| ||

| 4th June 2026 | view in browser | ||

| Markets navigate a fragile equilibrium | ||

| Markets remain driven by a fragile mix of Middle East geopolitical risk, sticky inflation and Fed uncertainty, and the ongoing AI investment boom, supporting the US dollar, underpinning oil and gold, and keeping broader risk sentiment cautious despite resilient equity valuations. | ||

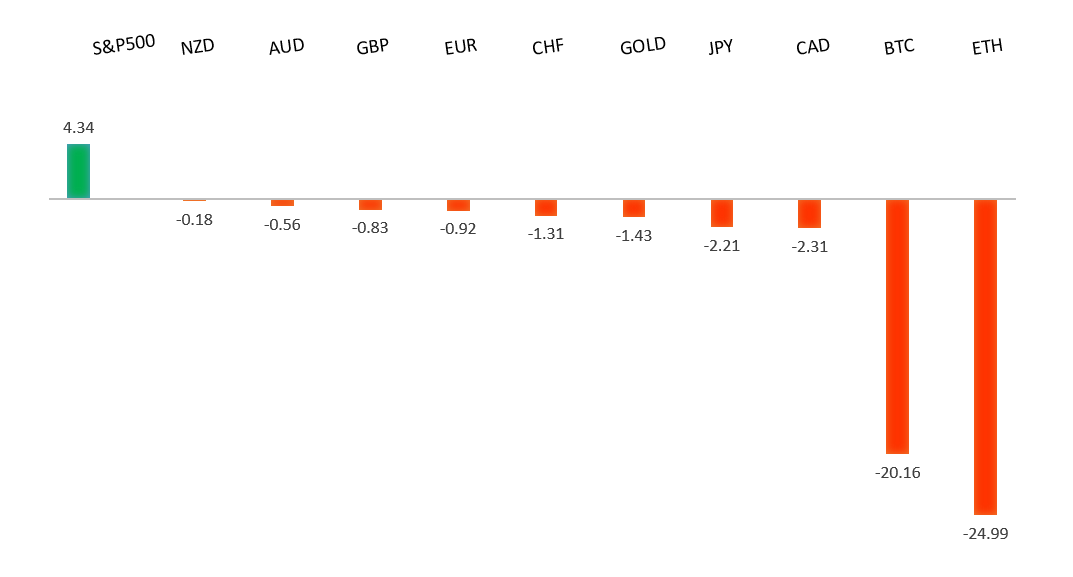

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1797 - 6 May high - Medium R1 1.1722 - 14 May high - Medium S1 1.1576 - 21 May low - Medium S2 1.1504 - 3 April low - Strong | ||

| EURUSD: fundamental overview | ||

| The euro has remained broadly supported on the back of a steadily more hawkish ECB outlook, with markets increasingly convinced the central bank will deliver a 25bp rate hike at next week’s meeting and potentially follow up with additional tightening later this year as inflation pressures remain elevated. Recent data showed Eurozone CPI accelerating to 3.2% in May, with core inflation also firming, reinforcing concerns that higher energy costs linked to Middle East tensions are feeding into broader price pressures. At the same time, ECB officials have continued to signal a willingness to act to prevent inflation expectations from becoming entrenched, helping underpin Euro demand despite signs of slowing regional growth and softer business activity data. More recently, easing geopolitical tensions following a reported Israel-Lebanon ceasefire have weighed on safe-haven demand for the US dollar, allowing EURUSD to be supported into dips. That said, upside in the single currency remains tempered by lingering uncertainty surrounding the broader Middle East conflict, elevated oil prices, and expectations that the Federal Reserve could maintain a relatively hawkish policy stance if US inflation risks persist. | ||

