| ||

| 11th December 2025 | view in browser | ||

| New day, new divergences | ||

| Global markets are navigating a sharply diverging policy landscape, with the Fed signaling its easing cycle is nearly finished just as the ECB and BoJ turn more hawkish, driving major currency moves and shifting rate expectations. | ||

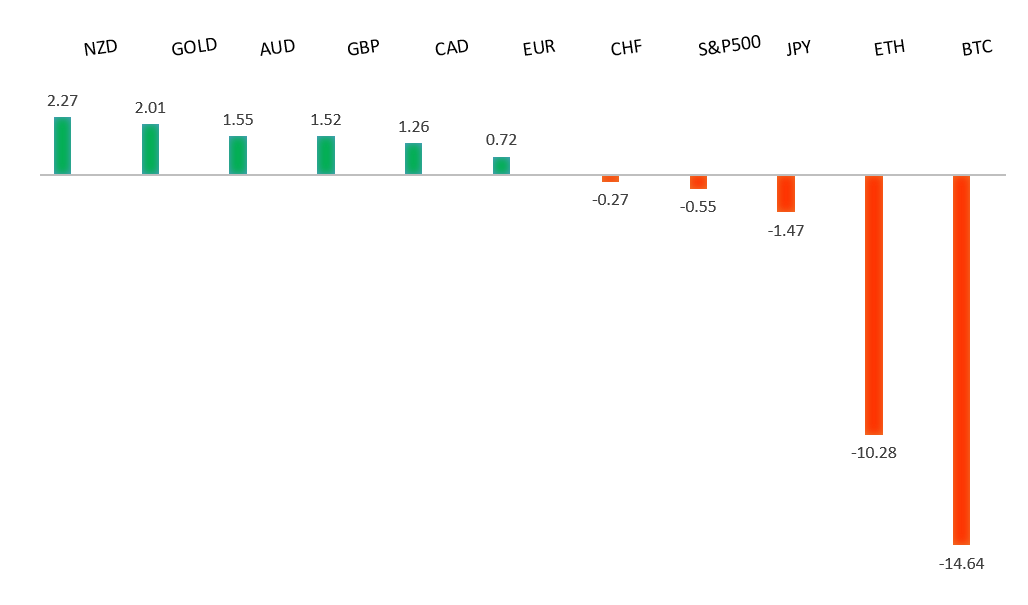

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1729 - 17 October high -Strong R1 1.1708 - 11 December high - Medium S1 1.1547 - 26 November low - Medium S2 1.1469 - 5 November low - Strong | ||

| EURUSD: fundamental overview | ||

| The ECB may lift its eurozone growth forecasts at next week’s final policy meeting, with President Christine Lagarde noting the economy has been outperforming earlier expectations. Markets still expect rates to stay at 2%, though recent hawkish comments—especially from Isabel Schnabel—have led traders to scale back expectations for 2026 rate cuts, even if many economists view pricing in hikes as premature given potential deflationary forces. The discussion comes amid broader debates about diverging Fed–ECB policy paths and differing exposure to political pressure. Adding to geopolitical tension, former EU diplomat Josep Borrell criticized the new U.S. National Security Strategy as a political “declaration of war,” urging Europe to recognize the increasingly adversarial stance. | ||

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, rallies should be well capped ahead of 160.00 ahead of a fresh down-leg back towards the 2024 low at 139.58. | ||

| ||

| R2 158.90 - 20 November/2025 high - Strong R1 156.96 - 9 December high - Medium S1 154.34 - 5 December low - Strong S2 153.61 - 14 November low - Medium | ||

| USDJPY: fundamental overview | ||

| USDJPY has slipped after the Fed’s rate cut as markets focused more on Powell’s caution about labor-market risks than on the Fed’s stated “high hurdle” for further easing. While the Fed still projects one more cut next year, markets expect two, and attention now turns to the BOJ, where a hike next week is widely priced in—any delay could trigger sharp yen weakness. Yet one Japanese bank notes that lingering doubts about the BOJ lifting rates toward 1% or higher continue to cap yen strength, with investors waiting for a clearer hawkish signal. Former BOJ official Hayakawa expects a hike to 0.75% in December and gradual tightening toward a 1.5% terminal rate, especially as Japan’s large fiscal package raises inflation risks. A key watch is whether the BOJ revises its estimate of the neutral rate, which would shape how restrictive future policy could become. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6707 - 17 September/2025 high - Strong R1 0.6686 - 10 December high - Medium S1 0.6520 - 28 November low - Medium S2 0.6421 - 21 November low - Strong | ||

| AUDUSD: fundamental overview | ||

| Australia’s November jobs report softened AUD sentiment as employment unexpectedly fell by 21,300, reversing October’s temporary strength. The jobless rate held at 4.3%, slightly better than forecasts, but largely due to a dip in participation. Economists caution that markets may have been too quick to price in 2026 rate hikes, noting risks of rising unemployment if labor demand weakens while population growth stays strong—potentially paving the way for rate cuts if inflation cools. Still, monthly employment data is volatile; the more influential Q4 CPI due January 28 is expected to show inflation staying uncomfortably high. Until then, markets may continue buying AUD on dips, anticipating policy divergence between the RBA and the Fed. | ||

| Suggested reading | ||

| 3 Contrarian Investment Ideas for 2026, D. Lefkovitz, Morningstar (December 10, 2025) Is It a Bubble? Has AI Enthusiasm Become Irrational?, H. Marks, Oaktree Capital (December 9, 2025) | ||