| ||

| 28th April 2025 | view in browser | ||

| Trade talks ease tariff fears | ||

| The market has shifted from expecting extreme tariffs to anticipating moderately elevated ones, which has helped to bolster risk appetite somewhat, though investors remain cautious amid ongoing trade negotiations, likely leading to choppy, sideways trading. | ||

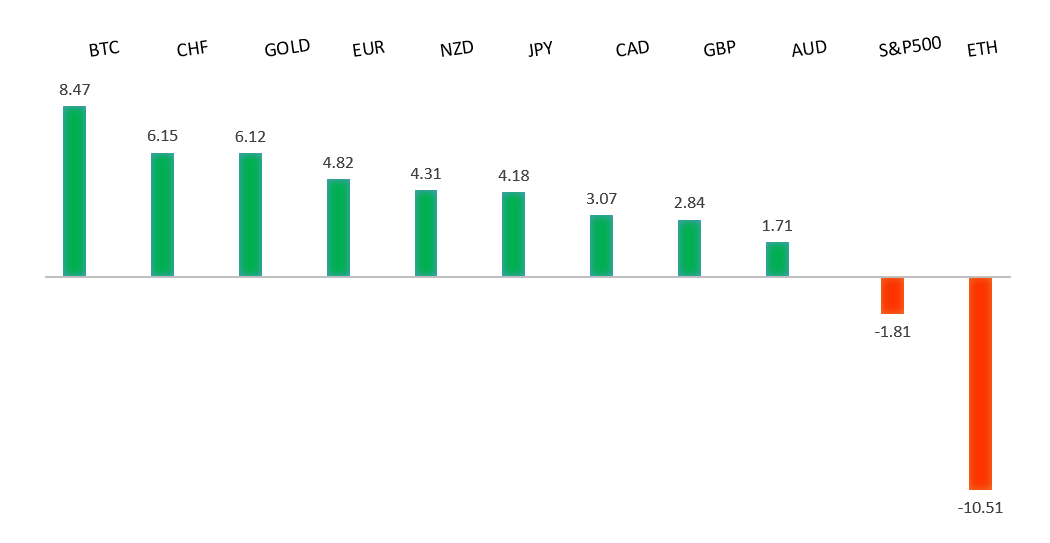

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro has finally broken out from a multi-month consolidation off a critical longer-term low. This latest push through the 2023 high lends further support to the case for a meaningful bottom, setting the stage for a bullish structural shift and the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported below 1.1000. | ||

| ||

| R2 1.1600 - Figure - Medium R1 1.1574 - 21 April/2025 high - Strong S1 1.1308 - 23 April low - Medium S2 1.1264 - 15 April low - Strong | ||

| EURUSD: fundamental overview | ||

| ECB Chief Economist Philip Lane stated that while U.S. tariffs may hinder Eurozone growth, trade tensions are unlikely to trigger a recession due to diverse trading partners. The ECB’s June meeting will release updated economic projections factoring in these tariffs, with expectations of weaker growth and inflation, aligning with the IMF’s revised 2025 forecast of 0.8% growth. ECB President Lagarde emphasized a data-driven approach to monetary policy, with potential for an eighth 25bps rate cut in June, as economists predict the deposit rate dropping from 2.25% to 1.5% to boost demand. Despite the ECB’s accommodative stance, Eurozone equities remain undervalued compared to U.S. markets, suggesting potential for growth and favoring European assets. This week’s Eurozone GDP and inflation data will be closely watched, while geopolitical developments, including Trump’s meeting with Zelensky and warnings of further sanctions on Russia, add uncertainty. | ||

