| ||

| 12th December 2025 | view in browser | ||

| Policy pivots driving market rotation | ||

| Global markets are rapidly repricing as central banks pivot policy in response to slowing growth, with the Fed’s dovish turn anchoring expectations while shifting investor focus toward labor, inflation data, and rotation into more rate-sensitive sectors. | ||

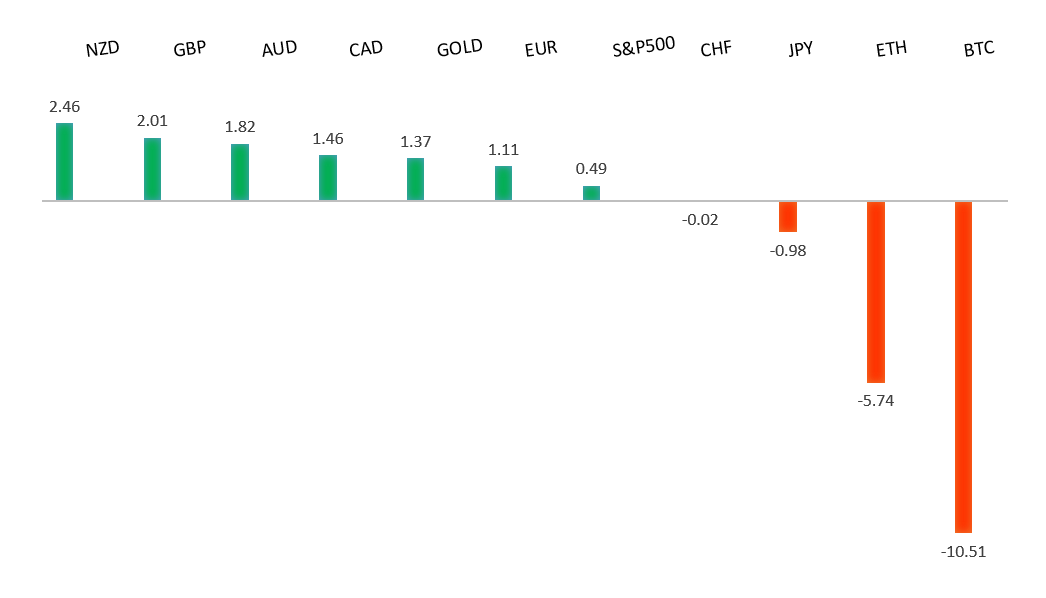

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1400. | ||

| ||

| R2 1.1919 - 17 September/2025 high -Strong R1 1.1779 - 1 October high - Medium S1 1.1615 - 9 December low - Strong S2 1.1469 - 5 November low - Strong | ||

| EURUSD: fundamental overview | ||

| EURUSD is hovering near two-month highs, supported by growing focus on policy divergence between a politically pressured Fed and a more insulated ECB. US political attacks on the Fed contrast with ECB signals that rate cuts may be over, though markets may be prematurely testing the idea of hikes in 2026, as many economists still see downside risks to euro-area growth from deflation, trade tensions, and a stronger euro. China’s rising trade surplus with Europe and the EU’s increasingly protectionist response add medium-term headwinds, but near-term FX impact remains limited unless tensions escalate. Optimism around a potential Ukraine ceasefire and bullish forecasts from some major US banks also offer mild near-term support for the euro, though longer-term gains hinge on policy credibility and geopolitical outcomes. | ||

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, rallies should be well capped ahead of 160.00 ahead of a fresh down-leg back towards the 2024 low at 139.58. | ||

| ||

| R2 158.90 - 20 November/2025 high - Strong R1 156.96 - 9 December high - Medium S1 154.34 - 5 December low - Strong S2 153.61 - 14 November low - Medium | ||

| USDJPY: fundamental overview | ||

| Markets are entering next week expecting the BOJ to deliver a rate hike, and failure to do so would likely trigger sharp yen weakness given that the move is already fully priced in. While investors remain skeptical that rates can rise much beyond 0.75%—seeing policymakers as trying to maintain loose fiscal policy, negative real rates, and a strong yen, an unsustainable mix—the yen has continued to weaken, ignoring official jawboning. Former BOJ official Hideo Hayakawa expects rates to rise gradually toward a 1.5% terminal level by 2027, arguing the BOJ is behind the curve on inflation, especially given expansionary fiscal policy. Still, the BOJ may struggle to signal a very hawkish path due to weak GDP growth and concerns over higher bond yields amid Japan’s fragile fiscal position. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6707 - 17 September/2025 high - Strong R1 0.6686 - 10 December high - Medium S1 0.6520 - 28 November low - Medium S2 0.6421 - 21 November low - Strong | ||

| AUDUSD: fundamental overview | ||

| Australia’s November labor report dampened AUD optimism, with employment falling by 21,300 instead of rising as expected, reversing October’s gains. While the unemployment rate held at a slightly better-than-forecast 4.3%, this was largely due to a lower participation rate, raising concerns that joblessness could increase as labor demand softens. Some economists argue markets have over-priced future rate hikes, warning that if inflation eases and economic conditions weaken into 2026, rate cuts could return. Although the RBA still sees the labor market as tight, employment data is volatile and markets are likely to focus more on upcoming CPI figures, with investors continuing to buy dips while expecting policy divergence between the Fed and RBA to persist. | ||

| Suggested reading | ||

| How Divided Is the Fed? 6 Soft Dissents Says ‘Very’ S. Hansen, Morningstar (December 10, 2025) Why the Stock Market Is Likely To Move Higher In 2026, M. Hulbert, Marketwatch (December 9, 2025) | ||