| ||

| 9th December 2025 | view in browser | ||

| Hawkish cuts and the end of easing | ||

| Global markets are bracing for a turning point as central banks lean decisively less dovish. In the US, a widely expected Fed rate cut this week is likely to be framed hawkish, with Chair Powell signaling a long pause amid sticky global inflation and rising yields, even as political uncertainty grows around Powell’s eventual successor. | ||

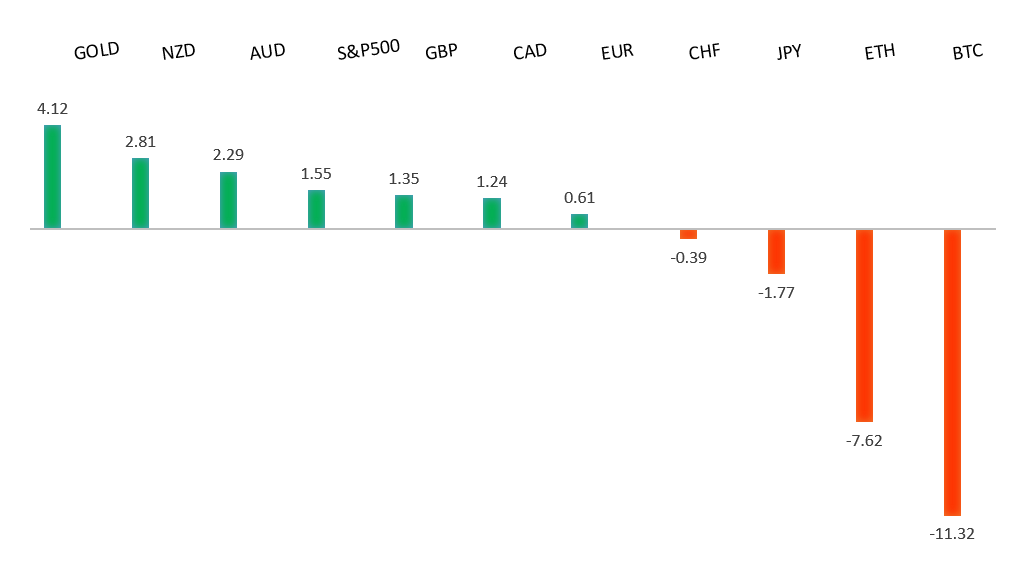

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1729 - 17 October high -Strong R1 1.1682 - 4 December high - Medium S1 1.1547 - 26 November low - Medium S2 1.1469 - 5 November low - Strong | ||

| EURUSD: fundamental overview | ||

| Germany’s October data point to tentative signs of stabilization rather than a strong recovery: industrial production rebounded by a much stronger-than-expected 1.8% month on month, supported by construction and capital goods, following a second consecutive rise in manufacturing orders. While this suggests German industry may be bottoming out, momentum still looks sideways. Planned government measures—potentially up to €1 trillion in investment and lower energy costs—could support a cyclical upswing. At the same time, ECB’s Isabel Schnabel signaled that rates are likely at their floor for now, noting resilient euro-area growth, sticky inflation, and possible upward revisions to ECB growth forecasts, while warning that disinflation has recently stalled and bears close watching. | ||

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, rallies should be well capped ahead of 160.00 ahead of a fresh down-leg back towards the 2024 low at 139.58. | ||

| ||

| R2 158.90 - 20 November/2025 high - Strong R1 156.59 - 28 November high - Medium S1 154.00 - Figure - Medium S2 153.61 - 14 November low - Strong | ||

| USDJPY: fundamental overview | ||

| USDJPY rebounded after reports of a major earthquake in northern Japan, as investors cautiously moved into the dollar while assessing whether the damage could delay the BOJ’s expected policy tightening. While past earthquakes have sometimes strengthened the yen through repatriation flows, markets currently assume damage is limited and still see a BOJ rate hike in December as the base case, albeit with risks of a longer pause given weak Q3 GDP and heightened caution after the quake. Looking ahead, further yen strength likely depends more on aggressive Fed rate cuts, as Japan’s combination of loose fiscal policy, cautious monetary tightening, and weak economic data—reinforced by disappointing November Eco Watchers survey results—continues to undermine confidence in a sustainably stronger yen. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6707 - 17 September/2025 high - Strong R1 0.6660 - 18 September high - Medium S1 0.6520 - 28 November low - Medium S2 0.6421 - 21 November low - Strong | ||

| AUDUSD: fundamental overview | ||

| The RBA kept the cash rate unchanged at 3.60%, but its December statement struck a mildly hawkish tone. By noting that inflation risks have tilted to the upside, private demand is recovering, and that it will do whatever is necessary to ensure price stability, the Bank pushed back against expectations for early rate cuts and left the door open to further tightening if needed. Markets appeared to have hoped for a softer message, which explains the muted initial AUD reaction. Separately, November NAB survey data showed business confidence easing to its lowest level since April while conditions remained solid, suggesting a cooling in momentum rather than a sharp downturn, with future risks depending on whether confidence and forward orders weaken further. | ||

| Suggested reading | ||

| Wall Street’s 2026 Outlook For Stocks, S. Ro, TKer (December 7, 2025) There’s An Inevitable Quality To the FOMC Meeting, R. Moody, Regions Bank (December 8, 2025) | ||