AUDUSD: fundamental overview | ||

| Recent strong Australian labor data suggests the Reserve Bank of Australia will continue a cautious, gradual rate-cutting cycle, with the big four banks predicting the Official Cash Rate will drop to 3.35% by the end of 2025, likely starting in November. The RBA’s moves depend on inflation staying within 2%-3% and unemployment between 4.3%-4.5%, while markets expect a more aggressive U.S. Federal Reserve cutting 55 basis points compared to 37 for the RBA, potentially supporting AUDUSD strength. China’s slowing economy, with weaker-than-expected industrial output, retail sales, and rising joblessness, may accelerate its consumer subsidy program, potentially boosting the Australian dollar through economic spillovers. Key upcoming Australian data, including consumer confidence, PMIs, and inflation expectations, alongside Fed Chair Powell’s Jackson Hole speech and U.S. PMI data, could significantly influence AUDUSD trends and RBA policy expectations. | ||

| Suggested reading | ||

| Jerome Powell’s Last Stand, N. Goodkind, Barron’s (August 15, 2025) The Dark Side Of The Artificial Intelligence Revolution, J. Horwitz, Reuters (August 14, 2025) | ||