| ||

| 20th November 2025 | view in browser | ||

| Nvidia lifts sentiment as Fed doubts grow | ||

| Federal Reserve minutes from the October meeting reveal deep divisions over the path of interest rates, with disagreements over both the recent rate cut and the outlook for December, where policymakers will be forced to decide policy without October or November employment data due to BLS delays from the government shutdown. | ||

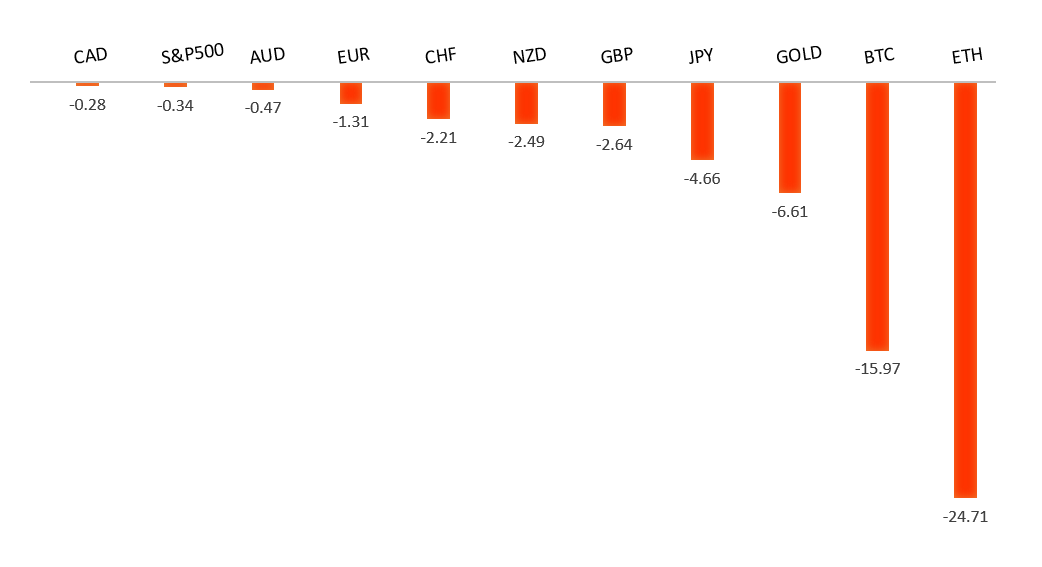

| Performance chart 30day v. USD (%) | ||

| ||

| Technical & fundamental highlights | ||

| EURUSD: technical overview | ||

| The Euro outlook remains constructive with higher lows sought out on dips in favor of the next major upside extension targeting the 2021 high at 1.2350. Setbacks should be exceptionally well supported ahead of 1.1300. | ||

| ||

| R2 1.1729 - 17 October high -Strong R1 1.1669 - 28 October high - Medium S1 1.1469 - 5 November low - Medium S2 1.1392 - 1 August low - Strong | ||

| EURUSD: fundamental overview | ||

| The eurozone’s current account surplus edged up in September to €23.1bn, supported by solid goods and services trade despite ongoing income deficits, though the surplus has generally been shrinking relative to GDP. Analysts see this as evidence of resilience driven by steady exports and contained inflation, but warn that industrial weakness and global trade uncertainties may limit future gains. Inflation data for October confirmed sticky price pressures, reinforcing expectations that the ECB will keep rates steady. One well regarded analyst argues the euro is slightly undervalued and could appreciate ahead of key U.S. data releases, forecasting EURUSD at 1.18 by year-end as U.S. rate-cut expectations build. Meanwhile, Germany’s October PPI is expected to stabilize, signaling that industrial price declines are easing but underlying demand and manufacturing challenges persist. | ||

| USDJPY: technical overview | ||

| There are signs of a meaningful top in place after the market put in a multi-year high in 2024. At this point, rallies should be well capped ahead of 160.00 ahead of a fresh down-leg back towards the 2024 low at 139.58. | ||

| ||

| R2 158.88 - 10 January/2025 high - Strong R1 158.00 - Figure - Medium S1 156.00 - Figure - Medium S2 155.21 - 19 November low - Medium | ||

| USDJPY: fundamental overview | ||

| Recent remarks from key Japanese officials have fueled further yen weakness by signaling limited room for near-term monetary tightening and raising doubts about the Bank of Japan’s independence. Comments suggesting no rate hike before March 2026, hints that the BOJ–government accord may be revised, and indications that yen weakness was not even discussed with Governor Ueda all reinforced the view that policy is being steered more by politics than economics. With speculation rising, no sign of imminent FX intervention, and expectations of a large new fiscal stimulus—alongside tense China relations—markets see any potential BOJ rate hike as “one and done,” leaving the path of least resistance for USDJPY still upward unless the U.S. Federal Reserve shifts to faster rate cuts. | ||

| AUDUSD: technical overview | ||

| There are signs of the potential formation of a longer-term base with the market trading down into a meaningful longer-term support zone. Only a monthly close below 0.5500 would give reason for rethink. A monthly close back above 0.7000 will take the big picture pressure off the downside and strengthen case for a bottom. | ||

| ||

| R2 0.6629 - 1 October high - Strong R1 0.6618 - 29 October high - Medium S1 0.6451 - 19 November low - Medium S1 0.6440 - 14 October low - Strong | ||

| AUDUSD: fundamental overview | ||

| Nvidia’s strong earnings boosted global risk sentiment and helped the AUD rebound from its 200-day moving average, while recent Australian data continues to keep the odds of rate cuts low. Indicators like the Westpac Leading Index show improving economic momentum into 2026, and steady wage growth suggests inflation risks remain contained but not eliminated. With resilient consumer confidence, strong home lending, and stable employment, the RBA is expected to keep rates on hold, with some analysts believing the easing cycle has ended. Policymakers remain cautious about reigniting inflation, and upcoming comments from RBA chief economist Sarah Hunter may lean slightly hawkish given the strengthening demand backdrop. | ||

| Suggested reading | ||

| There’s No Such Thing As a K-Shaped Economy, J. Tamny, RCM (November 19, 2025) The Fed’s Rate Decision Isn’t the Market’s Biggest Worry, M. Hulbert, Marketwatch (November 18, 2025) | ||