Next 24 hours: Australian Dollar shines after RBA surprises

Today’s report: Equities turn south on softer US ISM data

Some of the big headlines from Monday include US equities reversing course from yearly highs on softer US ISM data, Moody’s reaffirming a stable outlook on the US AAA rating, and oil supported on news Saudi Arabia will make a larger supply cut in July.

Wake-up call

- Lagarde, Nagel

- foreign investment

- Asset managers

- RBA surprises

- RBA move

- milk payments

- Inflation headache

- Dealers report

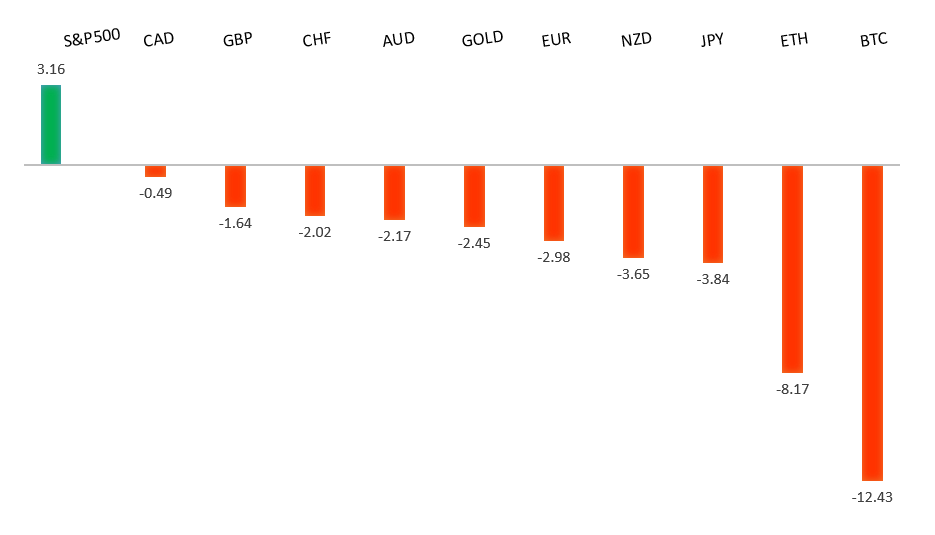

Peformance chart: 30 Day Performance vs. US dollar (%)

Suggested reading

- Saudi Arabia's Solo Oil Production Cut Is a Risky Strategy, J. Blas, Bloomberg (June 5, 2023)

- The GOP Created ‘Chair Bernanke,’ And the Internet Is Forever, J. Tamny, Forbes (June 4, 2023)

Chart talk: Technical & fundamental highlights

Choose pair:

EURUSD – technical overview

The Euro remains well supported on dips following a run to the topside through 1.1000 earlier this year. Any additional setbacks should be well supported ahead of 1.0500 in favor of the formation of the next major higher low and a bullish continuation. Ultimately, only a monthly close back below 1.0500 would give reason for concern. Next key resistance comes in the form of the March 2022 high at 1.1185.EURUSD – fundamental overview

The Euro recovered out from Monday lows, getting a boost from notable hawkish ECB communications. ECB Nagel initially struck a hawkish chord, saying underlying price pressures were "far too high" while adding ECB policymakers therefore "couldn't and wouldn't falter in the fight against inflation." ECB Chief Lagarde then said food price inflation remained elevated, there was no concrete evidence inflation had peaked, and the central bank was totally committed to fighting inflation. Looking ahead, key standouts on Tuesday’s calendar for the remainder of the day come from German factory orders, construction PMIs out of the Eurozone, Germany, and UK, ECB consumer inflation expectations, Eurozone retail sales, Canada building permits, and Canada Ivey PMIs.EURUSD - Technical charts in detail

GBPUSD – technical overview

Signs have emerged of the market wanting to put in a longer-term base after collapsing to a record low in September 2022. The November 2022 monthly close back above 1.2000 strengthens this prospect. Any setbacks should now be well supported ahead of 1.2000. Next key resistance comes in at 1.2680.GBPUSD – fundamental overview

All of the updates out of the UK on Monday were Pound supportive, which helped the Pound absorb a wave of broad based US Dollar demand post last Friday's US jobs report. UK new car registrations jumped, UK final services PMIs edged up, and an Ernst & Young survey showed the UK widening its lead as Europe's top draw for foreign direct investment in financial services. Looking ahead, key standouts on Tuesday’s calendar for the remainder of the day come from German factory orders, construction PMIs out of the Eurozone, Germany, and UK, ECB consumer inflation expectations, Eurozone retail sales, Canada building permits, and Canada Ivey PMIs.USDJPY – technical overview