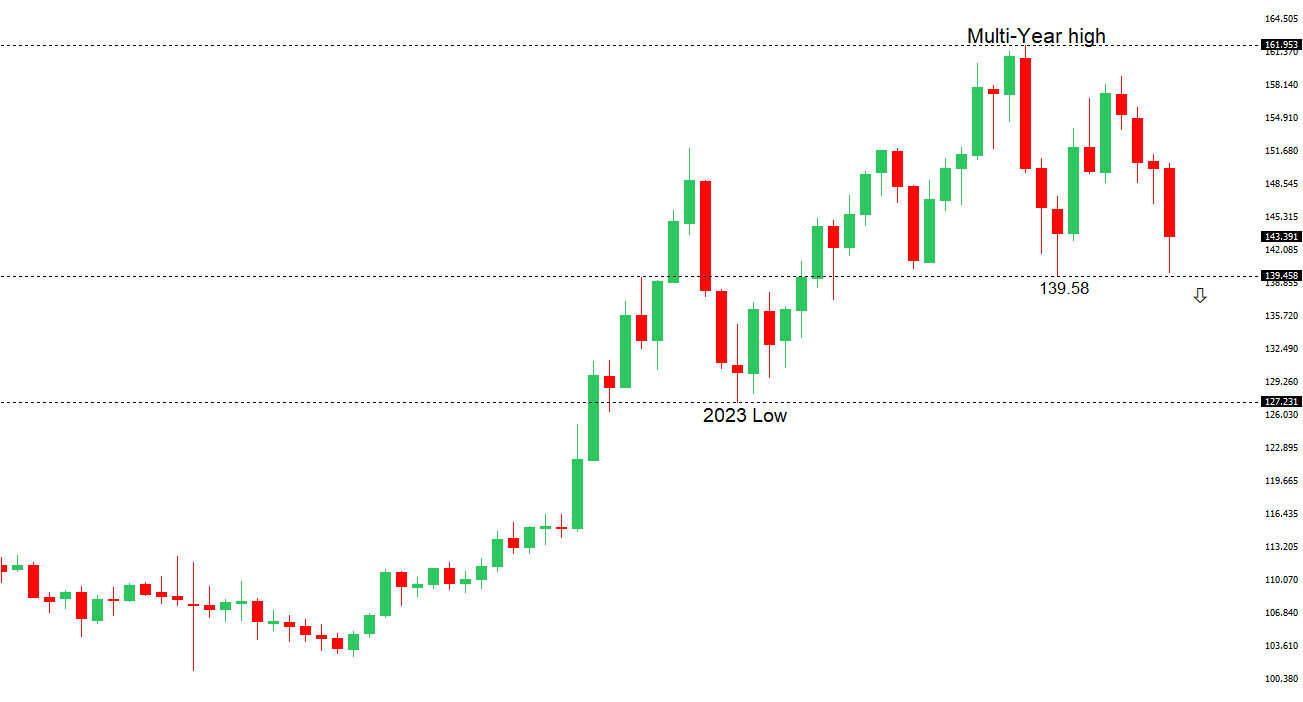

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, the door is now open for a deeper setback below the 2024 low at 139.58 over the coming sessions exposing a retest of the 2023 low. Rallies should be well capped below 150.00. | ||

| ||

| R2 144.58 - 11 April high - Medium R1 144.04 - 25 April high - Medium S1 139.89 - 22 April/2025 low - Medium S2 139.58 - 2024 Low - Strong | ||

| USDJPY: fundamental overview | ||

| Risk sentiment is improving and the yen has taken a hit as a consequence on the back of the traditional correlation. The Bank of Japan is anticipated to maintain its 0.5% target rate at the April 30-May 1 meeting due to trade war uncertainties, despite Tokyo’s CPI rising to 3.5% and core inflation at 3.4%, signaling persistent inflationary pressures above the BOJ’s 2% target. A Bloomberg survey indicates no policy change is expected, with only 45% of economists predicting a rate hike by September, and the BOJ’s terminal rate forecast lowered to 1%. The BOJ is likely to cut its growth forecast but signal gradual rate hikes to support yen strength, potentially aiding US-Japan trade talks, where Japan seeks concessions on tariffs and aims for an agreement by the G7 summit in June. Japan has been resisting U.S. efforts to align against China due to vital trade ties. Goldman Sachs has been out calling for USDJPY 135 within 12 months as the dollar’s overvaluation unwinds. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6500 - Psychological - Strong R1 0.6440 - 22 April/2025 high - Medium S1 0.6333 - 17 April low - Medium S1 0.6275 - 14 April low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian Dollar is showing signs of bottoming, driven by a shift away from USD assets and supported by China’s signaling of accelerated fiscal and monetary stimulus, including potential rate cuts and increased bond issuance, alongside easing US-China trade tensions. Australia’s Q1 and Q2 2025 GDP forecasts remain at 0.5% QoQ, with 2025 CPI slightly lowered to 2.5% YoY, and the RBA is expected to cut rates from 4.10% to 3.85% by Q2 2025, with markets pricing in a May cut due to growth concerns outweighing inflation risks. S&P has been out warning Australia’s AAA credit rating could be at risk if election pledges increase deficits, while polls suggest the Labor government is poised to win the May 3 election. | ||

| Suggested reading | ||

| Tariffs Are Hitting Global Supply Chains And Shipping, B. Wilds, Advancing Time (April 27, 2025) Is The “Dollar” Still King? Unpacking America’s Paper Power, D. Morgan, The Morgan Report (April 27, 2025) | ||