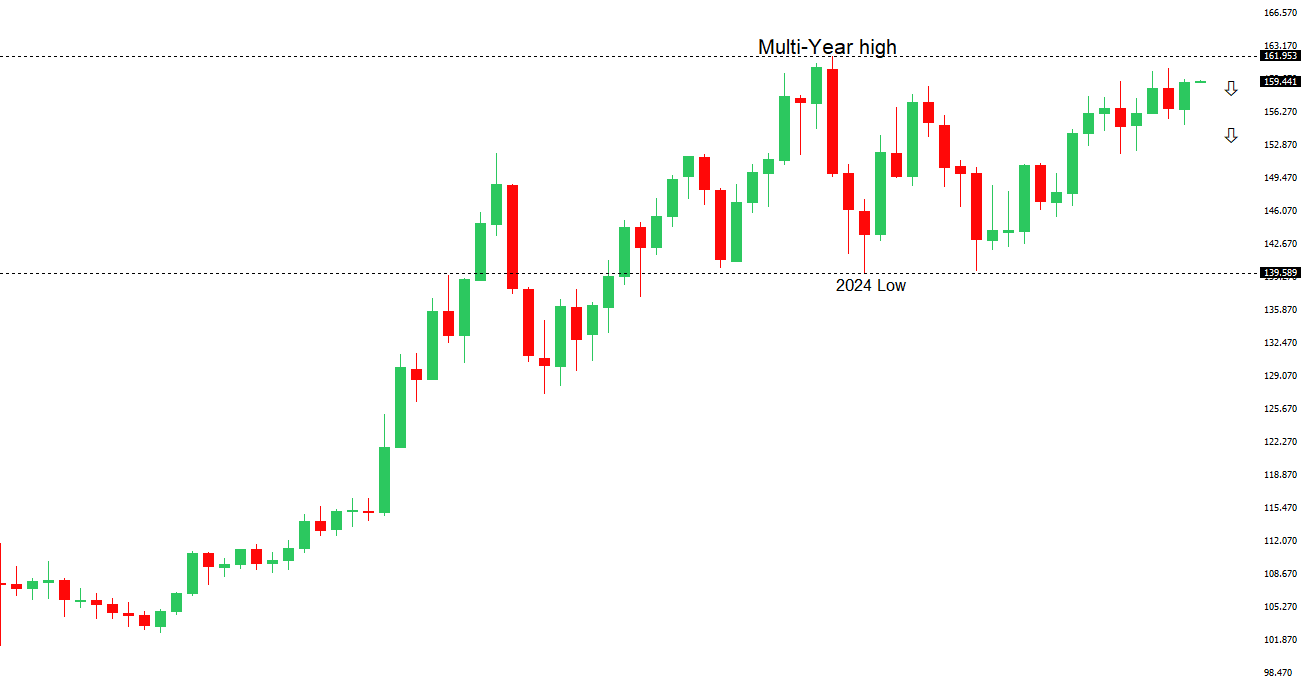

| USDJPY: technical overview | ||

| There are signs of the formation of a meaningful top after the market put in a multi-year high in 2024. At this point, rallies should be well capped above 160.00 in favor of a fresh down-leg back towards the 2024 low at 139.58. Only a monthly close above 160.00 negates. | ||

| ||

| R2 160.73 - 30 April/2026 high - Strong R1 160.09 - 3 June high - Strong S1 158.59 - 20 May low - Medium S2 157.29 - 14 May low - Medium | ||

| USDJPY: fundamental overview | ||

| The yen remains under pressure as the fundamental backdrop continues to favor capital outflows and a wide yield advantage for the US dollar. While Japanese officials have stepped up verbal intervention, with Prime Minister Takaichi, Finance Minister Katayama, and other policymakers reiterating their readiness to act against excessive and speculative FX moves, markets remain focused on the underlying drivers of yen weakness. Despite the Bank of Japan’s gradual normalization efforts and rising JGB yields, Japanese rates remain well below US Treasury yields, preserving the attractiveness of dollar assets and carry trades. At the same time, Japan’s status as a major energy importer leaves the economy vulnerable to elevated oil prices and geopolitical tensions, which can worsen the trade balance and weigh on the currency. Investors also remain unconvinced that the BoJ will tighten policy aggressively enough to materially narrow rate differentials, with government officials continuing to stress that specific policy measures remain the central bank’s decision. As a result, while intervention threats may slow the pace of USDJPY gains around the closely watched 160 level, markets continue to see sustained yen strength as unlikely absent a more pronounced slowdown in the US economy, a sharper narrowing in US-Japan yield spreads, or a significantly more hawkish shift from the BoJ. | ||

| AUDUSD: technical overview | ||

| There are signs of the formation of a longer-term base with the market recovering out from a meaningful longer-term support zone. The latest monthly close back above 0.7000 takes the big picture pressure off the downside and strengthens the case for a bottom, with the focus now on a push towards 0.8000. Setbacks should now be well supported ahead of 0.6700. | ||

| ||

| R2 0.7278 - 6 May/2026 high - Strong R1 0.7222 - 17 April high - Medium S1 0.7079 - 19 May low - Medium S2 0.6963 - 8 April low - Strong | ||

| AUDUSD: fundamental overview | ||

| The Australian Dollar has been underpinned by a combination of resilient domestic fundamentals and a still-hawkish Reserve Bank of Australia, with AUD finding support after April trade data showed a stronger-than-expected return to surplus as exports surged 7.2% month-on-month, driven by solid shipments of iron ore, coal and LPG, while import growth slowed sharply. The data reinforced the view that external demand remains supportive despite a moderation in domestic activity. On the monetary policy front, RBA Governor Bullock reiterated that inflation remains too high and is expected to rise further in the near term, maintaining a tightening bias even as the central bank paused after three consecutive rate hikes. While recent GDP figures and easing unit labor cost growth have strengthened expectations that the RBA may remain on hold for now, markets continue to price a meaningful chance of another hike later this year should inflation prove sticky. More broadly, the AUD has also benefited from an improvement in global risk sentiment and ongoing US dollar softness, though gains have been tempered by concerns over slowing Australian household demand, a cooling housing market, and rising geopolitical tensions in the Middle East, which have boosted safe-haven demand for the US dollar and increased uncertainty around the global growth outlook. | ||

| Suggested reading | ||

| Three examples of how AI could work for good, M. Murgia, Financial Times (May 31, 2026) The Fed’s Balance Sheet Is Costly No Matter What, N. Michel, Cato (June 2, 2026) | ||