The major pair has seen a nice recovery following the massive correction out from multi-year highs. Setbacks have finally been well supported ahead of 125.00 in the 127s thus far. At this stage, it looks like the market could be wanting to resume the bigger picture uptrend and head back towards a retest of that multi-year high from October 2022 up at 151.95. Look for any weakness to continue to be well supported in favor of higher lows along the way.USDJPY – fundamental overview

Asset managers are joining hedge funds in increasing bearish Yen bets on speculation the BOJ won't be moving any time soon to adjust ultra loose monetary policy. Looking ahead, key standouts on Tuesday’s calendar for the remainder of the day come from German factory orders, construction PMIs out of the Eurozone, Germany, and UK, ECB consumer inflation expectations, Eurozone retail sales, Canada building permits, and Canada Ivey PMIs.AUDUSD – technical overview

There are signs of the potential formation of a longer-term base following the late 2022 surge back above 0.6500. Next key resistance comes in at 0.7284. Setbacks should continue to be well supported in the 0.6500 area. Only a monthly close below 0.6500 would give reason for rethink.AUDUSD – fundamental overview

The Australian Dollar had already done a nice job holding up on Monday following a solid round of Aussie data, before rocketing higher on Tuesday after the RBA delivered a surprise 25 basis point rate hike and accompanied the hike with a statement that some further tightening of monetary policy may be required. Looking ahead, key standouts on Tuesday’s calendar for the remainder of the day come from German factory orders, construction PMIs out of the Eurozone, Germany, and UK, ECB consumer inflation expectations, Eurozone retail sales, Canada building permits, and Canada Ivey PMIs.USDCAD – technical overview

A recent surge back above 1.3000 signals an end to a period of bearish consolidation and suggests the market is in the process of carving out a more significant longer-term base. Next key resistance now comes in up into the 1.4000 area. Setbacks should be very well supported down into the 1.3000 area.USDCAD – fundamental overview

The Canadian Dollar has already recovered from Monday setbacks, likely getting a boost from the hawkish RBA decision which has resulted in an upgraded hawkish outlook for the Bank of Canada. Looking ahead, key standouts on Tuesday’s calendar for the remainder of the day come from German factory orders, construction PMIs out of the Eurozone, Germany, and UK, ECB consumer inflation expectations, Eurozone retail sales, Canada building permits, and Canada Ivey PMIs.NZDUSD – technical overview

Overall pressure remains on the downside with the market once again stalling out on a run up into the 0.6500 area. Ultimately, a break back above 0.6577 would be required to take the immediate pressure off the downside. A monthly close below 0.6000 would intensify bearish price action.NZDUSD – fundamental overview

The New Zealand Dollar has managed to trade higher early Tuesday, mostly on the back of Aussie gains from the RBA rate hike. At the same time, the Kiwi currency is a clear laggard against its commodity cousins, with the RBNZ outlook much less hawkish and New Zealand data looking softer of late. Dairy prices have been in focus after Fonterra, the world's biggest dairy exporter, lowered its projected milk payments to New Zealand farmers in May. Looking ahead, key standouts on Tuesday’s calendar for the remainder of the day come from German factory orders, construction PMIs out of the Eurozone, Germany, and UK, ECB consumer inflation expectations, Eurozone retail sales, Canada building permits, and Canada Ivey PMIs.US SPX 500 – technical overview

Longer-term technical studies are in the process of unwinding from extended readings off record highs. Look for rallies to be well capped in favor of lower tops and lower lows. A monthly close back above 4300 will be required at a minimum to take the immediate pressure off the downside. Next major support comes in at 4049.US SPX 500 – fundamental overview

We've finally reached a point in the cycle where the Fed recognizes unanchored inflation expectations pose a greater downside risk than over-tightening. This is significant, as it means less investor friendly monetary policy that risks potential recession in the months ahead. Overall, we expect inflation to continue to be a problem in 2023 that results in downside pressure into rallies.GOLD (SPOT) – technical overview

The 2019 breakout above the 2016 high at 1375 was a significant development, opening the door for fresh record highs. Setbacks should now be well supported above 1600 on a monthly close basis ahead of the next major upside extension. The recent break back above 1808 strengthens the bullish outlook. Next major resistance comes in at 2100, above which opens the next extension towards 2,500.GOLD (SPOT) – fundamental overview

The yellow metal continues to be well supported on dips with solid demand from medium and longer-term accounts. These players are more concerned about inflation risk and a less upbeat global growth outlook. All of this should keep the commodity well supported, with many market participants also fleeing to the hard asset as the grand dichotomy of record high equities and record low yields comes to an unnerving climax.